Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

5 Best Store Credit Cards in 2026 and How to Use Them Responsibly

July 1, 2025

.webp)

Store credit cards can be hit or miss – some offer great value, while others gather dust in your wallet. Here we highlight five of the best store credit cards of 2025, the ones with solid perks that stand out from the pack. More importantly, we’ll give you tips on how to use each card responsibly, so you can enjoy the rewards without the regret.

1. Prime Visa – Best for Online Shopping & Everyday Use

Why It’s Great:

[[ SINGLE_CARD * {"id": "79", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Amazon Shoppers", "headerHint": "Impressive Rewards and Benefits"} ]]

Using It Responsibly:

Despite being one of the best, you should still follow good habits. Pay the balance in full each month – this card’s APR is variable, which is lower than many store cards but still high enough to warrant caution. Since it’s easy to overspend on Amazon, set a budget for yourself. Perhaps use Amazon’s own tools like “budgets” on categories or load gift card balance as a way to control spending.

2. Target RedCard (Target Circle Mastercard or Store Card) – Best for Everyday Discounts at a Major Retailer

Why It’s Great:

The Target RedCard is a favorite for families and deal-hunters. It comes in two forms – a store-only card or a Mastercard – but both give the core benefit: 5% off all purchases at Target and Target.com, every day. This 5% discount is applied instantly at checkout, which is satisfying and straightforward.

Additionally, RedCard holders get free 2-day shipping on Target.com, no minimum, and an extra 30 days for returns. There are also occasional Target Circle bonus offers just for RedCard users, and 5% off in-store Starbucks cafes (nice perk for coffee lovers). No annual fee, of course. Target is a one-stop-shop for groceries, household goods, clothing, and more – so 5% off on your weekly essentials is a big win over time. It’s like having permanent sale pricing.

Using It Responsibly:

The RedCard’s 5% off is awesome, but don’t let it trick you into overspending at Target. It’s easy to load your cart with extras because “hey, I get 5% off.” Stick to your list! Always pay your RedCard bill in full; the Target RedCard’s interest rate is around 22.9% variable, which is slightly lower than some store cards but still not something you want to pay. If you have the debit card version, it pulls from your bank, so ensure you track those transactions.

One great strategy: since the 5% is automatic, you can combine the RedCard with Target Circle offers (the app’s coupons) and even manufacturer coupons – triple stack savings. There’s no special financing or anything to worry about here, which simplifies use. Just remember: only use the RedCard at Target.

The store version won’t work elsewhere; the Mastercard version will, but you only get 1% off outside Target, so it’s better to use a different card for non-Target shopping. By confining the RedCard to Target runs and paying it off, you’ll maximize its benefit with minimal risk.

[[ SINGLE_CARD * {"id": "2257", "isExpanded": "false", "bestForCategoryId": "52", "bestForText": "Frequent Target Shoppers", "headerHint" : "Simplified Rewards" } ]]

Capital One Walmart Rewards® Mastercard® – Best for Walmart Shoppers & More Versatile Rewards

Why It’s Great:

The Capital One Walmart Rewards® Mastercard® gives you robust rewards both in and out of Walmart. You earn 5% back on Walmart.com purchases, including grocery pickup and delivery orders, 2% back in Walmart stores, and 2% on restaurants and travel, plus 1% elsewhere. (Note: For the first 12 months, you also get 5% back in Walmart stores if you use Walmart Pay – an incentive to promote mobile wallet usage.) There’s no annual fee.

This card is especially lucrative for those who use Walmart’s online ordering (5% is great) or who shop in-store often (effectively 2% back there, which combined with Walmart’s low prices is nice). The inclusion of restaurants and travel at 2% means it has some general spending value too. Rewards are issued as points redeemable for statement credits, gift cards, or during online checkout. The versatility and relatively high earn rates make the Walmart Rewards Mastercard stand out among retail cards (it competes with some general cash back cards).

Using It Responsibly:

The Walmart card is a Mastercard, so keep an eye on where it’s best to use it. Ideally, use it for Walmart purchases (especially online) and when dining out or traveling if you don’t have another card that gives more than 2% on those. Don’t be lured into using it everywhere just because you have it – if you have a 2% everywhere card, that might be simpler for “everything else.” As always, pay it off to avoid interest (its APR can range, often in the low-mid 20% range).

Another tip: Walmart often offers special financing on big purchases (like 0% for 6-12 months on electronics) or the 5% back – usually you have to choose one. I’d lean towards taking the 5% back and avoiding financing unless absolutely needed, because the 5% is straightforward and you’re not risking a deferred interest scenario.

The card’s mobile app integration is good (Capital One), so use that to track your rewards and payments. Lastly, because this card can overlap with everyday spending categories, using a tool like Kudos can help ensure you maximize it – for instance, Kudos might remind you that your Walmart card gets 5% on Walmart.com so you don’t accidentally use a different card online, or conversely remind you to use a better card at a department store instead of the Walmart card. By staying mindful, you can let this card pay you back nicely for all those Walmart trips.

[[ SINGLE_CARD * {"id": "421", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Walmart Shopper", "headerHint": "Maximum Rewards"} ]]

4. My Best Buy® Credit Card (Citibank) – Best for Electronics & Appliance Shoppers (Financing Offers)

Why It’s Great:

Best Buy actually offers two versions: a store-only card and a Visa, but here we’ll talk about the core My Best Buy Credit Card program. Cardholders get a choice on most purchases: 5% back in rewards (i.e., 2.5 points per $1, with 250 points = $5 certificate) – that’s the equivalent of 5% – or special financing on eligible purchases (e.g., 6, 12, or 18-month no interest plans depending on amount). If you’re an Elite Plus member (very high spending), you get 6% back.

There are also occasional extra point events for cardmembers. This is a great card if you frequently buy electronics, gadgets, or appliances. The 5% back essentially makes it on par with Amazon’s card for electronics purchases, and sometimes Best Buy’s prices are the same or better. No annual fee unless you opt for a version with an annual fee that gives you flexible financing + points (most people choose the no-fee).

Using It Responsibly:

My Best Buy® Credit Card is one where you must be disciplined if you use the financing offers. Best Buy uses deferred interest on those “No interest if paid in full” deals. So only opt for special financing if you have a clear payoff plan. If you’re not sure, take the 5% back in points instead – it’s safer value. When you take 5% back, watch your points and certificates: Best Buy rewards certificates can expire relatively quickly.

Redeem them when they’re issued so you don’t lose them. Maybe set a reminder or use them on small accessories. If you’re a tech enthusiast, it might be worth it, but don’t let points expire – that’s wasted money. Also, because it’s easy to splurge in an electronics store, try not to impulse-buy just because you have the card. Make a shopping list or a 30-day wish list for pricey items to ensure you really want/need them.

As with others, pay the card off monthly; the APR is high (around 25%+). Another tip: Best Buy price matches many competitors. Having the card means you can still get 5% back on the matched lower price – double win. And if you’re also an online shopper, weigh your options: sometimes the Amazon 5% (if you have Prime Visa) vs Best Buy 5% – go for the retailer with the better deal or warranty, etc., since rewards rate is equal. In short, use the Best Buy card for planned electronics purchases, don’t carry a balance, and monitor those reward certificates so every point counts.

[[ SINGLE_CARD * {"id": "1301", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Best Buy Shoppers", "headerHint": "Generous Cash Back"} ]]

5. Lowe’s Advantage Card – Best for Home Improvement & Big Project Financing

Why It’s Great:

Homeowners and DIY enthusiasts love the Lowe’s Advantage Card. Its marquee benefit is 5% off on nearly all purchases at Lowe’s, every day (similar to the Target model). This includes in-store and Lowes.com purchases on eligible items. Alternatively, cardholders can choose special financing on purchases $299 and up: either six months deferred-interest financing on any $299+ purchase or sometimes fixed payments on larger project amounts (e.g., 0% interest if paid in 24 months on $~, or reduced APR with fixed payments for 4-year plans on really big installs).

There’s no annual fee. 5% off on home improvement supplies, appliances, tools, etc. can mean huge savings if you’re renovating or have a big project – those expenses add up fast. Lowe’s 5% off can even apply to gift cards for certain services or other products they sell in store, which some hacky customers utilize. It also stacks with most seasonal sales (unless stated otherwise). Considering many general cards would give 1-2% back on home improvement, a straight 5% discount is strong.

Using It Responsibly:

The Lowe’s card should be used much like the Target RedCard: for all your Lowe’s purchases, but not beyond. Don’t let the availability of financing make you overshoot your budget. If you opt for a financing deal, read the fine print – Lowe’s usually does deferred interest on the 6-month plan (no interest if paid in full in 6 months on $299+, which you should pay off to avoid back interest), or they have special longer-term options occasionally with reduced APR.

If you go the 5% off route (which is often best for smaller purchases), that discount happens at purchase, so you can still pay off immediately or when the statement comes. Always pay on time (Lowe’s/Citi will charge late fees and you could lose your promo rate if you pay late). Also, keep your Lowe’s card usage to home improvement needs – it’s easy to justify a splurge on a new grill or patio set by thinking “I get 5% off!” Make sure it fits your plan.

A good practice if you’re doing a big home project is to use the 5% off card in combination with Lowe’s 0% in-store installment offers on appliances, etc., if they allow both (sometimes they don’t allow 5% if you choose financing – you have to pick). Often, I recommend taking the 5% immediate savings and using a separate 0% APR credit card (like a bank-issued one) if you need to finance, because then you effectively get both.

Lastly, track your spending – home projects can rack up, so keep an itemized list. The Lowe’s card can save you a lot, but only if you don’t let interest or overspending creep in. And as always, pay that bill in full or within the promo period.

[[ SINGLE_CARD * {"id": "1162", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Lowe Purchasers", "headerHint" : "Closed-Loop Card" } ]]

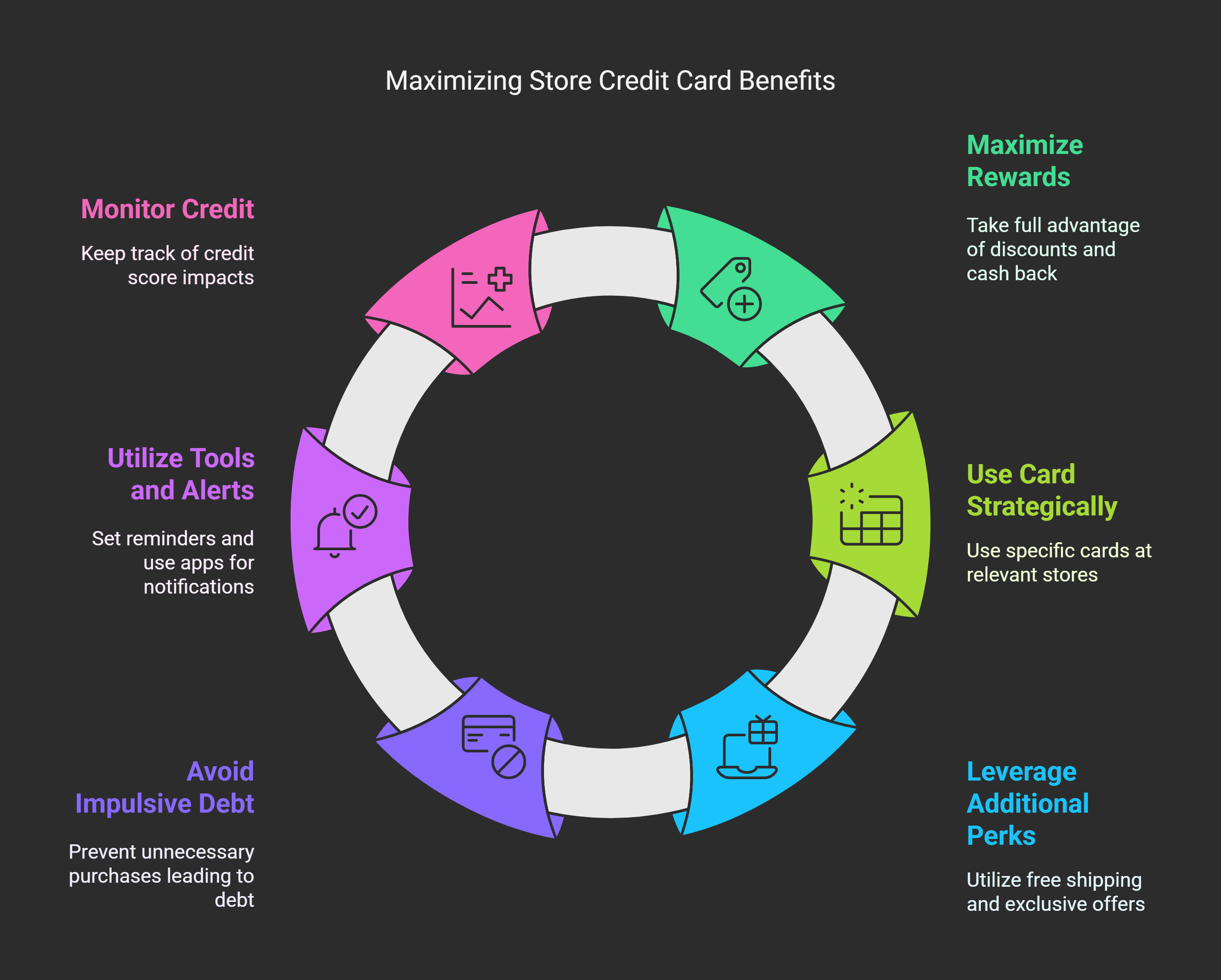

Responsible Card Use: A Recap for All Store Cards

All of the above “best” store credit cards share common threads in responsible use:

- Maximize rewards, minimize interest: Take full advantage of the discounts/cash back, but never carry a balance to avoid high APR charges.

- Use the card where it makes sense: Use the Amazon card at Amazon, Target card at Target, etc. For other purchases, use a general card that gives you more back.

- Leverage additional perks: Free shipping, extended returns, exclusive offers – use them! That’s extra value.

- Avoid impulsive debt: Don’t let the card push you to buy more than you need. A deal isn’t a deal if it gets you into debt for unnecessary stuff.

- Utilize tools and alerts: Set calendar reminders for promo financing deadlines. Use the issuer’s app for notifications. Consider using Kudos or a similar tool to remember which card to use (say you have both Amazon and Lowe’s cards, Kudos will remind you to use Lowe’s card on Lowes.com and Amazon card on Amazon – preventing mix-ups).

- Keep an eye on your credit: Having multiple store cards can affect your credit score (each one is an inquiry and a tradeline). If you’re going for top-notch credit or planning a big loan, don’t open all of these at once – space them out or only stick to one or two that really serve you.

By choosing one of these top store cards that aligns with your shopping patterns, and following the usage tips, you can reap significant rewards in 2025. These cards made the “best” list because their perks are above and beyond the typical store card – just remember that with great rewards comes the responsibility to manage them wisely. Happy saving, and enjoy those rewards!

FAQ: Picking and Using Store Credit Cards (Top 5 Edition)

Is 5% back (or off) the standard best rate for store cards?

Yes, 5% is a common generous reward rate among the top store cards (Amazon, Target, Lowe’s all use 5%). It’s kind of the gold standard – very few store cards go above 5% in a straightforward way. Some might effectively do more during special promos or for higher-tier members (Macy’s has tiers up to 5% in rewards plus extras, Kohl’s can exceed 5% during stackable coupon events), but as a baseline, 5% is what the best ones offer.

Keep in mind, 5% back in rewards vs 5% off can feel different: 5% off (Target, Lowe’s) is instant and guaranteed, while 5% back (Amazon) you have to redeem later. Both are valuable. Also, outside the store, some co-branded cards give elevated rewards (the Costco Visa’s 4% on gas, for example, or Amazon’s 2% on dining). But generally, 5% at the store is the peak for everyday earnings.

What credit score do I need to get these top store cards?

It varies by card:

- Prime Visa: Typically requires good credit (think FICO 670+). Being a Visa by Chase, they look for a decent score and history.

- Target RedCard: Surprisingly, the Target store card is often accessible to fair credit (600ish scores), whereas the Target Mastercard version goes to those with better credit after showing good use. Many people with limited credit have gotten the RedCard.

- Walmart Mastercard: Requires at least fair-good (maybe 640+). Capital One will consider those with a decent track record, but it’s not as easy as some store cards.

- Best Buy Card: They have multiple versions; people with fair credit might get the store-only version, while those with good credit get the Visa. Ideally mid-600s or higher for approval, but Citi store cards can sometimes approve lower with a low limit.

- Lowe’s Advantage: Often needs fair to good (around 640+). Synchrony (previous issuer) and now Citi look for a reasonable score, but people with limited credit history have been approved at times.In summary, for the best odds on these top cards, aim for a credit score in the mid-600s or above. If you’re lower, Target and maybe Lowe’s are slightly more lenient. Also, having a history with the store (e.g., using their loyalty program) doesn’t hurt but formal applications are mostly credit-score driven.

Can I have multiple store cards without hurting my credit?

You can, but you should be cautious. Each new card you open adds a hard inquiry and reduces your average account age, which can cause a temporary dip in your credit score. If you open, say, three store cards in a short span, that’s three inquiries and three new accounts – a credit score could drop some points because of that. However, if you manage them well (no late payments, low utilization), over time they can contribute positively by increasing your total available credit and showing good payment history. The key is not to go overboard at once and not to max them out.

Also, note that some issuers might be wary if you have too many new accounts. For example, if you opened a bunch of store cards and then apply for a prime credit card, the issuer might see you as higher risk due to multiple recent accounts. In short: yes, you can have multiple, and many people do (for different favorite stores), just space out applications (maybe a few months apart), and keep your credit healthy on all of them.

Among these best cards, which one should I get first?

It depends on where you spend the most. Think about your shopping habits:

- If you’re an Amazon Prime member and frequently order online, the Amazon Prime Visa might be the most broadly useful (since it’s great at Amazon and solid elsewhere).

- If you practically live at Target for groceries, household stuff, etc., the RedCard could save you a steady 5% on a big chunk of your budget.

- For a mix of everyday categories plus Walmart shopping, the Walmart Mastercard is well-rounded.

- If you have major electronics purchases or love tech, the Best Buy card could be valuable (especially for financing).

- If you’re a homeowner tackling projects, the Lowe’s card first could save you hundreds on renovations.In essence, choose the card for the store where you currently spend the most money (or plan a large purchase). That’s your low-hanging fruit for savings. Also consider credit requirements: if your credit is only fair, maybe Target (store card) or Lowe’s might be easier initial picks than Amazon (which likes good credit). Over time, you can add another if needed. But there’s no need to get all five – focus on the one or two that align with your lifestyle.

How do I keep track of multiple store card rewards and payments?

Juggling multiple cards can be tricky, but there are a few strategies:

- Set up Auto-Pay: For each card, consider setting auto-pay to pay the statement balance in full each month from your bank. This prevents missed payments and late fees, which is crucial.

- Use Calendar Reminders: If you utilized a special financing plan on a card, mark the payoff deadline on your calendar a month before, so you’re prepared.

- Consolidate Management: Use a personal finance app or even a simple spreadsheet to track balances, due dates, and rewards. There are apps where you can link accounts to see everything in one place.

- Leverage Tools like Kudos: As mentioned before, a tool like Kudos (an AI-powered wallet) can not only suggest the best card to use for a purchase but also keep your cards and their perks in one dashboard. It reminds you of expiring perks or better options, which is super helpful if you have, say, both the Target and Amazon card – you won’t forget which to use on which site.

- Keep Cards Visible: Sometimes the practical tip is to keep the physical cards or a list of them where you do most of your online shopping (securely). Remember, the goal of having these “best” store cards is to save money, so a little management effort is worth the return!

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)