Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Does Your Credit Score Affect Your Life Insurance Rates?

July 1, 2025

Credit Scores and Life Insurance Underwriting

When determining your life insurance premiums, insurers look at many factors – and your credit history can be one of them. Your actual FICO credit score isn’t directly used to set your life insurance rate, but the information in your credit report can influence an internal “insurance score” that some life insurers use in underwriting.

In other words, a low credit score by itself won’t automatically raise your premium, but any negative marks behind that low score (like late payments or bankruptcy) might flag you as a higher risk to the insurer.

In recent years, more life insurance companies have started factoring in credit history. A industry survey found the use of credit records in life insurance underwriting grew from 18% of companies in 2017 to 49% in 2019, and over 90% of insurers were either using or considering credit-based scoring by 2018.

The reason? Insurers have found that financial behavior can correlate with insurance risk. They generate a proprietary insurance risk score from your credit report, which helps predict the likelihood you’ll maintain your policy and not present certain risks. This insurance score is not the same as your consumer credit score – it’s a separate metric with a different scale and purpose.

It’s important to note that every insurer treats credit a bit differently. Some major life insurance companies heavily incorporate an insurance score in pricing, while others put little to no weight on credit factors. A few insurers don’t use credit history at all in underwriting.

In states where credit-based scoring is allowed for life insurance (currently most states, since bans on credit use usually apply only to auto/home insurance), each insurer decides how much it matters. That means if your credit isn’t great, you may get different outcomes with different insurers – which makes shopping around important.

Why Insurers May Consider Your Credit

Why do life insurers care about your credit in the first place? Credit history can signal aspects of your reliability and lifestyle that aren’t captured by medical records. Financial stress might indirectly affect health or increase the chance you drop your policy.

By reviewing credit, insurers look for red flags in your financial history that could indicate higher risk:

- Bankruptcy: If you have a recent bankruptcy on file, it suggests severe financial stress. Insurers commonly have rules around this. Others might still offer a policy but at a higher rate to offset the perceived risk.

- High Debt or Credit Card Balances: Owing large amounts can signal financial instability. Insurers worry a high debt burden could make it harder for you to keep up with insurance premiums long-term.

- Late or Missed Payments: A history of late debt payments suggests irresponsibility or cash flow issues. Life insurers see a pattern of missed bills as a potential indicator that you might also miss insurance payments or let your policy lapse.

- Short Credit History or Many Recent Applications: These aren’t as critical, but a very limited credit history or a flurry of recent credit inquiries could slightly lower your insurance score. It might indicate financial uncertainty or that the insurer has less data to trust your financial habits.

Not every company weighs these factors the same. One insurer might be perfectly fine with a high debt load if you have a good income and health, while another might raise your rate for it. There’s no universal standard – each insurer’s algorithm is unique. The key is that major derogatory marks like a recent bankruptcy, accounts in collections, or chronic late payments are the most likely to affect your life insurance offers.

Keep in mind that health and lifestyle factors still play the dominant role in life insurance pricing. Credit is typically a secondary factor. For instance, a person with some credit issues but excellent health may still get a better rate than someone with perfect credit but significant health concerns.

Insurers primarily want to know “how likely is this person to pass away during the policy term?” – that’s why your medical exam, prescriptions, and habits (smoking, etc.) matter most. Credit info is more about financial reliability: it helps gauge if you’ll maintain the policy and avoid fraud. It’s one more data point in a big picture.

How Credit Issues Could Impact Your Rates

If your credit report does have some of the red flags mentioned, how might it translate to your life insurance outcome? It can vary:

- Slightly Higher Premiums: This is the most common impact. You might still be approved for coverage, but an insurer could place you in a slightly less favorable pricing tier.

- Additional Scrutiny or Documentation: An insurer might ask for more information if they see something concerning on your credit report. In some cases, providing an explanation can help the insurer get comfortable.

- Policy Amount Limits: Occasionally, credit history can factor into how much coverage they’ll approve you for. Life insurers assess something called “financial justification” – basically, does the amount of insurance make sense given your income and net worth? If you have a bankruptcy or low credit implying low net worth, an insurer might be hesitant to issue.

- Possible Denial: It’s relatively rare for credit alone to cause a flat-out denial, but it can happen in extreme situations. The clearest example is a recent bankruptcy filing – many insurers will postpone an application until you’re at least 12–24 months past a bankruptcy discharge.

Importantly, if one insurer offers you unfavorable terms due to credit, another insurer might treat you more leniently. There are life insurance companies that focus almost entirely on health factors and give little weight to credit.

Other Factors Matter More Than Credit

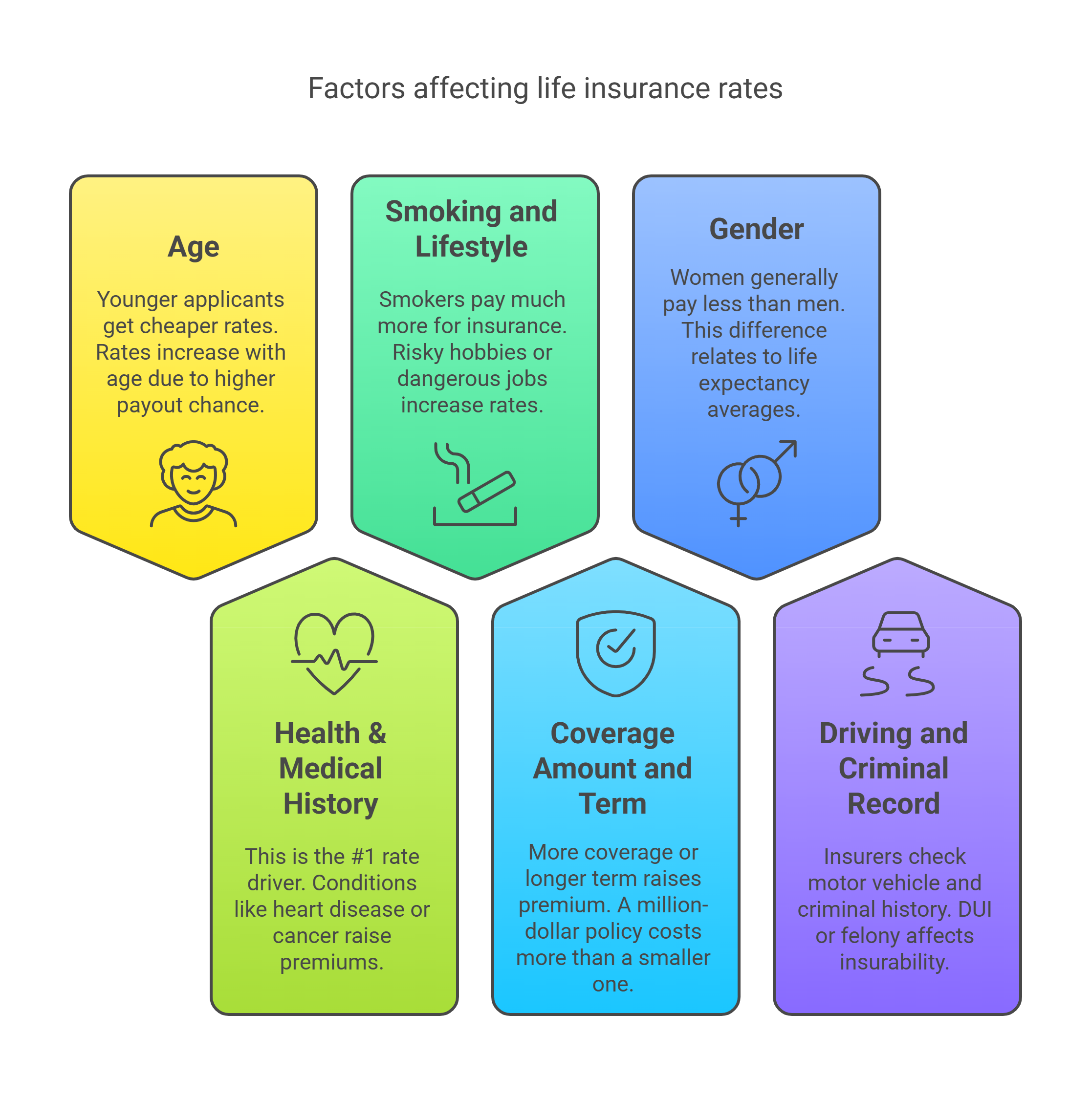

While we’re focusing on credit, remember that many other factors affect your life insurance rates far more substantially. These include:

- Age: Younger applicants get much cheaper rates, all else being equal. Rates increase with age because there’s a higher chance the insurer may have to pay out during the policy term.

- Health & Medical History: This is usually the #1 driver of your rate. Conditions like heart disease, diabetes, or a history of cancer can raise premiums much more dramatically than a credit issue would.

- Smoking and Lifestyle: Smokers often pay 2-3 times more than non-smokers for life insurance. Risky hobbies or dangerous occupations can also increase rates.

- Coverage Amount and Term Length: The more coverage you buy, or the longer the term, the higher the premium. If you choose a $1 million policy for 30 years, it will cost more than a $250,000 policy for 10 years, regardless of your credit.

- Gender: Women generally pay less than men because they have longer life expectancies on average. This difference can be significant and has nothing to do with credit or financial history.

- Driving Record and Criminal Record: Some insurers look at your motor vehicle report and any criminal history. A recent DUI or felony can affect insurability. These checks are separate from credit, but they’re part of the overall risk assessment.

In comparison to these, credit is a supplementary factor. So, if you’re worried that a mediocre credit score will doom your life insurance chances – take heart. If your health and other factors are strong, you’ll still get good offers. On the flip side, stellar credit won’t overcome major health risks; it can only fine-tune an otherwise solid application.

What You Can Do if You Have Bad Credit

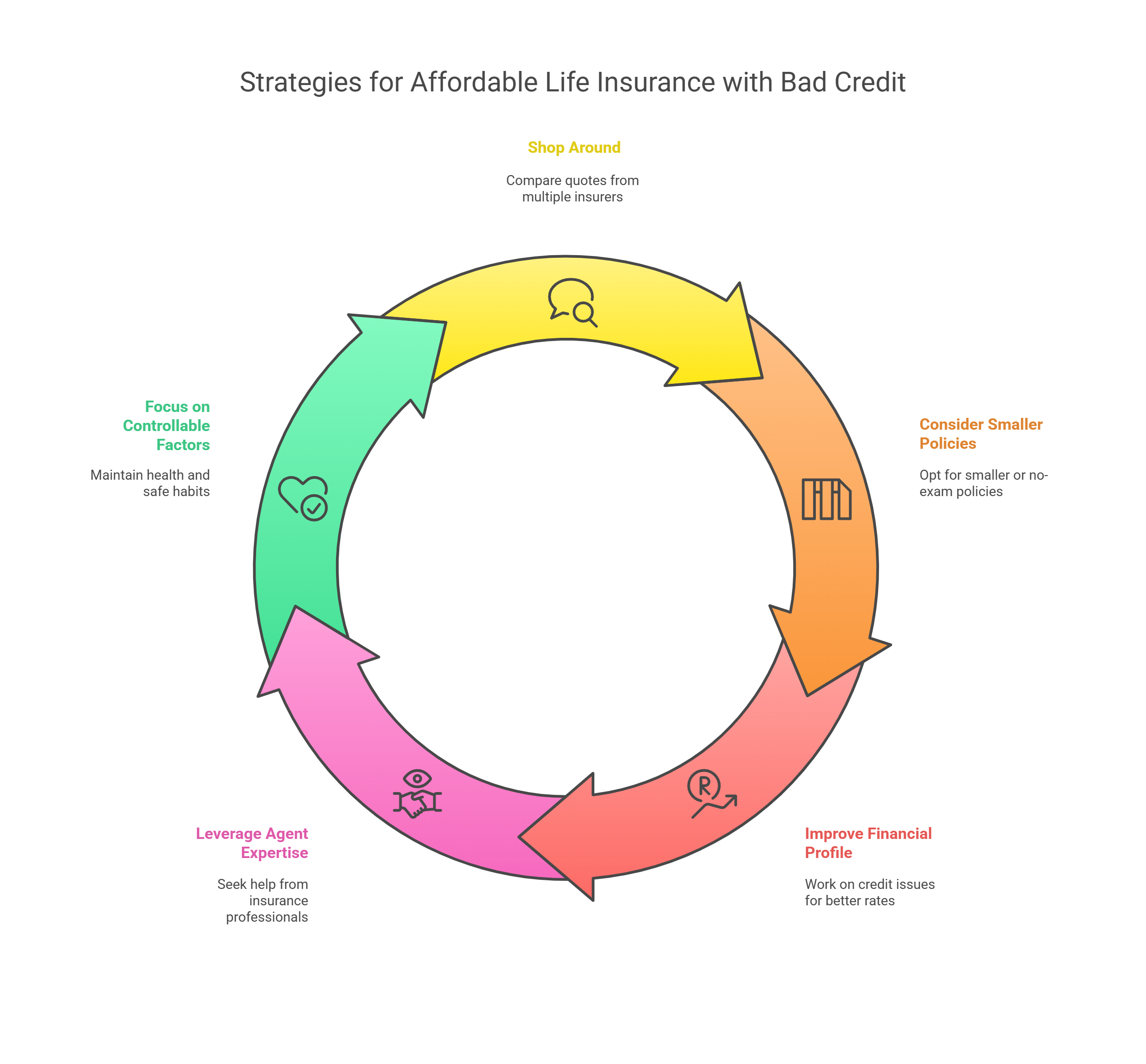

If you do have bad credit right now, there are steps to ensure you still get affordable life insurance:

1. Shop Around with Multiple Insurers

Each life insurance company has its own underwriting “personality.” Some are more forgiving of credit issues. It’s wise to compare quotes from a variety of insurers – or better yet, work with an independent insurance broker who can shop the market for you. A broker will know which companies might overlook a past bankruptcy or weak credit in favor of your strong health, for example.

2. Consider Smaller or No-Exam Policies:

If you’re having trouble due to credit underwriting, one strategy is to buy a smaller policy or a no-medical-exam policy now to get some coverage in place. Many no-exam life insurance policies rely on automated data (including credit) for approval, but they often have slightly higher tolerance for risk. You’ll pay a bit more per thousand of coverage compared to fully underwritten policies, but it can be a way to secure coverage without intensive scrutiny of your finances.

3. Improve Your Financial Profile (Long-Term)

Over time, work on the issues hurting your credit – not just for insurance, but for your overall financial well-being. Pay your loans and credit cards on time, reduce outstanding debts, and avoid new credit obligations if possible. While this won’t instantly change your insurance rate, improving your credit could open up better options down the road.

4. Leverage an Agent’s Expertise

If your situation is complex – say you have a recent bankruptcy plus a medical condition – it’s extremely helpful to use a licensed life insurance agent or broker. They can identify which insurers are likely to consider your application and which to avoid.

5. Focus on What You Can Control

You can’t change your credit past overnight, but you can control other factors that influence your insurability. Make sure you’re doing all you can on those primary factors: keep your health in check, avoid tobacco and substance use, and drive safely. These measures will ensure that health issues, not credit, don’t become the barrier to low-cost life insurance.

Finally, remember that credit is just one piece of the puzzle. Plenty of people with subpar credit scores obtain life insurance at reasonable rates. By being proactive – comparing options and possibly getting guidance – you can turn what might seem like a disadvantage into just a minor footnote in your application.

While you’re reviewing your insurance needs, you might also consider saving on your auto insurance. Kudos simplifies comparing auto insurance rates, quickly finding the best rate tailored for you. It’s easy and completely free.

Frequently Asked Questions (FAQs)

Do life insurance companies check your credit score

Many do perform a credit check as part of the application process, but it’s not the same as checking for a loan. Life insurers often pull a credit-based insurance score derived from your credit report. This helps them assess risk.

Can I be denied life insurance because of a low credit score?

It’s possible but uncommon. Minor credit issues usually won’t result in denial if you are otherwise a good risk. However, major financial problems like a recent bankruptcy can lead to a temporary decline or postponement. Insurers may ask that you wait until the bankruptcy is discharged for a year or two before they approve a policy.

Does bad credit increase life insurance premiums?

It can, but usually indirectly and to a limited extent. Life insurance premiums are primarily driven by health, age, and coverage amount. Bad credit might nudge you into a somewhat higher rate category if the insurer’s model finds your financial history concerning.

Which life insurance companies don’t use credit scores?

Most large insurers do use credit-based scoring now, but a few companies and policy types don’t. Group life insurance never uses credit checks. Some simplified issue or guaranteed issue policies forego credit info, focusing only on health questions.

If my credit improves after I buy a policy, will my life insurance premium go down?

Not automatically. Once your life insurance policy is in force, the premium is locked in for the term. The insurer won’t recheck your credit periodically and adjust your rate if your score goes up or down.

Is an insurance score the same as my credit score?

No, they are different. Your credit score predicts the likelihood you’ll default on a debt. An insurance score, on the other hand, predicts the likelihood that an insurance customer will file a claim or lapse a policy. Insurance scores do use information from your credit report, but they weigh factors differently and have their own scale.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)