Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

United MileagePlus® Debit Card: Everything We Know So Far (and How It Stacks Up Against Credit Cards)

July 1, 2025

.webp)

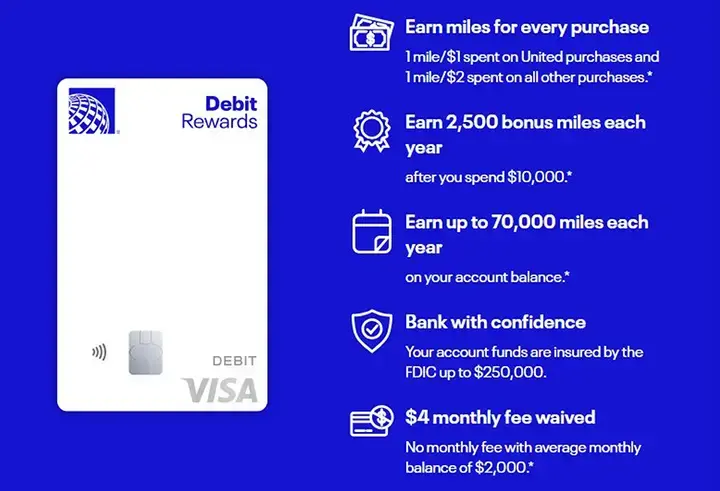

What’s in the Works: United MileagePlus Debit Rewards

Based on leaked details, United’s debit card would:

- Earn 1 mile per $1 on United purchases

- Earn 1 mile per $2 on all other purchases

- Charge a $4 monthly fee, waived with a $2,000 average balance

- Include a 2,500-mile annual bonus for $10,000 in yearly spend

- Cap total earnings at 70,000 miles per year

- Will be issued by Sunrise Banks N.A. and powered by SoFi Galileo

💡 For context: at 1 mile per $2, $10,000 in spend earns just 5,000 miles — roughly $50 in flight value.

How It Compares to the Southwest Debit Card

Southwest’s new Southwest Rapid Rewards Debit Card follows a similar playbook to United’s rumored product. Both are issued by Sunrise Banks N.A., offer FDIC insurance up to $250,000, and target customers who want to earn airline rewards without using a credit card. The main differences come down to network, fees, and structure.

The United MileagePlus® Debit Rewards Card is expected to run on the Visa network, while the Southwest Debit Card runs on Mastercard. United’s version will reportedly charge a $4 monthly fee, waived with a $2,000 balance, whereas Southwest’s card carries a slightly higher $5 fee, waived with a $2,500 balance.

Earning rates are nearly identical. United will likely earn 1 mile per $2 spent on everyday purchases and 1 mile per $1 on United flights. Southwest’s debit card mirrors that setup with 1 Rapid Rewards point per $2 spent and 1 point per $1 on Southwest purchases. United’s card includes a small 2,500-mile annual bonus after $10,000 in spending, while Southwest has yet to announce any welcome or anniversary bonuses.

In short, both debit programs are designed for customers who can’t or don’t want to use credit cards. They provide a way to earn modest rewards on debit purchases, but they trade flexibility and earning potential for simplicity.

[[ SINGLE_CARD * {"id": "21302", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Southwest Loyalists", "headerHint" : "1x at Southwest" } ]]

United Debit vs. United Credit Cards

While the rumored United MileagePlus® Debit Rewards card adds another option for earning United miles, it’s far less rewarding than United’s existing co-branded credit cards.

The United debit card is expected to earn just 1 mile per $1 on United purchases and 1 mile per $2 everywhere else, plus a 2,500-mile bonus after $10,000 in annual spend. That means if you spend $500 on groceries, you’d only earn 250 miles, roughly a single short-haul redemption mile.

Even with the $4 monthly fee waived for balances over $2,000, the effective return rate is minimal. By contrast, United’s Chase-issued credit cards deliver stronger earning power and valuable travel perks that debit cards simply can’t match.

For example:

- The United℠ Explorer Card offers 2x miles on United purchases, dining, and hotels, plus a free first checked bag and two one-time United Club passes each year.

- The United Quest℠ Card earns 3x miles on United purchases, 2x on dining and streaming, and two 5,000-mile anniversary credits that effectively offset part of its annual fee.

- The United Club℠ Card adds United Club lounge membership, Premier Access, and free first and second checked bags, benefits worth potentially thousands annually.

Beyond rewards, credit cards also offer consumer protections that debit cards lack, including trip cancellation insurance, rental car coverage, and purchase protection. Those benefits can save you significant money if travel plans change or items are lost or damaged. If your goal is to maximize United miles and travel benefits, a United credit card is the clear winner.

The debit version might make sense only for users who can’t or prefer not to open a credit line but still want to passively earn miles on everyday spending.

[[ SINGLE_CARD * {"id": "2406", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Priority Boarding"} ]]

[[ SINGLE_CARD * {"id": "2892", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Frequent Travelers", "headerHint" : "Mid-Tier Choice Card" } ]]

[[ SINGLE_CARD * {"id": "2410", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "United Loyalists", "headerHint": "Top-Tier Card"} ]]

Who the Debit Card Is (and Isn’t) For

Best For:

- Users who want to avoid credit checks

- Loyal United flyers with checking balances over $2K

- Consumers seeking FDIC insurance and debit-based rewards

Skip It If:

- You already have a travel rewards credit card

- You’re working toward elite status or free bags

- You prioritize earning flexibility

If you can’t qualify for a credit card yet, this debit card could bridge the gap, letting you earn while building a relationship with United. But if your goal is maximizing rewards value, pairing a United credit card with a cash-back debit option like the Southwest debit card or Fidelity Rewards Checking will deliver stronger returns.

How the Value Adds Up

Let’s put the numbers into perspective. If you spend about $12,000 per year on everyday purchases with the rumored United MileagePlus Debit Card, you’d earn roughly 6,000 miles, which translates to around $90 in flight value (assuming each mile is worth 1.5 cents). Add another $5,000 in United flight purchases, and you’d pick up about 5,000 more miles, or roughly $75 in value. That means your total annual earning potential is about 11,000 miles, or $165 in total rewards value, assuming you maintain a high enough balance to avoid the monthly fee.

By comparison, a United Explorer Credit Card or similar product could easily double or even triple that value. The same $17,000 in spending would earn around 17,000 to 25,000 miles, depending on category bonuses, worth $330 or more in travel. And that doesn’t include welcome offers, free checked bags, travel protections, or lounge passes, which can add hundreds more in yearly perks.

In short, even if the debit card offers a convenient, no-credit-check way to earn miles, it delivers only a fraction of the value of United’s co-branded credit cards.

Should You Apply?

Yes, if you can’t qualify for a credit card, and want to passively earn miles on debit spend. No, if you already hold or can qualify for a travel rewards credit card. The United Explorer or Chase Sapphire Preferred® Card) will outperform this debit product on nearly every metric.

[[ SINGLE_CARD * {"id": "509", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Exceptional Travel Value"} ]]

Final Take: A Step, Not a Game-Changer

United’s rumored MileagePlus Debit Card expands access for everyday earners, but the math doesn’t work out for most travelers. At best, this is a low-value entry point into rewards for those rebuilding credit or avoiding debt. For everyone else, credit cards remain the smarter path to meaningful travel value, elite perks, and protection coverage.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)