Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

How Much Down Payment Do You Need to Buy a House?

For decades, a 20% down payment was considered the gold standard when buying a home. In fact, more than half of Americans still believe you must put 20% down to purchase a house. But is that really true? The short answer: No – you do NOT need 20% down. In today’s market, many buyers – especially first-timers – put down far less.

According to recent data, the median down payment for first-time homebuyers is only about 9%. Some loan programs even let you buy with 0% down if you qualify. So don’t let the 20% myth hold you back from your homeownership dreams. Let’s dig into how much down payment is actually needed, the options available, and what makes sense for your situation.

Minimum Down Payments by Loan Type

The required minimum down payment depends on the type of mortgage you use. Here are common loan types and their minimum down payment requirements:

Conventional Loan (Conforming): 3% – 5% minimum.

Conventional loans typically require at least 5% down. However, there are special conventional programs for first-time or low-to-moderate income buyers that allow as little as 3% down (e.g. Fannie Mae’s HomeReady or Freddie Mac’s Home Possible). So, if you qualify, you can put just 3% down on a conventional mortgage. Keep in mind, with <20% down you’ll pay for private mortgage insurance (PMI), which we’ll discuss more below.

FHA Loan: 3.5% minimum (with credit 580+).

FHA-insured loans require a 3.5% down payment as long as your credit score is 580 or above. That’s $7,000 down on a $200k house – far from 20%. If your score is between 500-579, FHA does ask for a 10% down payment. FHA loans are popular for those with limited savings or lower credit, because of the lenient down payment and credit requirements.

VA Loan: 0% down.

VA loans, available to qualified veterans and active-duty military, do not require any down payment – you can finance 100% of the purchase price. This is an incredible benefit of VA loans. There’s also no PMI requirement, although the VA does charge a one-time funding fee that can be rolled into the loan.

USDA Loan: 0% down.

USDA rural development loans also offer 100% financing with zero down required. These loans are designed for low-to-moderate income buyers in eligible rural areas (and some semi-suburban areas). Like VA, there’s no PMI, but there is a small annual guarantee fee.

Jumbo Loan: 10% – 20% typical.

Jumbo mortgages (above conforming loan limits) usually require larger down payments because of the higher risk. Many jumbo lenders want 20% down, but some will accept 10% – 15% down if you have strong credit and finances. There are even a few jumbo programs allowing 5% down, but those are rare and come with higher rates and PMI-like requirements.

Down Payment Assistance (DPA) Programs:

These aren’t a loan type but worth mentioning – there are numerous local and state programs that can help cover your down payment (often for first-time buyers). DPA can be grants, forgivable loans, or second mortgages that provide funds for your down payment and closing costs. If saving is a challenge, researching DPA in your area can be a game-changer (income and purchase price limits usually apply).

As you can see, the notion that you must have 20% is outdated. It’s possible to buy a home with 3-5% down or even zero down through VA/USDA. In fact, a significant number of homebuyers take advantage of these lower down payment options.

According to the National Association of Realtors, in 2024 the median down payment for all buyers was 13%, and for first-time buyers it was only 9%. That means lots of people are successfully buying homes without anywhere near 20% upfront.

The 20% Down Myth (and Why It Still Matters)

If you don’t need 20% down, why does that number get thrown around so often? The “20% down” idea isn’t a hard rule, but more of a benchmark that comes with certain advantages:

- No PMI with 20% Down: The biggest reason 20% became standard is that traditional lenders waive private mortgage insurance (PMI) once you put at least 20% down on a conventional loan. PMI is an extra insurance fee that protects the lender in case you default. It’s required on conventional loans with less than 20% down. By putting 20% down, you avoid that monthly PMI cost.

- Instant Equity: A 20% down payment means you immediately own 20% equity in your home. That cushion can protect you if home values dip, and it gives you more options (like the ability to tap equity via a loan or line of credit later).

- Lower Monthly Payment: The more you put down, the less you borrow. A larger down payment (all else equal) results in a smaller mortgage and therefore lower monthly payments. This can improve your debt-to-income ratio and make your budget more comfortable.

- More Lender Options: Some mortgage programs (and lenders) do require higher down payments. For example, certain conventional products or jumbo loans might require 10-15% minimum or more. Hitting the 20% mark pretty much guarantees access to any loan product out there and may even fetch a slightly better interest rate in some cases (since the loan is less risky for the lender).

So 20% is not mandatory, but it’s kind of a “sweet spot” that eliminates extra fees (PMI) and potentially strengthens your loan application. It’s understandable many people aim for it. However, as we just covered, plenty of folks buy homes with far less down. The key is understanding the trade-offs and making an informed decision.

If you don’t have 20% down – or choose not to put that much even if you do (more on that later) – you’ll likely pay PMI or another fee. Let’s look at what that entails:

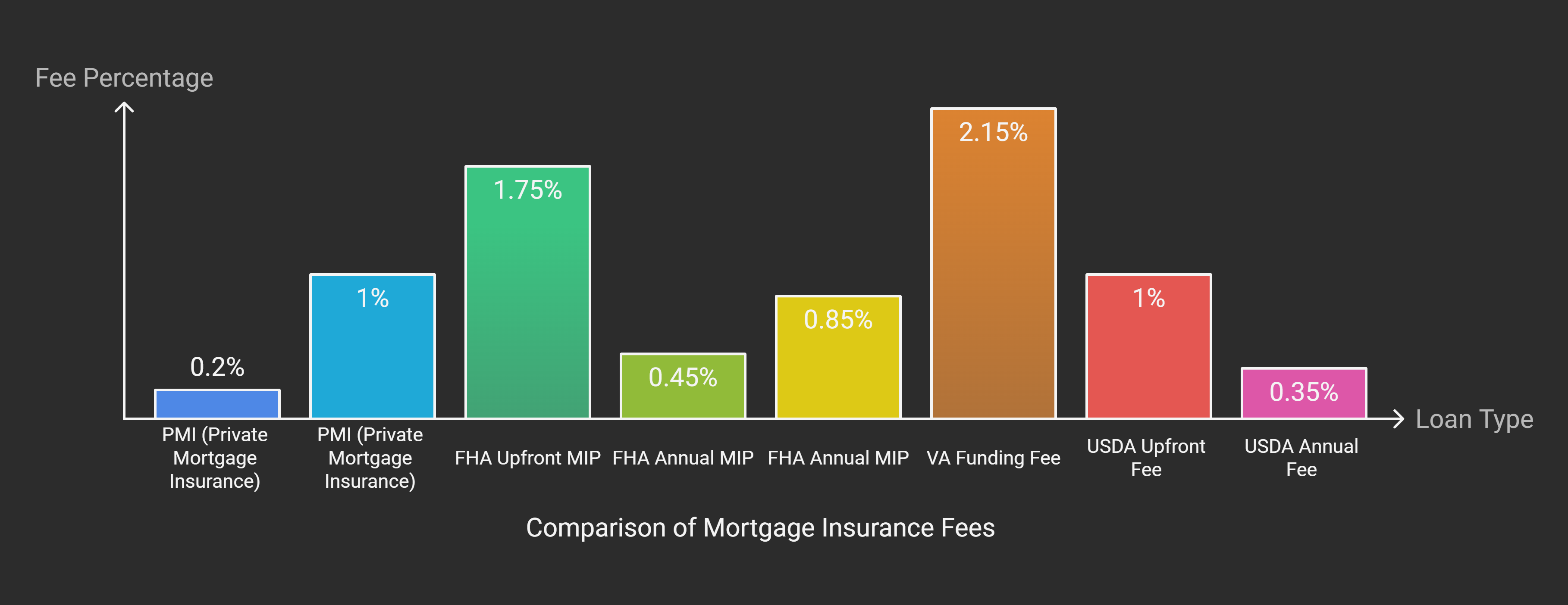

- Private Mortgage Insurance (PMI): On conventional loans, PMI is typically required if your down payment is under 20%. PMI usually costs about 0.2% – 1% of the loan amount per year, depending on your down payment and credit. For example, on a $300,000 purchase with 5% down, you might borrow $285,000 and pay around $100-$200/month in PMI.

- FHA Mortgage Insurance: FHA loans don’t have PMI, but they have their own mortgage insurance premiums (MIP). FHA requires an upfront MIP (1.75% of the loan amount, usually added to the loan) and an annual MIP around 0.45% – 0.85% of the loan, which is split into your monthly payments. If you only put 3.5% down, you’ll pay the higher end of that range.

- VA Funding Fee / USDA Fee: VA loans have no monthly PMI, but they do have a funding fee (unless exempt) which can be 2.15% (first-time use, zero down) or higher for subsequent use or if putting some money down. USDA loans have a 1% upfront guarantee fee and a 0.35% annual fee.

The takeaway: Putting less than 20% down is very doable, but budget for the extra insurance costs and slightly higher payment. It’s a trade-off – you can become a homeowner sooner, but you carry an added expense until you build enough equity.

Pros and Cons of a Larger vs. Smaller Down Payment

Deciding how much to put down is a personal decision that depends on your finances and comfort level. Let’s weigh the advantages and disadvantages of different down payment sizes:

🔑 Benefits of a Larger Down Payment (10% – 20% or more):

- Lower Monthly Payments: As mentioned, more down = less principal and interest to pay back. This can save you a lot in interest charges over 30 years. For example, a $250k loan vs. a $270k loan (because you put $20k more down) can mean thousands saved in interest.

- Avoiding or Reducing PMI: Hitting 20% down avoids PMI entirely on conventional loans. Even if you can’t do 20%, higher down payments often mean lower PMI rates. On FHA loans, putting 10% down shortens how long you pay annual MIP (11 years instead of lifetime).

- Competitive Edge in Bidding: In a hot housing market, sellers often favor buyers with larger down payments, seeing the offer as more secure (less financing risk). Your offer might stand out if you can put more down, especially compared to someone using a 3% down program.

- Instant Equity & Safety Net: A bigger equity cushion protects you if the market fluctuates. If home prices dip after you buy, you’re less likely to owe more than the home is worth (be “underwater”) if you made a substantial down payment. This was a big issue for those who bought with tiny down payments before the 2008 housing crash.

- Better Mortgage Rates: This one is situational – generally, interest rates are more influenced by credit score and loan type. But sometimes lenders offer a slightly better rate for, say, 25% down vs 5% down on a conventional loan, because the loan is less risky. The difference isn’t huge, but it can exist.

🔑 Benefits of a Smaller Down Payment (under 10%):

- Buy Sooner: The biggest advantage is time. If you don’t have to wait years to save 20%, you can become a homeowner sooner and start building equity through appreciation and principal pay-down. Home values and rents might rise while you’re saving – buying earlier locks in today’s price.

- Keep Cash for Emergencies or Improvements: Draining your savings for a huge down payment can leave you “house poor.” With a smaller down, you preserve savings for repairs, home improvements, or an emergency fund once you move in. Houses come with surprise expenses – it’s wise to have reserves.

- Opportunity Cost: Money tied up in your home is illiquid. If you have other investment opportunities (or even to pay off higher-interest debt), putting every spare dollar into a down payment may not be the best financial move. For instance, if you can secure a 3% down mortgage at a low rate and invest extra cash in the stock market or your 401(k), you might earn more over time.

- Qualification: If you’re using an FHA or VA loan with low down, those programs can be more flexible with credit or debt ratios. It might be easier to qualify for a loan with a smaller down payment program if your financial profile isn’t perfect. Also, some down payment assistance loans require you to put the minimum down (they cover the rest) – taking full advantage of those programs means you’re not putting more of your own money than necessary.

- Inflation Benefits: In an inflationary environment, a mortgage lets you pay back the loan with “future” dollars that are worth a bit less. The less of your own money you put in upfront, the more you benefit from essentially borrowing at a fixed cost and letting inflation and home price appreciation work in your favor. This is an abstract benefit, but it has proven true over time as home values generally rise.

In summary, a big down payment buys you peace of mind and cost savings, whereas a small down payment gets you the keys sooner and keeps your cash free for other needs. There is no one-size-fits-all answer. It depends on your savings, income stability, and financial goals.

Finding the Right Down Payment for You

So, how do you decide what you should put down? Here are some guidelines and tips:

1. Assess Your Finances:

Take a close look at your savings and monthly budget. How much can you afford to put down without wiping out your emergency fund? Remember you’ll also need cash for closing costs (usually 2-5% of the purchase price) and moving expenses. It’s generally recommended to keep at least 3-6 months of expenses in savings after your home purchase for emergencies.

2. Consider PMI Impact:

Get quotes on the PMI if applicable. Sometimes PMI on a 5% down loan might be, say, $150 a month – which could be acceptable if it means getting the house sooner. Also remember PMI isn’t permanent. You can plan to refinance or remove PMI in a few years once you have enough equity (via paying down the loan or home price appreciation).

3. Think About Home Price Trajectory:

In a rapidly rising market, buying sooner with a small down payment might save you money as prices increase. In a flat or falling market, a larger down payment provides protection against declining equity. Research your local market or ask your real estate agent for insight.

4. Avoid Over-Stretching:

It can be tempting to empty your bank account to hit 20%, but doing so might leave you vulnerable. Make sure after down payment and closing, you have a cushion for unexpected home repairs (the water heater will inevitably break in the first year 🙃). Also, don’t forget you’ll need some cash for furnishings, utilities startup, and possibly a few new pieces of furniture when you move in.

5. Use Gift Funds or Assistance if Available:

If family is willing to help, many loans allow gift money toward down payment. Just be sure to follow the lender’s rules for documenting it (a gift letter, etc.). Likewise, if you qualify for a down payment assistance grant or loan, take advantage of it. That can effectively increase your down payment without draining your own funds. Free money is great – just understand any conditions attached (like living in the home for a certain number of years).

Finally, it may help to use a down payment calculator to play with numbers. For example, input different down payment amounts and see how they affect your monthly payment and total interest paid. This can clarify the long-term cost of, say, 5% down vs 10% vs 20%.

If you’re a first-time buyer feeling overwhelmed, remember that many people buy homes with modest down payments. Lenders and programs are out there to facilitate this. Just be sure to plan for the added monthly costs (PMI, slightly higher payment) and don’t neglect other aspects of homeownership prep – like keeping your credit score strong (your rate depends on it) and avoiding new debt.

Pro tip: While you’re saving up, consider using a cashback credit card for regular expenses to earn a little extra money toward your house fund – just pay it in full each month. A tool like Kudos can help you maximize those rewards by telling you which card to use for each purchase. Every bit of cashback or points can go into your “new house” piggy bank!

FAQ: Down Payments and Home Buying

Do I really need a 20% down payment to buy a home?

No. 20% is not a requirement, just a recommendation from the past. In reality, you can buy a home with far less down. Many conventional loans allow as little as 3-5% down, FHA loans need only 3.5%, and VA/USDA loans require zero down payment.

What are the disadvantages of putting 0% to 5% down?

The main drawbacks of a very low down payment are: higher monthly costs (due to PMI or mortgage insurance fees), little immediate equity in the home, and potentially higher interest rates. With 0-5% down, you have almost no equity buffer – if home values dip, you could owe more than the home is worth. You’ll also have to budget for PMI.

Can I use gift money or borrowed money for a down payment?

Gift money – yes. Most loan programs allow family members (or even close friends) to gift you money for the down payment. You’ll need a signed gift letter stating the funds are a gift, not a loan. Lenders will want to see the paper trail (the money moving from the giver’s account to yours). Borrowed money – generally no for the down payment itself. You typically can’t take out a personal loan or use a credit card advance for down payment; such borrowed funds won’t be counted as “your” funds.

What is PMI and how long do I have to pay it?

Private Mortgage Insurance (PMI) is a protective insurance for the lender when you put less than 20% down on a conventional loan. It’s an extra fee added to your monthly mortgage payment. PMI does not pay your mortgage if you can’t; it only reimburses the lender if you default. The cost can range from 0.2% to 1% of the loan per year depending on your down payment and credit score. On a $250,000 loan, that might be roughly $40 to $200 per month. You don’t have to pay PMI forever. Once your loan-to-value (LTV) hits 80%, you can request the lender cancel PMI.

Is it okay to use all my savings for the down payment?

It’s generally not advisable to empty your savings for a down payment. While putting more down can reduce your mortgage costs, you don’t want to be cash-strapped after closing. Homeownership comes with many surprise expenses – repairs, maintenance, higher utility bills, etc. If you use all your cash on the down payment and closing costs, you could be in a tough spot if an emergency comes up. Most experts recommend keeping an emergency fund of 3-6 months’ expenses aside, even after paying your down payment.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)