Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

7 Smart Ways Gen Z Can Maximize Credit Card Rewards

July 1, 2025

1. Always Use the Right Card for the Purchase

It sounds obvious, but a lot of us don’t do it: use the card in your wallet that gives the highest rewards for what you’re buying. If you have more than one credit card, each likely has strengths in certain categories. For example, one card might give you 3% back on dining, another only 1%. If you accidentally use the wrong one on your $30 takeout order, you missed out on an extra 2% (that’s $0.60 you could’ve earned). It seems small, but over a year of spending, it adds up significantly.

In fact, an analysis of Kudos’ 300K+ user base showed only 54% of transactions were made with the best card in the person’s wallet – meaning nearly half the time, people weren’t maximizing their rewards on each purchase. How to do better: Keep mental track of your cards’ bonus categories (e.g. Card A = groceries/gas, Card B = restaurants/entertainment). Some people put a little sticky note on each card as a reminder. Even better, use a tool or app to automate this: Kudos (free extension) will pop up at online checkout and literally tell you which card to use for maximum rewards, taking out all the guesswork.

If you’re shopping in-store, you can quickly check a rewards app or even a simple cheat-sheet on your phone. The goal is to match each purchase with the card that earns the most. When you consistently do this, you’d be surprised – you might squeeze out dozens or hundreds of dollars more per year from the same spending.

2. Take Advantage of Sign-up Bonuses (But Don’t Overspend)

Sign-up bonuses are the quickest way to earn a windfall of points or cash back. As a Gen Z cardholder, you might be new to these: many credit cards offer a big bonus (e.g. “Earn $200 after you spend $500 in 3 months” or “Earn 50,000 points after spending $3,000 in 3 months”) as an incentive for new customers. This is essentially free reward value – often worth 20-30% or more of the required spend. Gen Z consumers are actually more likely to have a credit card with a sign-up bonus than older generations, showing that banks are targeting young adults heavily with these offers.

To maximize: only go for bonuses that fit your budget. For example, a $500 spend requirement over 3 months is roughly $167 a month – if you have regular expenses to cover that, great. But a $3,000 requirement might be too high if you’re living on a student budget; don’t overspend or buy stuff you don’t need just for the points (that defeats the purpose).

Time your credit card applications around life events if possible: say you’re about to move apartments or need to buy a new laptop for school – that spend could help hit a bonus naturally. Once you have a new card, make a plan: $3,000 in 90 days is about $1,000 a month – list your known expenses (rent, groceries, books, etc.) and see if they can all go on the card.

If you’re short, maybe prepay a utility or buy a gift card for future use to reach the threshold (only if you were going to spend that money later anyway). Hitting these bonuses can yield huge returns. Example: a 50,000 point bonus could fund a flight worth $500+ or get you $500 cash – that’s a 17% reward rate on the $3,000 spend, way above normal earn rates. Just remember to pay off those purchases (don’t carry a balance; interest will eat into your bonus big time).

3. Pay Your Balance in Full (Avoid Interest to Keep Rewards Profitable)

This might be the unsexiest tip, but it’s absolutely critical: never carry a credit card balance if you can help it. Why is this in a “maximize rewards” article? Because interest charges will wipe out the value of any rewards you earn. Credit card rewards typically return 1-5% of your spending. Meanwhile, credit card interest (APR) on unpaid balances might cost you 20% or more annually.

Do the math: if you don’t pay off a $1,000 purchase, it could accrue ~$200 in interest over a year – even if that purchase earned you 5% back ($50), you’re heavily in the red. A recent survey found 36% of cardholders across all ages check their rewards balances only a few times a year or less, but far more check their credit card bills every month – indicating people feel the pain of payment more than the joy of rewards if not managed properly. The Gen Z approach: treat your credit card like a debit card. Only spend money you have (or will have by the due date), and set up auto-pay in full.

This way, you always avoid interest and truly get free money from rewards. If you absolutely must carry a balance (say an emergency expense you couldn’t cover in full), aim to use a card with a 0% intro APR promotion or pay it off as fast as possible. Think of interest as negative rewards – it’s the opposite of maximizing. By eliminating interest costs, every point and dollar you earn in rewards stays in your pocket.

4. Leverage Bonus Categories and Calendar Promotions

To get more than the base 1% or 1 point per dollar, maximize your use of bonus categories. Many cards for young adults have rotating 5% categories or fixed category bonuses. Other student cards have similar promos. Also watch for limited-time offers: sometimes your card issuer will send an email like “get an extra 5% back at Target this holiday” or you’ll see deals in your app.

Gen Z are heavy online shoppers, so don’t ignore those email offers – a quick click to activate could mean extra rewards on your next purchase. Another trick: some issuers have shopping portals or programs (e.g. Amex Offers, Chase Offers) where you can activate deals (like “10% back at Adidas, up to $10”).

Take a minute each month to scroll through your card’s offers and activate those relevant to you. It’s essentially free extra cash back. Many college students and young professionals also take advantage of seasonal promotions – e.g. a back-to-school bonus category or holiday rewards boost. Keep an eye on your mail or issuer’s social media for these announcements.

Maximizing categories does require a bit of planning, but it can significantly increase your annual reward haul. One strategy: align your big purchases with high-reward times. Need a new phone? If your card offers 5% at Amazon in Q4, perhaps wait until then to buy it there. Just don’t let the tail wag the dog – never buy stuff you don’t need solely because it’s a 5% category. Use categories to amplify necessary spending.

5. Stack Rewards with Apps and Portals (Double Dip when possible)

“Stacking” rewards is a pro move but surprisingly easy these days with technology. Stacking means using multiple reward mechanisms on one purchase. A common stack: use a shopping portal + your credit card rewards. For instance, Rakuten (formerly eBates) or your credit card’s own shopping portal might offer 5% cash back at a retailer online. If you click through that portal and pay with your 2% cash back card, you just earned 7% total on that purchase. Sweet! Many Gen Z shoppers are already familiar with browser extensions like Honey – adding a cash-back portal extension (like Rakuten’s) can alert you to activate that extra cash back.

Similarly, if you use food delivery apps or rideshares, check if your card has a partnership: e.g. some cards give monthly credits on Uber or extra points on DoorDash. Use the affiliate link or add your eligible card to that app to stack benefits. Another stack example: sign-up bonuses + category – say you have a new card with a sign-up bonus for $500 spend, and that card also earns 5x points on groceries this quarter.

When you spend $500 on groceries, you’ve both met the bonus (maybe earning $200) and got 5x points on that $500 (worth perhaps $25 if points are $0.01 each), totaling $225 rewards on $500 spend – a huge 45% return! These opportunities are real, you just have to seize them.

Look out for student discounts or cash-back offers that can layer with your card – for example, UNiDAYS student discounts can be combined with paying by card (the discount reduces price, you still get rewards on the reduced price). Remember, every extra percent counts. Over 40% of Gen Z have used a Buy Now Pay Later or other fintech for deals, but those often don’t give you any rewards; by sticking to credit and stacking smartly, you come out ahead.

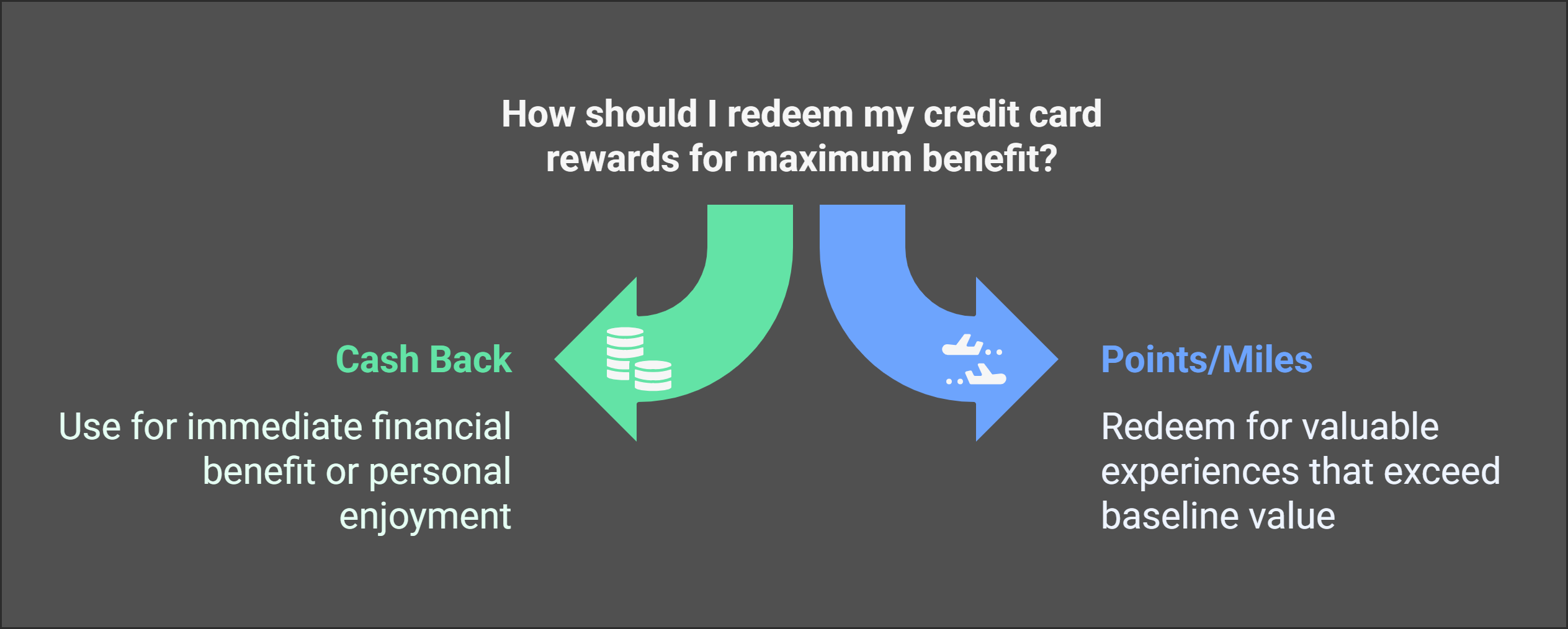

6. Redeem Strategically – Don’t Let Your Rewards Sit Idle

Earning rewards is only half the game – using them effectively is the other. You might be tempted to hoard points for a “big redemption.” That’s fine to a point, but hoard too long and you risk devaluation or expiration. True story: roughly 40% of rewards cardholders feel unsure whether to redeem now or later, and this confusion is highest among Gen Z.

Here’s a simple rule: redeem rewards when you have a meaningful use that gives good value. For cash back, that’s easy – redeem as statement credit or bank deposit whenever you want (personally, I cash out each time I hit $25 or so). For points and miles, “good value” typically means getting more than 1 cent per point.

For instance, if you have travel points, redeem for a flight or hotel that gives you ~2 cents per point instead of a low-value gift card. Don’t sit on points aimlessly for years – their value can erode (airlines and banks can change programs). Case in point: during the pandemic, many travel rewards piled up unused; some were later hit with devaluations. Use your airline miles for that trip home during school break or spring break vacation while you can.

Gen Z tip: Some cards allow you to pay with points on Amazon or PayPal – convenient, but often a poor value (usually 0.8 cents per point). You’re usually better off transferring those points to a travel partner or getting a statement credit. If you’re not sure how best to use a reward, do a quick search (there are blogs and Reddit threads full of “best uses for X points”). And if you decide to save up for something big (like you want to cover a $500 flight next year), have a plan and a timeline. Track your points so they don’t expire. Also, avoid redeeming for stuff just because it’s available – like merchandise through your issuer’s portal often is a bad deal (they markup the points price).

Bottom line: Be purposeful with redemptions. Cash back is straightforward – take it and put it to good use (maybe invest it or at least buy yourself something nice). Points/miles – use them for experiences that you’ll enjoy and that give you more value than the baseline. That’s how you truly maximize the end benefit of your credit card rewards.

7. Exploit Your Card’s Perks (Purchase Protection, Credits, and More)

Maximizing rewards isn’t just about points and cash – it’s also about maximizing the fringe benefits that save you money. Many Gen Z cardholders aren’t aware of all the perks their card offers – and unused perks are lost value. For example, does your card provide cell phone protection if you pay your phone bill with it? If yes, use that card for your phone bill! Then if your phone is damaged or stolen, you could get reimbursed (saving you $500+ easily – way more than typical cash back).

Some cards (especially those with annual fees, but even a few no-fee ones) offer monthly credits for things like streaming services, ride shares, or food delivery. If your card gives $10 monthly Uber credit, make sure you’re using it (set a calendar reminder if needed). These credits are essentially extra cash back, but only if redeemed. Another example: purchase protection and extended warranty – say you buy a new laptop and it breaks after 6 months. If you used a card with purchase protection, you might get a repair or refund from the card issuer. That’s recovering hundreds of dollars – which can dwarf the 1-2% in points you earned on the purchase. Don’t sleep on these benefits.

To maximize them: read through your card’s benefit guide (yes, that booklet or PDF that we all skip). Highlight ones relevant to you. If you have an electronics-heavy life, know about purchase protection. If you travel occasionally, know that your card might have travel insurance, trip delay reimbursement, free checked bags, or airport lounge access. Using those perks = money saved (which is value, just like rewards). For instance, using a free checked bag perk on a flight saves ~$30; do that 3 times a year = $90 saved, effectively like earning $90 in rewards.

Some premium cards even offer subscription trials (like free DashPass for DoorDash or Disney+ months) – activate them if you have the card. Gen Z tends to be very digitally connected, so even perks like ShopRunner membership (free 2-day shipping at various online stores), which some cards give free, can be valuable for your online shopping sprees. The key is to treat your credit card like a benefits bundle and not just a payment method. One report noted consumers collectively leave billions in rewards and benefits unused. By educating yourself on your card’s perks and actually using them, you’re part of the savvy group getting the maximum possible value.

By implementing these tips, Gen Z can punch above their weight in the credit card game – extracting outsized value even with modest budgets. Remember, every swipe can be an opportunity to earn. If you make it a habit to optimize, over time you’ll essentially get paid to use your credit cards. Now let’s address a few common questions to clear up any remaining doubts about maximizing rewards.

FAQs

How do I maximize credit card rewards as a beginner?

Start simple: use one card for all your purchases and make sure it’s a good all-around rewards card. As a beginner, pick a card with broad cash back (like a flat 1.5% cash back on everything or a combo of 3-2-1% on common categories). Put all your expenses on it (and pay the bill in full). This ensures you’re at least earning something on every dollar. Once you’re comfortable, consider adding a second card that complements the first – for example, if your first card is flat 1.5% back, get a second card that gives 3-5% in a category you spend a lot in (groceries, gas, etc.). Then practice using the right card for the right purchase.

Is it okay to have multiple credit cards for the sake of rewards?

Yes – if you manage them responsibly. Multiple cards can help maximize rewards (one card might be best for groceries, another for travel, etc.). Many Gen Zers eventually carry 2-3 cards to cover all bases. Monitor your spending on each so you don’t accidentally overspend just because you have more credit available. As long as you pay on time and in full, having multiple cards won’t hurt your credit; in fact, it can improve your utilization ratio and boost your score over time. Just avoid opening too many in a short span (that can temporarily drop your score with hard inquiries).

What about using debit or BNPL instead of credit – am I missing out on rewards?

Debit cards typically do not offer significant rewards (there are a few that give 1% or so, but they’re rare). And Buy Now Pay Later (BNPL) services (like Klarna, Afterpay) don’t give rewards at all – they’re just installment payment plans. So yes, you’re potentially missing out on rewards when you use those instead of a credit card.

Do credit card rewards expire? How can I avoid losing them?

It depends on the program. Cash back on most cards doesn’t expire as long as your account is open and in good standing. For example, if you have $100 cash back accrued, it will sit there indefinitely until you redeem it (though read your card’s terms – a few issuers say cash back expires if your account is inactive for a long period, like 12-24 months of no use). Points and miles are trickier: some expire after a certain period of inactivity (e.g. many airline miles expire if you have no earning or redemption activity for 18-24 months).

What’s the best way to use credit card points for travel (for maximum value)?

The best way to use points for travel is usually to redeem them for travel! That sounds circular, but what we mean is: you typically get the highest value per point by using points for flights, hotels, or other travel expenses, rather than gift cards or merchandise.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)