Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

A Freelancer’s Guide to Business Credit Cards – How to Qualify and Maximize Benefits

July 1, 2025

.webp)

If you’re a freelancer, independent contractor, or gig worker, you might wonder if business credit cards are “off-limits” to you. Good news – freelancers can absolutely get business credit cards, and doing so can be a game-changer for your finances.

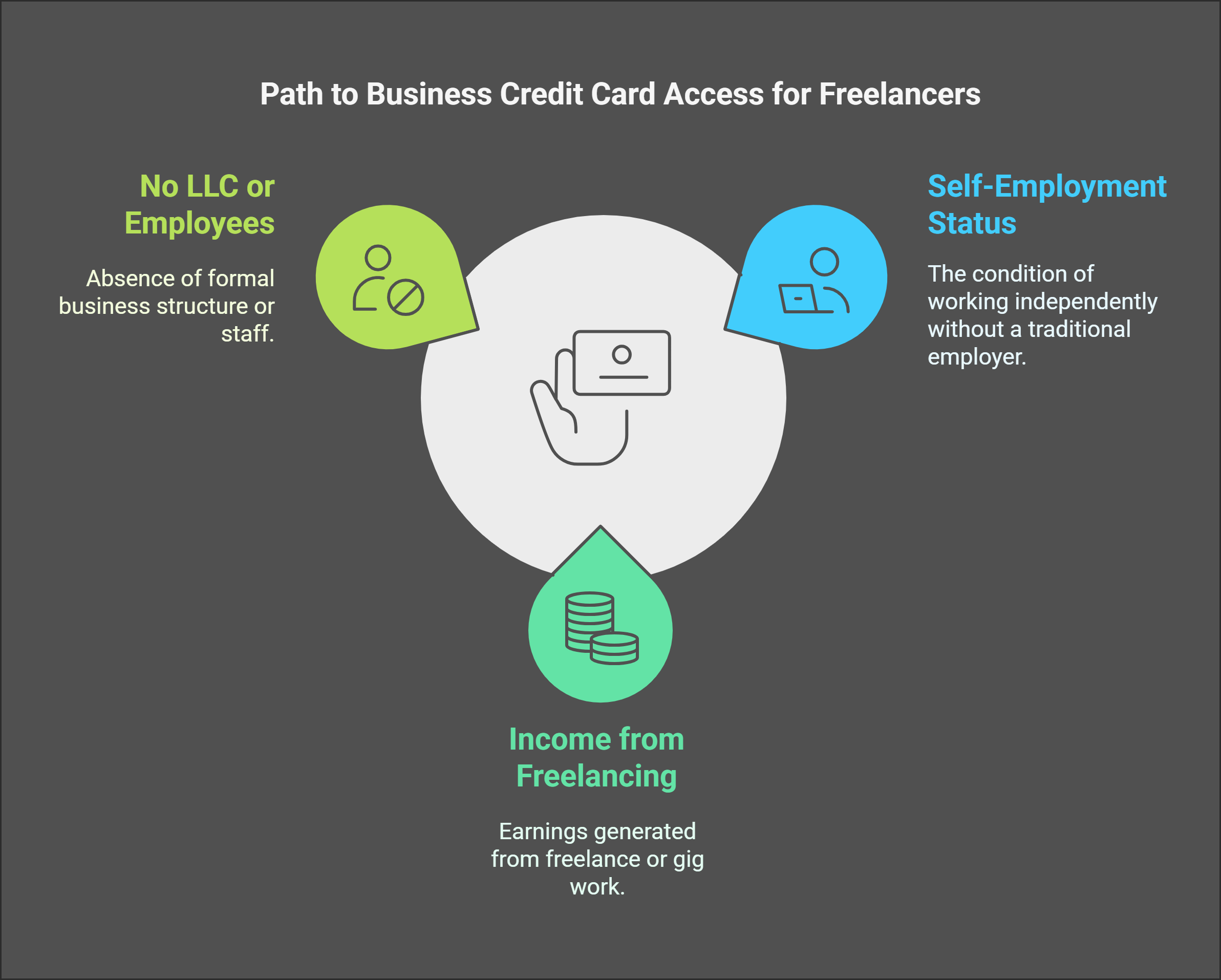

This guide will walk you through how to qualify for a business credit card when you’re self-employed, how to navigate the application process, and tips to squeeze the most benefit from your new card. No LLC, no employees, no problem – if you have income from work you do on your own, you likely meet the definition of a business in the eyes of credit card issuers. Let’s demystify it step by step.

1. Understanding “Business” in Credit Card Terms

First, it helps to know what counts as a “business” for credit card applications. Essentially, any activity you do for profit can be a business. This includes freelancing (writing, graphic design, programming, consulting, etc.), driving for rideshare or delivery apps, selling goods online (Etsy shop, eBay flipper), tutoring, and so on. You do not need an incorporated business or EIN (Employer Identification Number) to apply – your Social Security number and your own name can serve as the business identifier.

In applications, you’ll often see a choice for business structure; as a freelancer, you select sole proprietorship (which just means a one-person business, not registered as an LLC or corporation). Millions of Americans operate as sole props – and banks issue business credit cards to them all the time.

Key point: When a credit card application asks for “Legal Business Name,” use your own name (unless you have a separate business name you’ve registered with a local authority, but that’s optional for most freelancers). For “Tax ID,” use your Social Security Number (SSN).

You’ll also need to provide your personal address (which doubles as business address if you don’t have a separate office) and usually your personal income in addition to any business income. Think of it this way: to the bank, you are the business. They will evaluate your personal creditworthiness primarily, but treat the account as a business account.

2. Qualification Criteria – What Do Banks Look At?

To get approved for a business credit card, here’s what matters:

Personal Credit Score:

This is number one. Typically, you’ll want a good to excellent credit score (roughly 680+) for most business cards, especially those with big rewards. Some cards (like certain Capital One or store cards) might approve lower scores, but generally aim to improve your score before applying. The bank will do a hard credit inquiry on your personal credit when you apply.

Income (Business and Personal):

You’ll be asked to state your annual business revenue (even if it’s $0 for a new venture) and maybe total income. Be honest – it’s okay if you’re just starting and the number isn’t huge. Banks use income to gauge your ability to pay. There isn’t a strict cutoff; a freelancer earning $20k a year can get a card, as can one earning $200k. If your business income is low but you have other income (a part-time job, spouse’s income you have access to, etc.), you can often include that in “total income.” Regulations allow you to state any income to which you have reasonable access.

Time in Business:

Applications often ask “years in business.” Don’t be intimidated – even if the answer is “0” or “less than 1,” that’s fine. Many people apply as soon as they start their side gig. If the form allows, “1” year is a common minimum choice; it doesn’t need to be exact. Lenders understand a lot of applicants are newly minted businesses. They might weigh your personal credit more heavily if your business is new.

Business Type and Industry:

You’ll need to select an industry category for your business. Just choose what fits best (for example, a freelance writer could pick “Writing/Editing Services” or “Consulting,” a rideshare driver might pick “Transportation” or “Independent Driver”). There is no “correct” answer that will make or break the application; it’s mostly for the bank’s records. All industries from creatives to contractors are generally acceptable. (A few restricted categories like gambling or illegal activities aren’t allowed, but obviously freelancers aren’t applying for those!)

Existing Relationship:

Having a checking account or prior card with the bank can slightly help but is not required. If you already have, say, a Chase personal credit card and handle it well, getting a Chase business card may be a tad easier. But plenty of people are approved as new customers too.

Myth busting: You might have heard you need an EIN or to show invoices, etc. Usually, you do not need to provide any proof of business when applying. In some cases, if your application gets flagged for verification, the bank might ask for documentation (like a proof of business existence or income).

This is relatively rare for freelancers with straightforward applications. To be prepared, you could have a simple document like an invoice from a client or a bank statement showing deposits from your freelance work, but most likely you won’t be asked for it.

3. Step-by-Step: Applying for a Business Credit Card as a Freelancer

Step 1:

Choose your card. Ideally, pick one that suits your needs (see our “5 Best Cards” article for ideas). If it’s your first, maybe a no-annual-fee card with cashback is wise. Ensure your credit score is in range – you can check your score for free via many services.

Step 2:

Fill out the application with your business info. This includes:

- Business Name: Your name (unless you have a DBA name you use, but that’s optional).

- Business Address: Your home address (if that’s your office).

- Type of Business: Sole Proprietor.

- Tax ID: Your SSN.

- Years in Business: Can be 0, 1, etc. If you’ve freelanced informally for a while, it’s okay to count that time even if you only just decided to get a card now.

- Number of Employees: 1 (that’s you) unless you actually have others.

- Annual Business Revenue: Sum up what you made in the last 12 months from your freelance/gig work. If you’re brand new, you could put 0 or a reasonable expected first-year figure (some put their projected income for the year, which is acceptable as “expected revenue” – just don’t wildly inflate it).

- Estimated Monthly Spend: Sometimes asked – can estimate what you think you’ll put on the card monthly.

Step 3:

Fill in personal info. This is similar to any credit card app: your personal annual income (include all sources), rent or own home, etc., and your personal contact info. This is because you as an individual are guaranteeing the debt.

Step 4:

Submit and wait briefly. Many applications give an instant decision (approval or denial) within a minute. Sometimes it goes to pending review. Don’t panic if it’s pending – that can happen for various reasons not necessarily negative (maybe they want to double-check something). You might get a call or an email in a few days. You can also call the bank’s application status line to inquire.

Step 5:

If approved, congratulations! The card will be mailed to you, typically within 7-10 business days. If denied, you have the right to an adverse action letter explaining why. Common reasons for denial might be “limited credit history” or “too many recent inquiries” or “credit score not high enough.” If that happens, you can call the issuer’s reconsideration line to plead your case (e.g., explain your income, ask if they’ll reconsider – sometimes providing more info can overturn a decision). There’s no harm in trying.

Step 6:

Activate and use wisely. Once you have the card, treat it like the business tool it is. Use it for your freelance expenses, and remember to pay on time. Typically, business cards won’t show up on your personal credit report unless you default, so they won’t impact your personal credit utilization – one reason they’re great. But note: one exception is Capital One and Discover business cards, which do report to personal bureaus. If you got one of those, manage your utilization to keep your personal score safe.

4. Building Business Credit as a Freelancer

Now that you have a business credit card, you’re actually starting to build a business credit profile in addition to your personal credit. Small sole proprietorships can have a business credit score (like a Dun & Bradstreet PAYDEX, etc.).

Using your business card responsibly can eventually help you get other forms of financing (like a small business loan, or simply higher credit limits). Here’s how to leverage that:

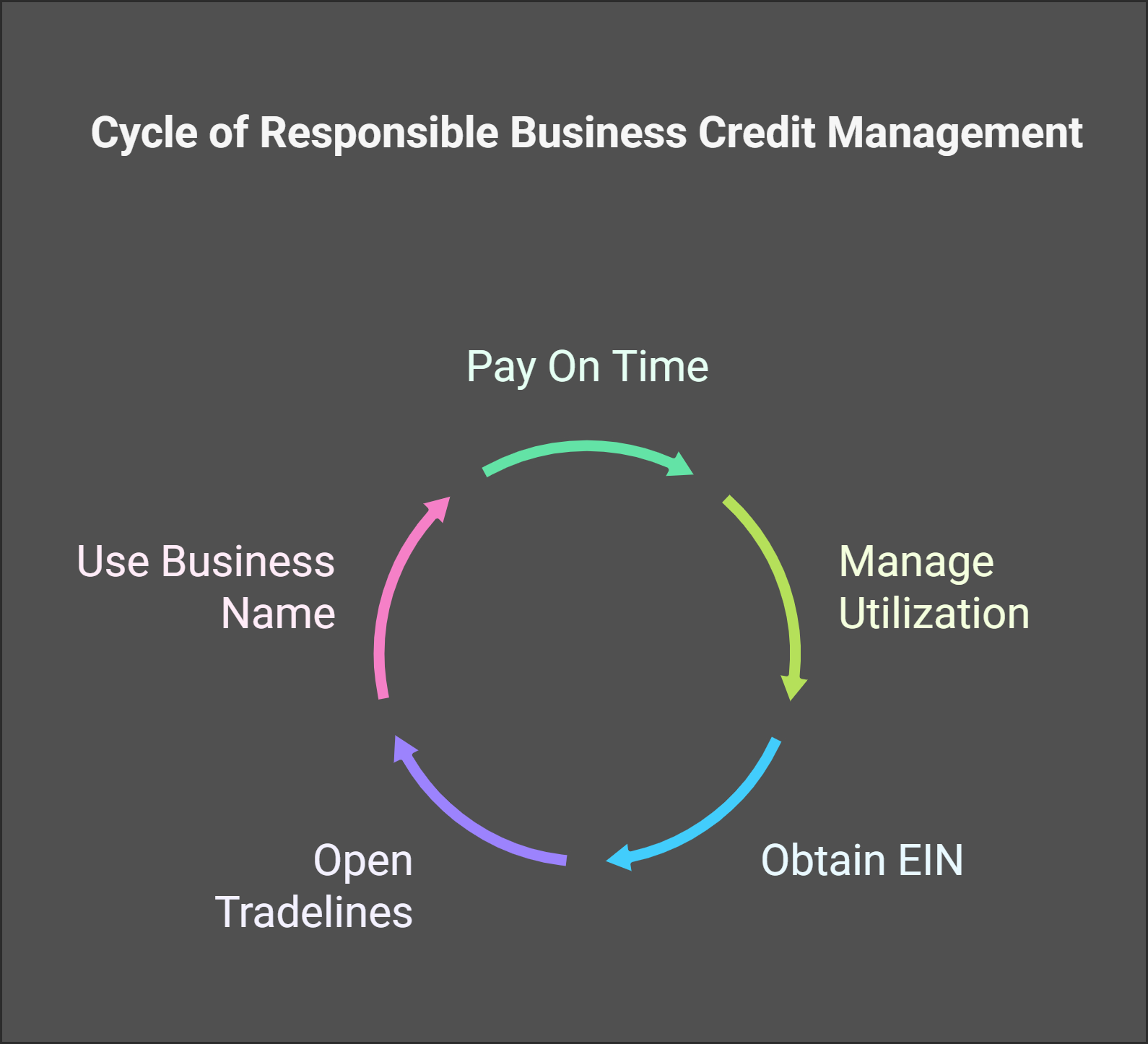

- Always pay on time (early if possible). This is the biggest factor for any credit score, personal or business.

- Keep utilization reasonable. Even though most business cards don’t affect your personal credit score, the issuer still monitors how you use the credit line. If you max it out often, they might be hesitant to increase your limit or approve you for another card. A good rule: try to keep balances under 30% of your limit, and pay them off monthly.

- Consider getting an EIN eventually. While not required, if your freelance biz grows, you can apply for a free EIN from the IRS. You can then call your card issuer and update the Tax ID on file to your EIN (and your SSN remains as personal guarantee). Having an EIN can also let you register with business credit bureaus formally. It’s not necessary at the start, but something to know for the future.

- Open tradelines with vendors (if relevant). This is more if you have expenses like supplies from specific companies – some freelancers who, say, buy a lot of craft supplies might open a small account with a vendor that reports payments to business bureaus, further building credit. But this is an advanced tactic and usually not needed unless you plan to seek larger financing.

- Use your business name on invoices and payments. Even as a sole prop, you can start using a business name or your personal name “DBA [Your Business Name]” on invoices, and open a separate bank account for your business transactions. Paying your business credit card from a dedicated business bank account (even if it’s just another checking account you label for business) creates a clear financial separation that lenders like to see.

Remember, as a freelancer, you and the business are legally the same. So your business credit and personal credit are intertwined. If your business card defaults, you are personally liable. But also, your good behavior benefits you personally – e.g., Chase might be more likely to approve you for a personal Sapphire card down the line if you’ve been a great customer on the Ink business card, and vice versa. Building business credit is a marathon, not a sprint, but you’ve taken a key first step by getting a card.

5. Maximizing Business Card Benefits for Freelancers

Now that you’ve got the card, use it to the fullest! We touched on strategies in previous articles, but here’s a quick checklist specific to new cardholders:

Hit that welcome bonus:

If your card has a sign-up bonus (spend $X in 3 months to get reward), plan for it. Funnel every possible business (and even personal, if allowed) expense through the card to meet the goal. Just avoid buying things you don’t need – instead, time things like equipment upgrades or paying annual subscriptions upfront.

Set up autopay:

Missing a payment can kill your score. Set at least the minimum to auto-pay. Ideally, set full statement balance to auto-pay (assuming you have an emergency fund to cover a slow business month – if not, autopay the minimum and pay extra manually).

Use the perks:

Does your card have cell phone insurance? Then pay your cell bill with it. Does it have airport lounge access (like Amex Business Platinum does)? Use it on your next trip. You’re self-employed, you deserve the benefits that normally corporate folks get! If you’re not sure what perks your card offers, read the guide or the benefits on the issuer’s website. You might be surprised – for example, some Chase Ink cards give a free year of DoorDash DashPass (handy for meal deliveries when you’re working late).

Expense tracking:

As you start putting everything on one card, leverage the transaction categorization. Many card issuers categorize transactions (gas, travel, supplies, etc.). This will help at tax time. You can also export to CSV or connect the card to accounting software. This is a huge lifestyle improvement – no more sorting piles of receipts (though keep digital/paper receipts as needed for tax backup).

Tax deductions:

Interest on business purchases and annual fees on business cards can be tax-deductible as business expenses (talk to a tax professional, but generally if a cost is solely for business, it’s deductible). That means if you ever do carry a balance for a business purchase, the interest paid could be written off (still best to avoid interest, but worth noting). Same with annual fees: if you have a $95 fee for a business card, you can likely deduct it on Schedule C as a banking expense.

Leverage support:

Many business cards come with a dedicated customer support line for business customers. If you ever have an issue (fraud, need a credit line increase, late fee waiver request), don’t hesitate to call – issuers often value small business customers and will try to help to keep your loyalty.

Final Tips

Getting a business credit card as a freelancer is not only doable, it’s often one of the first “official” steps in treating your hustle like a business. It can be empowering to see a credit card with your name and “business” on it – a small but meaningful validation that yes, you’re a business owner! Use that as motivation to keep growing and refining your venture. Keep communications from your issuer — sometimes they send targeted offers (e.g., spend $X more this quarter for bonus points, or refer a friend bonuses) that you can take advantage of.

And don’t forget the earlier strategies we discussed: the card is a tool. When used right (paying in full, leveraging rewards, separating expenses), it can simplify your life and even boost your earnings (through cash back, points, and savings on fees). As your business evolves, periodically review if the card you got is still the best one for you, or if you could add another to optimize rewards. Many freelancers start with one card and a year later get another to maximize a different category – that’s fine as long as you can manage them well.

Being a freelancer means you have to create your own benefits and financial stability – a good business credit card is one piece of that puzzle, providing convenience, security, and value. Now that you know how to get one and use it wisely, you’re adding a powerful ally to your freelance toolkit.

Managing a business credit card (or a few) alongside your personal finances might sound like a lot, but it doesn’t have to be. Kudos is a free tool designed to help people like you manage multiple cards with ease. It can automatically apply the best card at checkout online, remind you of which card to use for what category, and keep track of your rewards.

Think of it as a smart wallet that knows your freelancer life. As you step into the world of business credit cards, let Kudos simplify the day-to-day usage so you can focus on growing your business. From suggesting the card that gives you 5% back on that online software purchase, to ensuring you never miss out on points, Kudos has your back. It’s like having a virtual CFO for your one-person business – making sure every swipe is optimized. Put your new business credit card to work, and let Kudos help you reap all the benefits, hassle-free.

FAQs and Troubleshooting

Let’s address a few common concerns new freelance cardholders have (many we’ve hinted at earlier):

What if I get denied?

It’s not the end of the world. First, consider calling the issuer’s reconsideration line. Be ready to explain your business (e.g., “I’m a freelance graphic designer looking to separate my business expenses from personal ones. I have steady clients and expect to earn about $XX this year.”). Sometimes providing additional info or clarifying a mistake on the application can turn a “no” into a “yes.”

If it still doesn’t work out, don’t immediately apply for another card – multiple inquiries can hurt your credit in the short term. Instead, work on the likely reasons for denial (common ones: limited credit history – in that case, use a personal card or secured card to build up; high credit utilization – pay down balances; recent late payments – get back on track and wait 6-12 months). You can also seek out a card that is known for easier approval, like a bank where you have a checking account, or a card specifically for “fair” credit.

Will using a business credit card help my personal credit score?

Indirectly, yes. Most business cards (e.g., Amex, Chase, Citi business cards) do not report your monthly spending or balances to personal credit bureaus, so they won’t build your personal credit through on-time payments in the way a personal card would. However, they also won’t hurt your personal score by adding to your credit utilization. They usually only show up on your personal credit if you default. That said, some issuers like Capital One do report business card activity to personal credit files. If you have one of those, then on-time payments will help your personal score (and conversely, missed payments will hurt it).

Even if the card doesn’t report, having it can improve your finances (by organizing debt, freeing up personal credit lines), which can help you keep your personal credit in good shape. Also, note that the inquiry for the application will appear on your personal report and may shave a few points off your score temporarily (as any credit inquiry does). So don’t panic when you see that – it’s normal and usually rebounds in a few months.

Are there any downsides to using a business card versus a personal card?

A minor one is business cards are not covered by certain consumer protection laws (like the CARD Act in the U.S.). This means, for instance, business cards aren’t required to give you 21 days from statement to due date (though most issuers still do), or they can change your APR without as much notice. In practice, major issuers treat their business customers well, and you likely won’t notice a difference. Another consideration: reward redemption options can differ (e.g., you can’t use Chase Ultimate Rewards from an Ink card for cash back at a superior rate unless you have a Sapphire Preferred/Reserve; but you can still get 1 cent per point).

Also, missing a payment on a business card can still indirectly hurt you (fees, possible reporting to personal after 60-90 days delinquent). So the “downside” is just that you should exercise the same caution as with any credit product. Finally, some business cards don’t have 0% APR offers that personal cards do. But some do (Spark Cash Select, as mentioned, or U.S. Bank Triple Cash). So if you need a promotional APR, pick accordingly.

Can I use one business credit card for multiple freelance gigs?

Absolutely. If you do various types of freelance work, you don’t need separate cards (unless you want to for your own tracking). For example, you might be a freelance web developer and drive Uber on weekends. You can use the same card for both sets of expenses. All of it collectively is your “business” (even if diversified). If you eventually form separate businesses (like you LLC your consulting separate from your Etsy store, etc.), you might then get a card for each entity.

But most people starting out have a general sole prop that covers all side hustles. Just be sure to use the card only for business-related expenses from those gigs – don’t mix personal stuff, to keep accounting clean and to uphold the integrity of the separation in case of an audit or credit review.

What if I stop freelancing – do I have to close the card?

Not necessarily. If you cease your business, you can keep the card open for a while especially if it has no annual fee, since closing it could slightly ding your credit (closing accounts can reduce your available credit). However, strictly speaking, the card is meant for business use. If you truly no longer have any business, some cardholder agreements say you should close it. In practice, if a hobbyist shuts down for a year then resumes, they often just keep the card.

Alternatively, you could call the issuer and ask to convert it to a personal card (few issuers allow this, but it’s worth asking – sometimes a bank might let you switch a business card to a personal version). If you keep it, avoid putting personal expenses on it – that breaches terms. One approach: if you stop freelancing, perhaps use the card for any remaining quasi-business expenses (like winding down costs) and then sockdrawer it (don’t use it). The account will remain in good standing and continue to build credit age. If it has an annual fee and you’re not using it for business anymore, then yes, probably close it or downgrade it to a no-fee business card if possible.

Will I have to pay my business credit card bill from a business bank account?

No, you can pay from any bank account (personal or business). There’s no requirement that the payment come from a business account. However, for cleanliness, you may want to pay from a dedicated account – it could be a separate checking account you set up for your freelance finances. Many freelancers simply use their personal checking to pay the card each month, which is okay. If you do that, just ensure you note those transactions for bookkeeping (so you don’t confuse a business expense payment as personal). As you grow, opening a business checking account is a good idea to further separate church and state. But it’s not mandatory to have one to use a business CC.

Are there any fees unique to business credit cards I should watch for?

Generally, fees are similar to personal cards: potential annual fee, late payment fee, cash advance fee (don’t take cash advances unless emergency; same rule as personal). One thing to watch is foreign transaction fees – if you deal internationally, pick a card with no foreign fees. Many business cards do waive foreign fees (like all Capital One, Chase Ink Preferred, etc.), but some don’t (Chase Ink Cash has 3% foreign fee).

Another “fee” scenario is if you add employee cards – the cards in our list all offer free additional user cards, but a few premium business cards charge for extra users (usually ones with hefty perks). As a sole prop, you likely won’t have extra users (unless you give one to a spouse or assistant to make purchases on your behalf). In short, check the terms just as you would a personal card. Business cards follow similar patterns, just with the legal distinction of being a business liability.

What’s the biggest advantage of having a business card as a freelancer?

In a word: professionalism (and all the financial perks that come with that). It forces you to treat your freelance work as a separate entity, which can clarify your finances. The rewards are tailored to common business needs (making it potentially more rewarding than using a random personal card). Also, as you earn points or cash back on business expenses, it feels like reinvesting in your business. There’s also something to be said about establishing a relationship with a bank on the business side – down the road, if you ever need a line of credit or a loan, having a history with a business credit card account can help.

Emotional perk: some freelancers mention it helped them mentally separate work spending, which improved their budgeting. It’s easier to analyze “was my freelance gig profitable this month?” when all the expenses for it are on one statement. And come tax time, you’re basically handed a neat summary of deductions, rather than combing through everything.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)