Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Do I Need Umbrella Insurance? Who Should Get a Personal Umbrella Policy in 2026

July 1, 2025

.webp)

“Do I really need umbrella insurance?” It’s a common question for anyone learning about this extra liability coverage. The idea of an additional insurance policy might sound excessive if you already have auto and home insurance. But a personal umbrella policy can be a critical safety net depending on your situation.

In this article, we’ll help you figure out if you need umbrella insurance by looking at who benefits the most from it and why. We’ll cover the types of people and scenarios where umbrella insurance makes sense (and when it might not be necessary).

By understanding your own assets, lifestyle, and risk exposure, you can make an informed decision. As we navigate these considerations, keep in mind how umbrella insurance works: it’s there to protect against unlikely but financially devastating events (major lawsuits, huge claims).

We’ll also sprinkle in some 2025 context – costs, lawsuit trends – to ensure the advice is up-to-date. Plus, we’ll mention a few financial tips (like using Kudos for smart spending) because protecting your wealth and growing it often go hand in hand.

Let’s dive in and see if umbrella insurance is right for you.

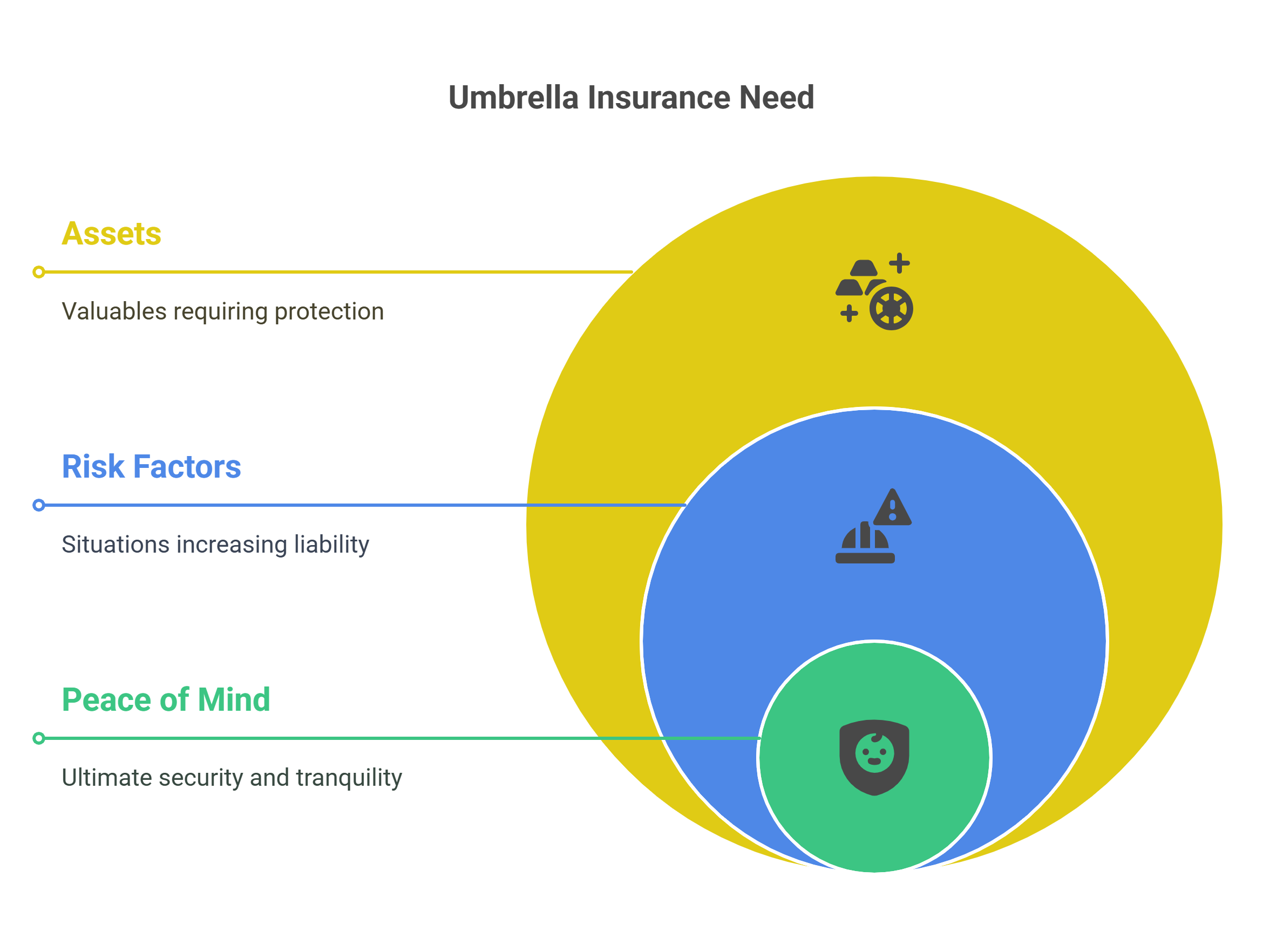

Who Really Needs Umbrella Insurance?

There’s no law saying you must have umbrella insurance; it’s optional. The real question is about risk management: Can you afford NOT to have it if something big happens? You need to assess your personal risk factors.

Here are the profiles of people who should strongly consider an umbrella policy:

1. Homeowners with Assets

If you own a home (or multiple properties), especially in 2025’s market where home equity might be significant, you have assets that could be targeted in a lawsuit. Liability claims from accidents on your property can easily exceed your homeowners insurance limits.

For example, if a visitor is severely injured at your home, you could face a lawsuit for medical costs and “pain and suffering” that surpasses a $300k homeowners policy limit. Your house, savings, and investments become vulnerable without an umbrella.

Essentially, if you’ve built some wealth – a house, a retirement fund, etc. – an umbrella policy is a shield for that wealth. Even middle-class homeowners find value in umbrella insurance, not just the ultra-rich.

2. Individuals with High Net Worth (or on the way there)

Consider your net worth (the sum of your assets minus liabilities). The higher it is, the more you stand to lose in a lawsuit. Financial experts often suggest that anyone with a net worth over around $500,000 should have umbrella insurance. This isn’t a hard rule, but it’s a common benchmark.

Why $500k? Because a serious liability claim can easily reach or exceed that amount, and at that level of assets, you have enough that plaintiffs (or their lawyers) would find it “worth it” to pursue your money. If you’re a millionaire (congrats), umbrella insurance is almost a no-brainer. But even if you’re at say $300k net worth and climbing, think about the trajectory: you will have more to protect in the near future.

Umbrella insurance can scale with you (you can increase coverage as needed). It’s wise to get in place once you have substantial assets. Remember: Umbrella policies also protect future earnings – so even if you’re younger with “only” say $100k net worth now but a high salary, someone could target your future income in a judgment. Protecting your future wealth is as important as protecting what you have today.

3. Families with Young Drivers or Active Kids

If you have teenagers who drive, or even college-age drivers on your policy, your household risk is higher than average. Statistically, teen drivers have more accidents. One major accident with injuries could blow past auto policy limits. As a parent (who likely would be held liable since you probably own the car/insurance), an umbrella policy is crucial once you have a teen behind the wheel.

Similarly, if you have kids who host friends at your home often (pool parties, sports in the yard, etc.), there’s increased chance of injuries on your property. Kids (and their visiting friends) can unintentionally create liability — e.g. a visiting child breaks an arm on your trampoline, or your kid accidentally injures someone with an errant baseball throw. Umbrella insurance is there for those kinds of family-related mishaps that result in big claims.

4. Frequent Hosts or Public Figures

Do you frequently have guests over, or do you volunteer in the community, or have a bit of a public profile? The more people you interact with or host, the greater the chance of something happening. If you’re the neighborhood BBQ house or you often let friends use your vacation home, consider the exposure.

Additionally, if you’re known in the community or have a high-profile job, people might be more inclined to sue (rightly or wrongly) thinking you have “deep pockets” or for the publicity. Umbrella insurance provides a legal defense for frivolous suits too — if someone tries an unfounded lawsuit, your umbrella will still cover the legal costs to defend you (up to the policy limit). It’s protection for your reputation and finances in that sense.

5. Owners of Rental Property or Land

If you rent out property (be it a single-family home, a duplex, or even just a room via Airbnb regularly), you take on the liability of a landlord. Landlords can be sued for accidents on the premises, tenant injuries, or even things like wrongful eviction claims. Even with landlord insurance, some judgments can exceed those limits or fall into gray areas.

An umbrella policy extends over your rental properties (as long as they’re listed on the policy) and can cover large liability claims from tenants. For example, if a tenant’s guest drowns in an unsupervised pool at your rental – that could be a multi-million dollar lawsuit due to negligence. Umbrella insurance would be crucial in such a scenario.

6. Boat and Recreational Vehicle Owners

Do you own a boat, jet ski, ATV, or other recreational vehicles? These fun toys come with high liability risk. A boating accident, for instance, could injure multiple people (think of a collision on the water or a passenger injury) and result in huge claims.

While you should have primary liability coverage via boat insurance, etc., those often have limits like $300k or $500k. Umbrella can cover above that if you’re at fault in a serious accident. Same goes for snowmobiles, off-road vehicles, etc. If you have such assets, you are a candidate for umbrella insurance. (Be sure to inform your insurer of these so the umbrella covers them – typically you need underlying policies on them too.)

7. People Worried About Lawsuit Trends

It’s worth noting that over the years, the costs of lawsuits (settlements, judgments, legal fees) have risen. In 2025, we continue to see high jury awards for liability cases (some states and jurisdictions are known for big payouts). If you’re generally risk-averse or concerned about this trend, an umbrella policy provides peace of mind.

It’s one of those things that you’ll be tremendously relieved to have if you ever face a big claim. Many financially savvy individuals get umbrella insurance for this very reason: the world is unpredictable, and this is cheap “sleep insurance” to not worry about worst-case scenarios.

In summary, you likely need umbrella insurance if you identified with one or more of the above: you have assets (home, savings) worth protecting, you have risk factors (young drivers, rental properties, etc.), or you just want maximum peace of mind.

Who Might Not Need Umbrella Insurance (Or Could Wait)?

Umbrella insurance is valuable, but there are cases where it might not be urgent or necessary. Let’s consider who might reasonably forgo it:

1. People with very limited assets and low income

If you’re just starting out financially, rent your home, have minimal savings, and don’t have a high income, then the chances of someone suing you for a large sum (and actually being able to collect) are lower. Essentially, you can’t squeeze water from a stone – if you truly have no assets, lawyers might not pursue a huge claim against you vigorously because there’s nothing to get. Also, if you declare bankruptcy due to a judgment, that’s a route (albeit a painful one) out of paying – which is an option people with no assets might end up using.

2. Individuals adequately covered by existing policies for their situation

If you only drive minimally and have high auto liability limits already, or you never host anyone and live a very low-liability lifestyle, the additional coverage of an umbrella might not provide much incremental benefit. For instance, a retiree who doesn’t drive and lives in a condo (with no pool, no kids around, etc.) and has $500k liability on their condo and an idle umbrella coverage might rarely find a scenario where a claim would exceed those limits.

3. Those who are already judgment-proof

Similar to limited assets, if you have assets but they are legally protected from creditors (for example, in some states retirement accounts or homestead equity up to a certain amount are protected from lawsuits), you might be less concerned. Also, elderly individuals who plan to rely on legal protections or have trust structures might sometimes opt out.

Even if you think you fall into these categories, carefully evaluate your exposure. Umbrella insurance is inexpensive enough that many people who are on the fence choose to get it “just in case,” knowing they can drop it later or adjust coverage as life changes.

It’s also worth considering how you’d feel in the unlikely event of a lawsuit. If the thought of any chance of losing future earnings or dealing with legal hassle stresses you out, umbrella insurance buys peace of mind, regardless of your current asset level.

If you’re asking “Do I need umbrella insurance?”, chances are you’ve got something worth protecting or some risk that’s nagging at you. In 2025, with lawsuit verdicts sometimes reaching eye-popping figures, having that extra cushion can be more important than ever.

Weighing the Cost vs. Risk

Another angle to decide: compare the cost of the policy to the potential benefit. Umbrella insurance is quite affordable. In 2025, the average cost for a $1 million umbrella policy is roughly $150–$300 per year (around $15–$25 per month), depending on your situation. Even on the high end, say you have multiple homes and teen drivers and it costs $500/yr, that’s still relatively low.

Now think of the potential loss without it – hundreds of thousands of dollars, or even millions, plus legal headaches. It’s almost like buying a lottery ticket in reverse: the “jackpot” (but a bad one) is a huge lawsuit, and the premium is the small price to avoid that jackpot. If you find that trade-off worth it (and most do), then you need umbrella insurance.

Put simply, ask yourself: “If I was sued for $1 million tomorrow, how would I pay it?” If you don’t have a good answer (and very few do, aside from “liquidate everything and still come up short”), then purchasing an umbrella policy is a prudent choice.

Making the Decision

Consider the following steps to conclude whether to get umbrella coverage:

- List Your Assets and Risks: Write down your major assets (home equity, savings, investments, valuable property). Then list risk factors (do you drive often? kids? pool? dogs? etc.).

- Look at Your Current Insurance Limits: Check your auto and home liability limits. Are they $100k, $300k, $500k? This shows how much coverage you have before an umbrella would be needed.

- Evaluate Likelihood vs Impact: Even if a major event is unlikely, its impact could be life-changing. Think about your personal comfort with that risk.

- Consider Advice/Benchmarks: Align with expert recommendations like the net worth rule. If you’re above a threshold that experts flag (like the earlier $500k net worth example), lean towards yes. If you’re below but close or expect to be above soon (maybe your house is rapidly appreciating or you’re building a portfolio), it’s easier to get it now than to wait.

- Get a Quote: It doesn’t hurt to get a quote for umbrella insurance. You might be surprised how inexpensive it is for you. If the cost is very low, it’s almost an easy decision to add it. If it’s higher (maybe due to multiple risk factors), weigh that cost against the peace of mind it brings.

Remember that umbrella insurance can be scaled. You could start with a $1M policy now, and in a few years if your assets double, increase to a $2M policy. It’s not locked in stone – you can adapt it to your needs over time. The key is to not be caught without it when a disaster strikes, because by then it’s too late to buy insurance.

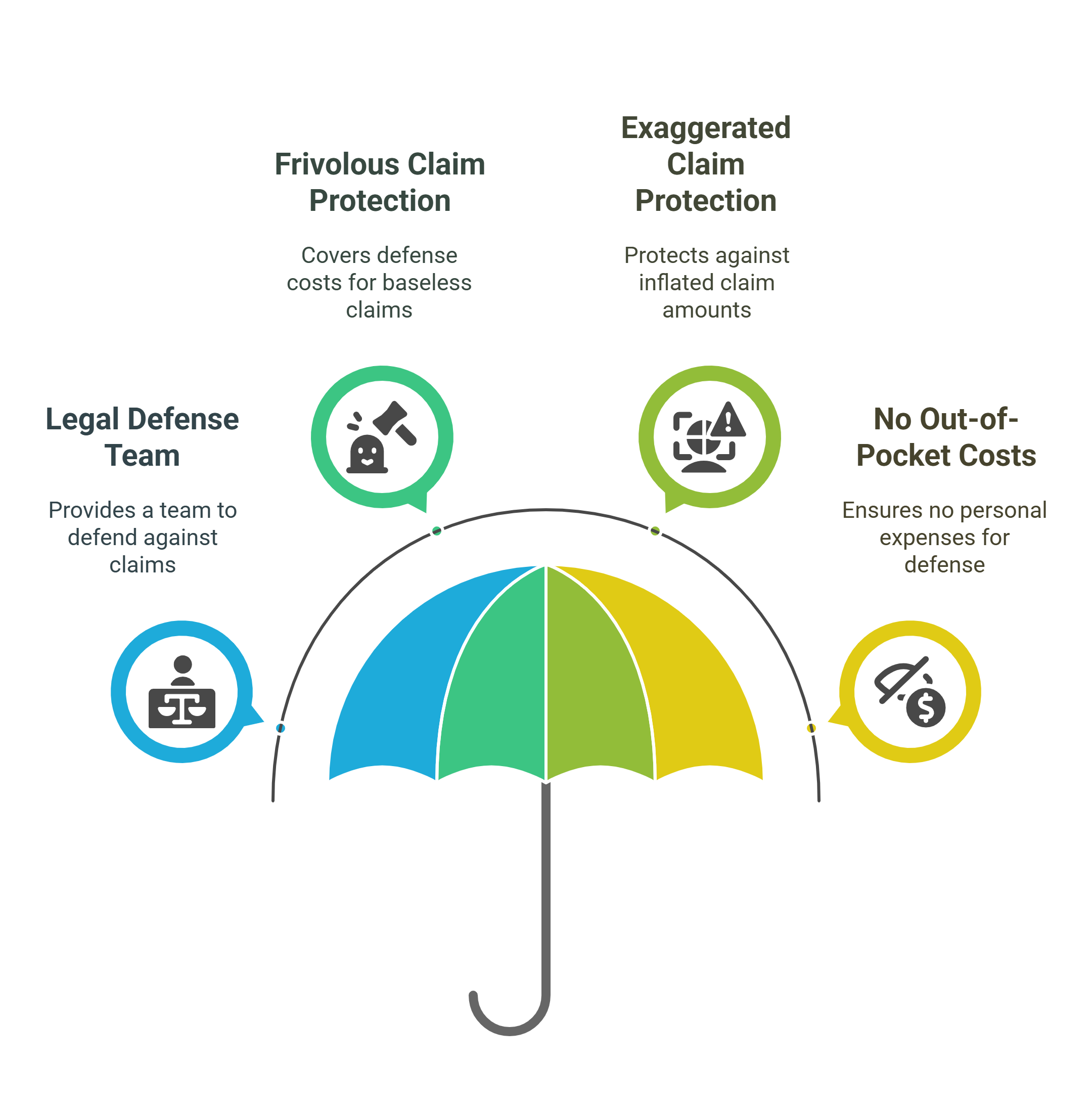

Finally, keep in mind one more thing: legal defense. Umbrella insurance doesn’t just throw money at a problem; it provides you with a defense team. Even if a claim against you is frivolous or exaggerated, you won’t pay out of pocket to fight it – your insurer does.

This is a huge stress relief. Without umbrella (or if you choose to go uninsured for a claim beyond your base coverage), you might have to personally hire lawyers and manage a defense, which is daunting and expensive. That alone is a reason many get umbrella coverage – they want an insurance company’s lawyers on their side if something happens.

A Note on Personal Finance and Peace of Mind

If you determine you do need umbrella insurance, that’s a positive step in fortifying your financial plan. You’re essentially eliminating a big vulnerability. While you’re in this protective mindset, also consider other areas of your financial life where a little effort now yields security or savings later.

For instance, making sure you have a solid emergency fund is important (so you’re not living paycheck to paycheck and can cover smaller unexpected expenses without going into debt). Similarly, think about ways to optimize your finances so you’re getting the most out of what you spend and save.

One simple optimization: use the right tools to ensure you’re not leaving money on the table with everyday spending. Kudos, for example, is a tool that can help maximize your credit card rewards automatically. If you’re paying for insurance or any other bills, using the best credit card for that purchase could earn you additional cash back or points.

Kudos will recommend which card in your wallet to use for a given payment to get the highest reward. Over a year, this can amount to a decent chunk of “free” money just for paying the way you normally do. For someone who’s careful enough to consider umbrella insurance, squeezing extra value from credit card rewards is a natural next step – it’s like ensuring every aspect of your financial life is optimized for benefit and protection.

Also, if you go through the process of getting an umbrella policy, you might get a discount on your other policies (bundling) or realize you should update your coverage on auto/home. It’s a good trigger to do an overall insurance review, making sure you have appropriate coverage all around.

For most people who have worked hard to build any amount of wealth, the answer leans toward yes, you should strongly consider it. The peace of mind and financial protection far outweigh the modest cost. And once you have it, you can go about your life not in fear of what could happen, but confident that you’ve prepared for it.

Frequently Asked Questions (FAQ)

At what point (net worth or assets) should I get umbrella insurance?

A commonly cited point is around $500,000 net worth – at that level, many experts say umbrella insurance becomes essential. However, you might want it even sooner if you have risk factors. Essentially, once you have assets that exceed your base liability coverage (often $300k on home/auto), you should get an umbrella to cover the gap.

Can I skip umbrella insurance if I just increase my auto/home liability limits?

Increasing your base policy limits is a good step, but it may not fully replace the need for an umbrella. Most auto/home insurers max out personal liability at around $500k (some offer $1M on homeowners). Umbrella policies take you beyond that (to $1M+ on top of base).

What happens if I don’t have umbrella insurance and a huge claim hits me?

If you lack an umbrella and a judgment exceeds your insurance, you become personally responsible for the remainder. That could mean selling assets (house, cars, etc.), garnishing your wages (a court can order a portion of your paycheck to go to the plaintiff), seizing bank accounts, and generally financial ruin. You might consider bankruptcy in some cases to discharge a judgment, but note: certain liability judgments (e.g. ones involving intentional harm or DUI accidents) may not be dischargeable.

Does umbrella insurance cover my whole family or just me?

Personal umbrella policies generally cover you (the policyholder) and your immediate household family members for their actions. So if your spouse causes an accident, or your teenage child is liable for something, the umbrella policy would cover those claims just as it would if it were you.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)