Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Are Retail Store Credit Cards Worth It? Pros, Cons & What to Consider

July 1, 2025

.webp)

The Appeal of Store Credit Cards (Pros)

Store credit cards can indeed offer some attractive perks for loyal shoppers. According to Experian, these cards often provide exclusive discounts, special financing deals, free shipping, or other rewards at the retailer – and they can even be a way to start building credit if you have a limited credit history.

Key advantages include:

Instant Discounts & Perks:

Most store cards give you a significant one-time discount on your first purchase when you sign up (often 10–20% off) and ongoing perks like exclusive coupons, birthday rewards, or free shipping for cardholders. These benefits can save frequent shoppers money as long as you avoid impulse spending on extra items you wouldn’t buy otherwise.

Special Financing Offers:

Big-box retailers (especially for appliances, electronics or furniture) may offer “no interest for 6 months” or similar financing on large purchases if you use their store card. This deferred interest promotion can help stretch out payments interest-free – but only if you pay off the full balance within the promo period (more on the catches below).

Loyalty Rewards:

Some store cards function as enhanced loyalty programs, earning you points or cash back only usable at that store. For example, a clothing retailer’s card might give 5% back in store credit for every purchase, on top of regular sales. If you’re already spending a lot at that store, the rewards can effectively boost your savings.

Easier Approval (Build Credit):

Retail cards are generally easier to qualify for than general-purpose credit cards. Many store cards accept applicants with fair or even limited credit. The credit limits are lower, but that lower barrier to entry means you can use a store card to help build your credit history with on-time payments. In fact, approval rates for people with credit scores in the 620–720 range are about 20% higher for retail cards than for regular cards. For someone new to credit or rebuilding, a store card can be a stepping stone.

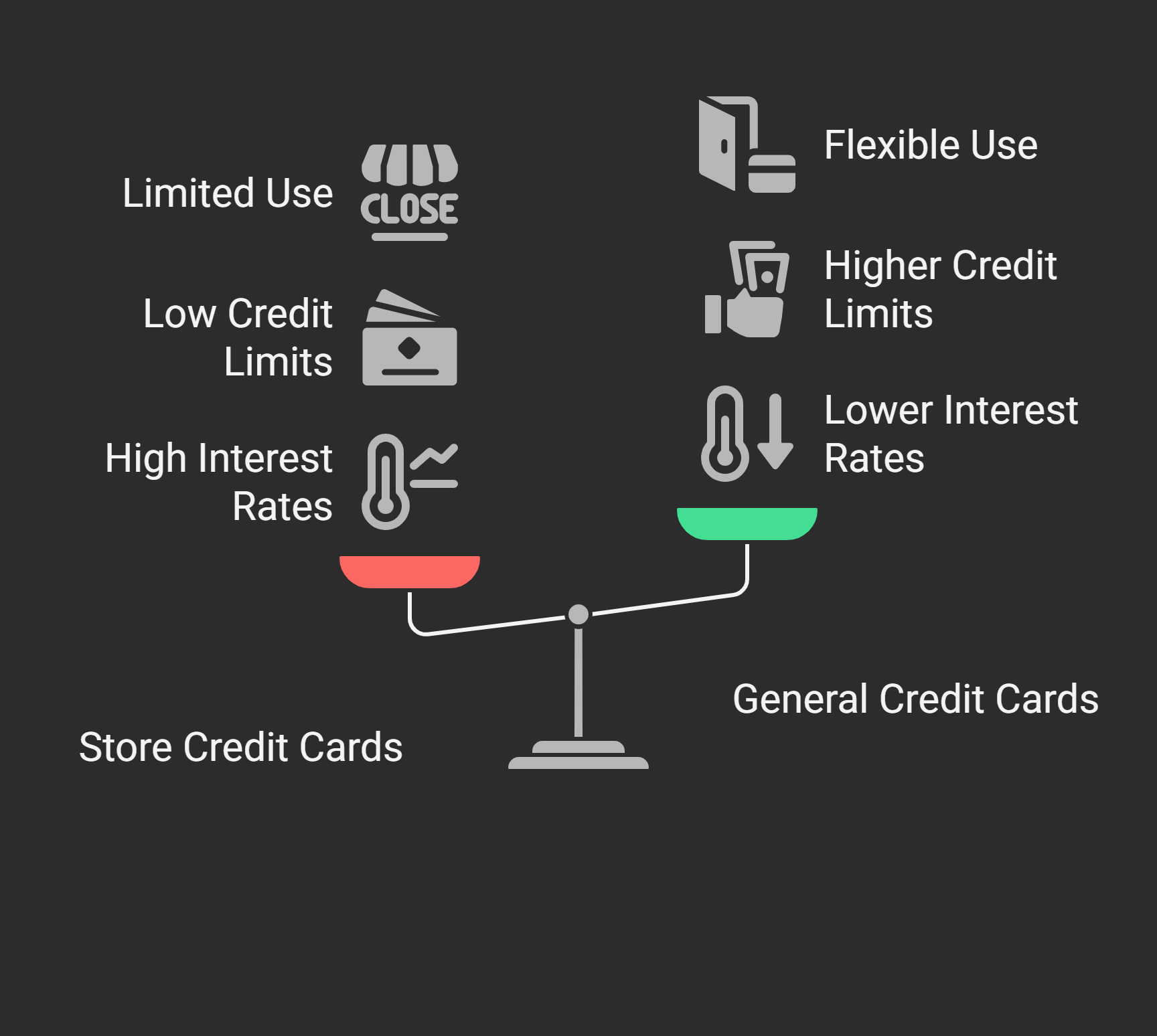

The Downsides of Store Credit Cards (Cons)

Despite the perks, store credit cards often carry serious drawbacks that make them a “better deal for the store than for the customer”. Here are the major cons to be aware of:

High Interest Rates:

Retail store cards tend to charge much higher annual percentage rates (APR) than general credit cards. While the average APR on a general credit card is around 16–22%, store-only credit cards often have APRs well into the mid-20s or even around 30%. This means if you don’t pay the balance in full, interest charges rack up quickly – wiping out any savings from that 15% sign-up discount. Translation: The store earns the rewards, not you, if you carry a balance.

Low Credit Limits:

Store cards typically come with lower credit lines than general cards. A big shopping trip or a couple of purchases can easily max out a store card’s limit, which hurts your credit utilization ratio (a factor in your credit score). For instance, a $500 limit card would be 80% utilized by a $400 purchase – potentially dinging your credit score if reported that way.

Limited Use (Closed-Loop):

Many store credit cards are “closed-loop,” usable only at that specific retailer or its affiliates. You can’t swipe them at other stores to take advantage of rewards elsewhere. Some major retailers do offer co-branded versions (Visa, Mastercard) that work anywhere, but the richest rewards still apply only to that store. Either way, a store card generally lacks the flexibility of a general cash-back or travel card that earns rewards on all your spending.

Deferred Interest Traps:

Those “0% interest” special financing deals are often deferred interest offers. This means if you fail to pay off the full balance by the end of the promo period, you’ll get hit with all the interest backdated to the purchase date. For example, a $1,000 TV on a “6 months no interest” store plan could suddenly accrue hundreds in interest at a 25% rate if you still owe even $1 when the 6 months are up. General-purpose 0% APR cards don’t do this – they usually only charge interest on the remaining balance going forward. So the store card’s financing can prove far costlier if you’re not careful.

Impact on Credit & Future Cards:

Applying for any new credit card will put a hard inquiry on your credit report and slightly ding your score. That’s not a big deal on its own, but opening a low-value store card could use up a slot that might prevent you from getting a better card soon after. For example, avid credit card users note Chase bank’s “5/24 rule” – if you’ve opened 5+ cards in 24 months, you can’t get certain top-tier cards. Store cards count toward that limit. It’s worth considering whether it’s worth sacrificing future opportunities (like a great travel rewards card) for a modest one-time store discount. Additionally, having too many open store accounts can be a management headache and potential fraud risk if you’re not actively using them.

So, Are Store Credit Cards Worth It?

For most shoppers, a general-purpose rewards credit card will offer more long-term value than a single-store card. With a regular cash-back or travel card, you can earn rewards anywhere you shop, usually get a higher credit limit, and benefit from a lower APR and broader perks (like purchase protection or travel insurance) that store cards don’t provide. Flexibility is key: you’re not locked into spending only at one retailer to reap benefits.

That said, store credit cards can be worthwhile in specific situations:

- If you are a die-hard loyalist of a particular store and shop there frequently and you’re confident you’ll always pay the card in full. In this case, the 5% back, exclusive coupons, or special sales access might outweigh the limitations. For example, the Target RedCard (store version) gives 5% off every Target purchase plus free shipping – a strong ongoing perk for regular Target shoppers. Just don’t use it for more than you’d normally buy.

- If you’re building or rebuilding credit and can’t qualify for a traditional card yet. A store card could be an easier approval that helps establish credit. Use it for a small purchase periodically and pay it off to generate positive payment history. Once your score improves, you can upgrade to better cards.

- If there’s a big one-time discount that truly makes a difference and you have the discipline to manage it. For instance, saving $100 on a major appliance with a new store card offer could be worth it – if you then pay it off and maybe even consider closing the card to avoid long-term issues. Be cautious: closing a brand-new card can slightly hurt your score in the short term, but keeping it open and unused can also pose risks (like forgetting a bill or annual fee, if any). Weigh the pros and cons based on your situation.

In the end, it depends on how you use them. If you carry a balance or overspend due to the card, a store credit card will definitely cost you more than it saves you. However, if you’re a savvy shopper who uses the card’s perks strategically and avoids its pitfalls, it might provide value in its niche. Just remember that there are often alternative ways to get similar benefits without the downsides – which we’ll touch on next.

Alternatives to Store Cards: Maximizing Rewards with Fewer Hassles

Before jumping on a store credit card, consider some alternatives that can still reward your spending:

General Cash-Back Cards:

A flat-rate cash back card (like a 2% back on everything card) or a rotating category card (like 5% on different categories each quarter) can yield great savings across all stores, not just one. For example, one popular card offers 5% back at Amazon and Target in Q4 each year, effectively matching many store cards’ rewards during the holiday season. The rest of the year, you still earn rewards everywhere else. Bottom line: you don’t need a separate card for each store if one or two good general cards cover all your spending with rewards.

Use Technology to Your Advantage:

Tools like Kudos (a free smart wallet browser extension) can automatically help you maximize rewards without needing store-specific cards. Kudos can suggest the best credit card to use at checkout for any given online store to get the highest cashback or points, and even alert you to hidden perks on your cards. This means you could get, say, 5% back by using your existing card with the best rewards for that store – no new card required. It also keeps track of all your cards’ benefits in one place, so you never miss out on a deal you already have. By leveraging such tools, you can replicate a lot of the savings store cards advertise, while using the cards you already carry.

Manufacturer or Retailer Apps/Coupons:

Sometimes you can sign up for a retailer’s loyalty program or mailing list to get similar discounts (like 10% off coupons or members-only sale days) without opening a new credit line. Many stores offer a debit card option (like the Target Debit RedCard) or simply send promo codes via email. Always check if there’s a non-credit alternative for the discount.

0% APR Promotions on General Cards:

If the appeal is financing a big purchase, note that many general credit cards offer 0% introductory APR periods for 12–18 months on purchases. These true 0% APR offers don’t charge retroactive interest. They can be a safer way to finance something over time compared to a deferred-interest store card offer. Just be sure your credit is good enough to qualify and always aim to pay off before the intro period ends.

FAQ: Retail Store Credit Cards

What is a retail store credit card?

It’s a credit card offered by a specific retailer, often usable only at that retailer (closed-loop) or as a co-branded Visa/Mastercard usable anywhere. Store cards typically provide special benefits when used at the store – like discounts or rewards – but with higher APRs and restrictions on where you can use them.

Do store credit cards help build credit?

Yes – store cards report to credit bureaus just like other credit cards. If you make on-time payments, it will help build positive credit history. They’re often easier to get approved for, so they can be a starter card for those with no or low credit. Just keep balances low (ideally pay in full) to avoid the high interest and to keep your credit utilization in check.

Why do store credit cards have such high interest rates?

Retailers and their bank partners often charge higher interest (often 25–30% APR) because they’re taking on more risk by approving more applicants with average credit. Also, the attractive upfront perks come at a cost. The banks recoup that cost through higher finance charges on those who carry a balance. In short, the convenience and easy approval of store cards is offset by the pricey interest if you don’t pay off purchases immediately.

What’s the “catch” with 0% financing offers on store cards?

Many store cards advertise “No interest if paid in full in X months.” The catch is this is typically a deferred interest deal. If you pay every penny before the promo period ends, you’re fine. But if even $1 remains, you get charged all the interest from day one. For example, a 0% for 12 months offer at 25% APR – if you fail to pay it off, month 13 will bring a 25% interest charge on the entire starting balance. Always read the fine print. A true 0% APR offer (common on some general cards) doesn’t do that.

Should I get a store credit card just for a one-time discount?

Be cautious. While saving e.g. $50 on a big purchase feels great now, consider the long term. If you don’t plan to use the card regularly, you might end up with a ding to your credit (from the inquiry and new account), and possibly temptation to spend more. If you do take a one-time deal, try to pay it off and maybe even close the card to avoid future fees or misuse. Often, a competitive general cash-back card with a sign-up bonus can be an even better deal than a modest one-time store discount. For instance, some cash-back cards give $200 bonus after you spend a certain amount – far richer than most store card intro offers. Only get a store card if the ongoing benefits make sense for you, not just the upfront coupon.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)