Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Cash Stuffing 101 – The TikTok Budget Hack Gen Z Loves (Envelope Method Explained)

July 1, 2025

Tired of swiping your card and losing track of spending? Cash stuffing might be the budgeting trick for you. This old-school method (also known as the Envelope System) has made a huge comeback thanks to TikTok – where videos of people stuffing cash into pretty budget binders have racked up hundreds of millions of views. Gen Z has rediscovered what maybe your grandma did with jam jars: using cash and envelopes to manage money.

In this article, we’ll break down exactly how cash stuffing works, why so many people are obsessed with it, and whether it actually helps you save. You’ll get a step-by-step guide to start cash stuffing on your own, plus some modern tips to make this method work in today’s digital world.

(Spoiler: you don’t have to ditch your credit cards entirely – you can have the best of both worlds!). Let’s dive into this tactile, ASMR-worthy budgeting trend and see if stuffing envelopes with cash can stuff your savings account, too.

What is Cash Stuffing? A Quick Overview of the Envelope Method

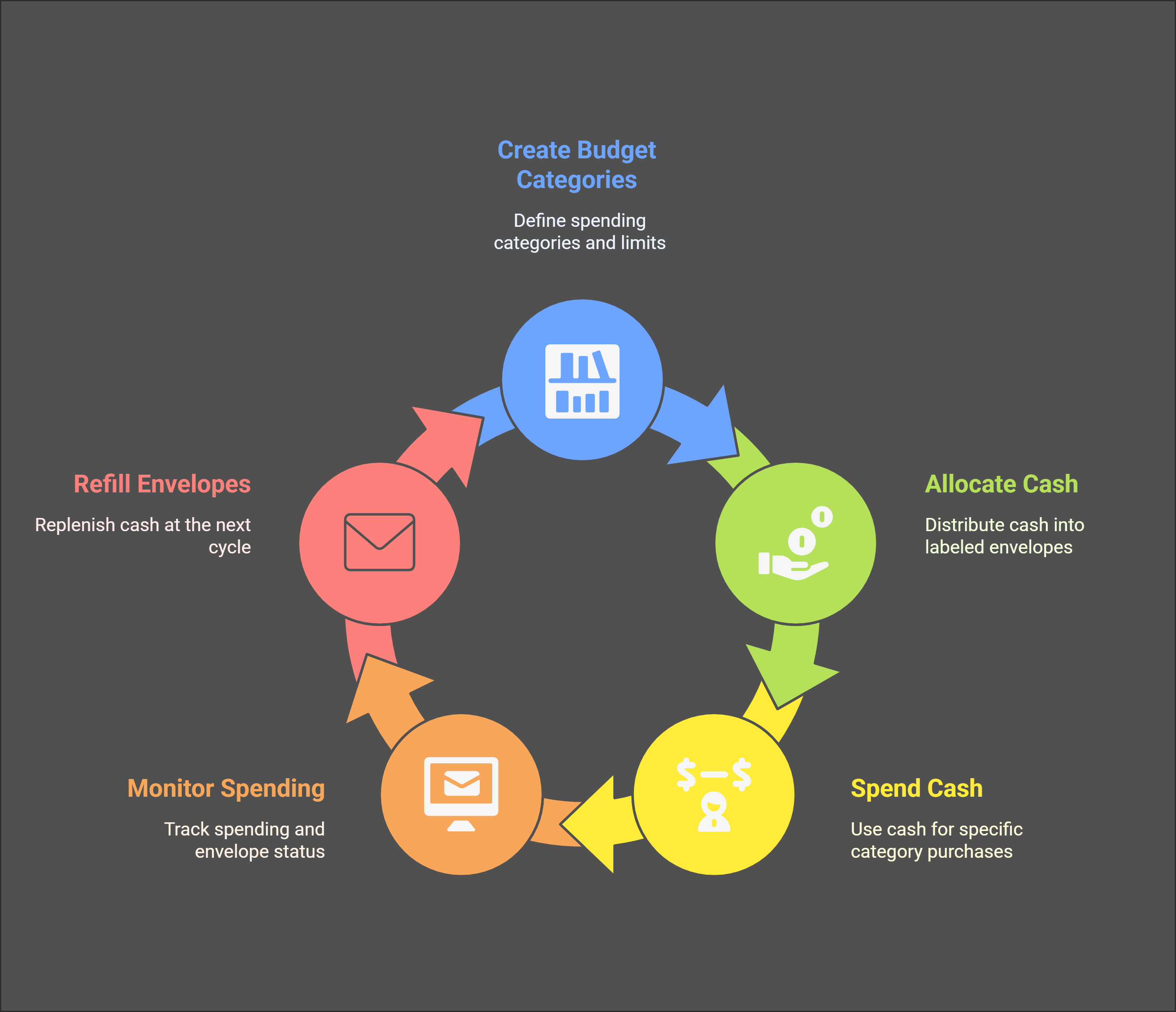

Cash stuffing is basically a fancy term for the cash envelope budgeting system. The concept has been around for decades: you allocate a set amount of cash to different spending categories by keeping physical money in labeled envelopes. Once an envelope is empty, you stop spending in that category until it’s replenished at the next paycheck.

On TikTok, #CashStuffing became a viral phenomenon in 2022-2023 as many young adults turned to this tangible method to get a grip on their finances. There’s something satisfying about literally stuffing money into envelopes – it makes budgeting feel more real and controlled than just numbers on a screen.

Here’s how it works in a nutshell:

- You create budget categories, typically for flexible spending like Groceries, Dining Out, Gas, Fun Money, Clothing, etc.

- For each category, you have an envelope (physical paper envelope or a section in a cash binder). You decide how much money goes into each for the month or pay period.

- On payday or at the start of the month, you withdraw cash and fill your envelopes. e.g. $300 into “Groceries”, $100 into “Eating Out”, $50 “Clothes”, $60 “Entertainment”, etc., based on your budget plan.

- Throughout the month, you pay with that cash for the respective category. When you grocery shop, you use money from the Groceries envelope only.

- When an envelope runs out, that’s it – you’ve hit your budget for that category. No dipping into other funds or using credit; you wait until the envelope is refilled next cycle.

The forced limit is what makes it powerful: it’s a visual and physical cue of how much you have left to spend. No more guessing or overspending – if there’s $0 in “Fun Money,” you know tonight is a Netflix-at-home night instead of going out.

TikTokers have glamorized cash stuffing with aesthetic budget binders, ASMR videos of cash, and decorating envelopes – making budgeting oddly satisfying to watch. But beneath the fun visuals, the appeal is real: cash stuffing brings discipline and awareness. It’s budgeting in a touchable form, which can be helpful if swiping cards makes it too easy to overspend.

How to Start Cash Stuffing – Step by Step Guide

Ready to give cash stuffing a try? Follow these simple steps to set up your own envelope budget:

List Your Spending Categories:

First, figure out which budget categories you want to control using cash. Common ones are: Groceries, Restaurants/Takeout, Gas, Entertainment, Clothing, Personal Care, Miscellaneous. You typically don’t do envelopes for fixed bills like rent or utilities – those are better paid online. Envelopes are great for variable expenses where you tend to overspend.

Decide Your Budget Amounts:

Look at your income and expenses. How much can you realistically allocate to each chosen category per month or per paycheck? For example, maybe per paycheck you allot $150 to groceries, $40 to coffee/dining out, $30 to fun, etc. Make sure the total of all your envelope budgets is less than or equal to your take-home pay minus fixed bills and savings. This ensures you’re covering essentials and goals first.

Prepare Your Envelopes:

You can go low-tech with plain envelopes and a pen, or get a cute cash stuffing binder with labeled pouches – whatever motivates you. Label each envelope with the category name. (If you want to be extra, decorate them or color-code – anything to make budgeting feel enjoyable!).

Stuff the Cash (Payday Routine):

On payday, head to the bank (or ATM, but bank tellers can give specific bill denominations which is handy) and withdraw the total cash you need for envelopes. Then divide the money according to your plan. For example: put $150 in Groceries, $40 in Dining, $30 in Fun, etc., until all envelopes have their allocated cash. Pro tip: Keep smaller bills for flexibility (a $100 bill in “Food” is harder to budget with than smaller bills you can pull out for smaller trips).

Spend from the Envelopes Only:

Now as you go about your week, spend only the cash from the correct envelope for each expense. Going to the movies? Take $20 from “Entertainment.” Grocery shopping? Bring your Groceries envelope. Leave your cards at home if possible to avoid temptation. This step trains you to live within the set limits.

Stop When It’s Empty:

This is the hard but crucial part – if an envelope is out of money, pause that type of spending. If your “Eating Out” envelope had $40 and you used it up in two weeks, then for the rest of the month you’d cook at home or use your Groceries envelope instead. No refilling from elsewhere! This boundary is what helps curb overspending. It might feel restrictive at first, but it’s also kind of like a challenge or game.

Rollover or Reallocate at Month End:

At the end of the month or before your next refill, see what cash is left. You can decide to roll it over (keep it in that category for next month, possibly reducing how much new cash you add), or reallocate it. Some people take leftover cash and put it toward savings or debt – a nice bonus for coming in under budget! Others leave it to build a buffer. Choose what fits your goals.

And that’s the basic cycle. It may take 1-2 months to fine-tune the amounts. If you consistently run out too fast in Groceries but always have surplus in Clothing, adjust the allocations. The beauty of cash stuffing is that it forces you to really observe your spending habits and adjust in a tangible way.

Pros and Cons of Cash Stuffing (Is It Right for You?)

Why people swear by cash stuffing:

- Tighter Control: You literally can’t overspend beyond your budget if you stick to the system – the cash simply isn’t there once it’s gone. This is great if you struggle with impulse buying or going overboard on your credit card.

- Better Awareness: Handing over physical cash makes you feel the spending more than a quick card swipe. It creates awareness. Many find they spend less when they see the envelope thinning out.

- No Surprise Bills: Since you’re not putting those expenses on a credit card, you won’t get a big statement later. Fewer bills to juggle, and no risk of interest or debt for those categories. It’s all pay-as-you-go.

- Great for Beginners or Reset: If you’re new to budgeting or need a financial reset, this method is straightforward and forces good habits. It’s very clear-cut, which can be reassuring.

- Encourages Saving Leftovers: If you have money left in envelopes, you can easily set it aside as savings. It feels “extra” since you didn’t need it – kind of a reverse psychology that can boost your saving rate.

Downsides to consider:

- Inconvenience: Let’s face it, we live in a digital world. Carrying cash for everything can be inconvenient (and sometimes less safe). You might not always have the exact amount, or you may forget an envelope at home. Plus, some purchases are just easier online or by card.

- No Card Rewards: Using only cash means you miss out on credit card rewards or cash back you could earn on those purchases. For example, if you spend $500/month on various things in cash, you’re forgoing maybe $5-$15 in rewards (depending on your card’s rate). Over time that adds up – something to weigh if you love points and miles.

- Not Building Credit: Similarly, if you rely solely on cash, you won’t be using credit much, which is fine short-term but building a good credit history is important. You’ll want to at least keep a credit card active for some bills or occasional use.

- Cash Security: Keeping a lot of cash at home or in your wallet has risks (loss, theft). Be mindful – perhaps don’t stuff huge amounts, or find a secure way/place to store your envelopes.

- Rigidity: Life isn’t always predictable. You might have an empty “Car Gas” envelope but really need to drive somewhere. In strict theory, you’d stop driving – but that’s not practical. So you need a bit of flexibility and judgment; sometimes you may break the envelope rule (and that’s okay if you adjust elsewhere).

Who does cash stuffing work best for? Likely those who need a disciplined structure to get spending under control, and don’t mind using cash. If swiping cards has gotten you into trouble before, this could be a game-changer to rebuild good habits. It’s also popular among people who enjoy the ritual of budgeting – if you like organizing or tactile processes, stuffing envelopes can actually be fun (seriously!).

Others who might not benefit: if you’re already pretty disciplined with a digital budget, switching to all-cash might feel like a hassle with not much added value. Or if you do all shopping online (where cash isn’t an option), you’d have to adapt the method significantly.

Modern Twists – Digital “Cash Stuffing” and Using Kudos for Rewards

You can absolutely adopt the principles of cash stuffing without strictly using cash for everything. The goal is controlled, category-specific spending.

Here are a few modern adaptations:

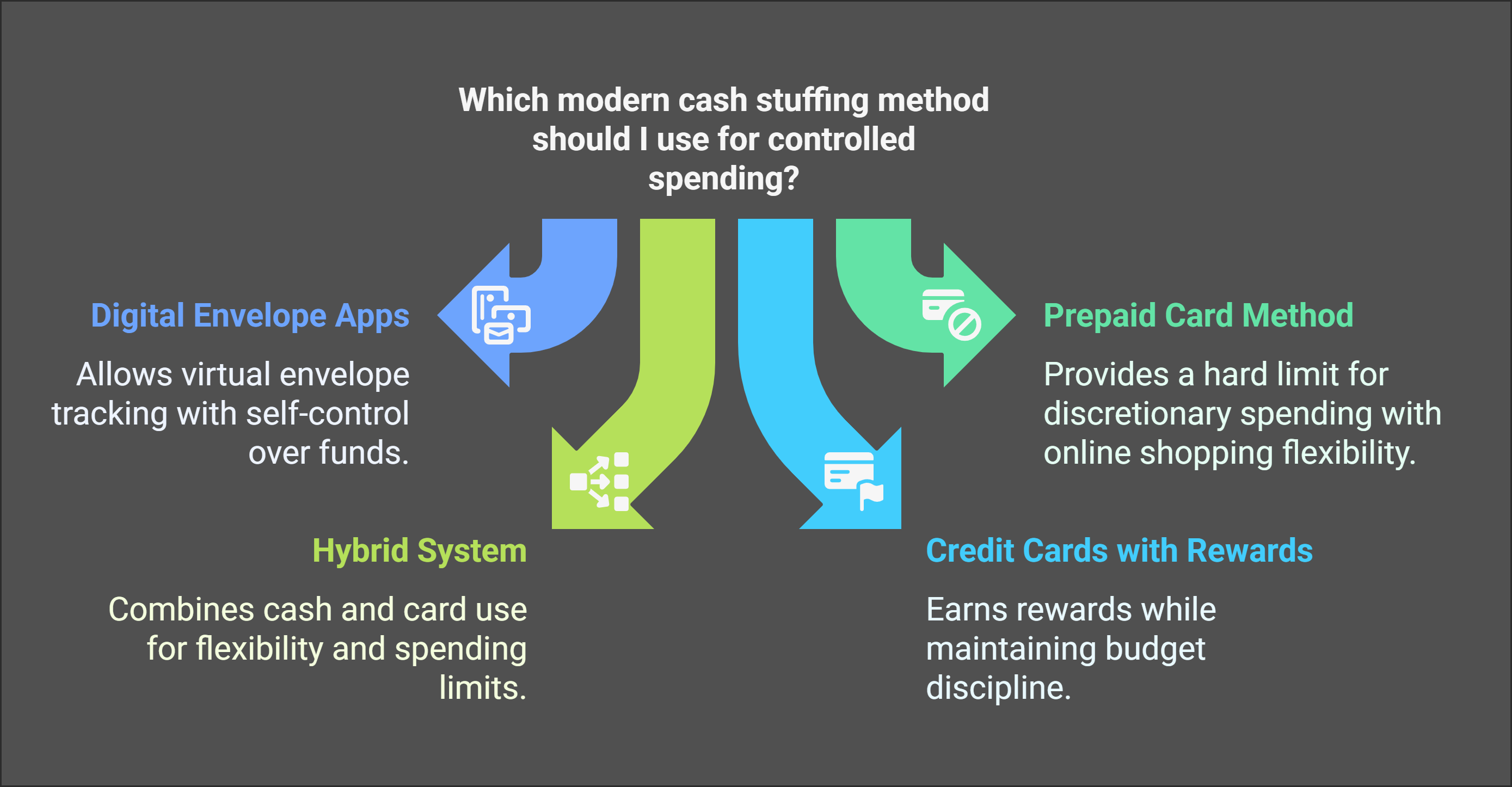

Digital Envelope Apps:

There are budgeting apps (like Goodbudget, or even features in Mint/YNAB) that let you allocate money into virtual “envelopes.” You could keep your money in the bank but track as if you had envelopes. Some people do this by having multiple checking accounts or sub-accounts for categories. It requires self-control (not pulling extra funds), but it’s doable and keeps things digital.

Prepaid Card Method:

Another hacky approach: Load a prepaid debit card with your fun money for the month. That card becomes your “envelope” for discretionary spending – once its balance hits zero, you stop. This way you can shop online or use a card, but still have a hard limit separated from your main funds.

Hybrid System:

Many find a mix works best. For example, use cash envelopes for groceries, dining out, and personal spending (where you tend to overspend), but pay other things like gas or subscriptions with a credit card. That way you reduce cash carrying and still enforce limits where needed.

Using Credit Cards Responsibly:

Believe it or not, you can still follow an envelope mindset with credit cards – it just takes discipline. One idea: continue to budget with envelopes, but instead of spending the cash, you use your credit card for the purchase and immediately remove that amount of cash from the envelope and set it aside to pay the card bill. At the end of the month, deposit that cash and pay off the card. This way you earn rewards on the card but never overspend, because the cash envelope was your guide. It’s a bit advanced but it combines the best of both worlds.

Where does Kudos fit in? If you’re a fan of credit card rewards (who isn’t, free money is nice!), Kudos can help you integrate rewards into a cash stuffing lifestyle. For instance:

Suppose you want to keep using a credit card for groceries to get 2% cashback, but you fear overspending. You could set a “Groceries” envelope but instead of cash, put an index card noting the budget (say $300). Each time you grocery shop with your card, use the Kudos extension at checkout (if shopping online) or check your Kudos app to ensure you’re using the best rewards card for that grocery spend.

After the purchase, deduct that amount from your envelope’s balance (you could even put the receipt in the envelope). You still stop when you hit $0 on paper, but you also rack up rewards. Kudos basically ensures every dollar you do spend works harder for you via points or cashback.

Another scenario: Let’s say you’re following cash stuffing, but you allow yourself one online purchase a month (maybe for something like Amazon or a treat). When that time comes, you won’t be using cash – so use Kudos’s recommendation to pick which of your cards to use for that purchase to maximize rewards. It’s like having a friend whisper, “hey, use the XYZ card here, you’ll get 5% back,” ensuring that even when stepping outside the cash system, you’re not leaving money on the table.

Lastly, if you do the aforementioned hybrid method of using a card then pulling cash from your envelope, Kudos just makes sure the card choice is optimal. For example, maybe you have a gas envelope but use a gas credit card for the discount – Kudos would remind you of that when you’re buying gas.

In short, Kudos can supercharge your cash stuffing strategy by introducing rewards into the mix wherever possible, and by helping you stay aware of which spending is happening on which card (useful if you’re juggling a hybrid system).

Final Thoughts – Should You Try Cash Stuffing?

Cash stuffing isn’t magic, but it can feel magical when you see it working. By simply limiting yourself to available cash, you might find you spend far less and finally break the paycheque-to-paycheque cycle. If you’re intrigued, give it a test for a month or two. You don’t have to commit forever – see if it helps you spend more mindfully.

Many who try it say they gained a new appreciation for money – $20 in an envelope suddenly felt more valuable than the same $20 on a card. If that happens, you’re on the right track. Over time, you might loosen the cash strictness once you’ve trained your habits. Or you may stick with it long-term because it simply works for you.

Remember, personal finance is personal. What matters is finding a system that helps you achieve your goals (whether that’s saving more, paying off debt, or just not feeling broke before payday). Cash stuffing is one tool out of many – and now you understand how to use it effectively.

Even if you don’t adopt it 100%, you can take lessons from it: such as the power of budgeting by category, the importance of setting hard limits, and the benefit of being intentional with every dollar. Those lessons apply whether you’re transacting in cash, card, or crypto.

So, grab some envelopes (or an app), plan out your budget, and try “stuffing” for yourself. It might be the tactile change that makes money management click for you. And don’t forget, you can still enjoy your modern perks (hello, credit card rewards) alongside the envelope method by being a little creative (and using tools like Kudos to guide you).

Happy budgeting – may your envelopes always overflow (in the best way)! 💰✉️

FAQ (Cash Stuffing)

Does cash stuffing really save you money?

It can! Cash stuffing helps many people spend less because it imposes strict limits. When you only have, say, $100 for “fun money” in cash, you’re far less likely to overspend compared to using a credit card with a high limit. It doesn’t magically give you more money, but it helps you control the money you have. By preventing overspending, you end up saving more or having cash left over which you can then actually save.

What do I need to start cash stuffing?

At minimum, you need some envelopes (or cash pouches) and discipline to only use the cash you’ve set aside. You’ll withdraw cash for each budgeting period and sort it into envelopes labeled by category (like groceries, entertainment, etc.). Optionally, you can buy a dedicated cash stuffing binder or wallet which has sections for each category – many find this keeps things organized and fun to use. Other than that, just your budget plan and the cash itself!

Can I do cash stuffing without carrying cash everywhere?

Yes, there are a few ways to adapt it:

- You can use a budgeting app with an envelope feature to simulate cash stuffing digitally. You’d track spending against those virtual envelopes, which requires self-reporting but no physical cash.

- Another method is the “cashless cash stuffing” approach: still budget by category, but use a single debit card for those expenses and keep a written log or use a spreadsheet as your “envelope.” It’s a bit more work to track, but it avoids carrying cash.

- Some people use multiple bank accounts or prepaid cards to mimic envelopes (e.g., a separate account for dining out). When one account’s funds are used up, you stop spending from it.So, while the classic method uses paper money, you can absolutely tweak it to suit a more digital lifestyle – just ensure you maintain the spending limits that make cash stuffing effective.

What if I have cash left in an envelope at the end of the month?

That’s a good problem to have! It means you underspent your budget in that category. You have a few options:

- Roll it over: Keep the extra cash in that envelope and add less new cash next month (since you already have a head start). This could allow you to gradually shrink some category budgets if you consistently underspend.

- Reallocate it: Move the leftover to another envelope that might have run short, or use it for a one-time treat.

- Save it or pay debt: A popular choice is to take all envelope leftovers and put them towards a savings goal or debt payment. This way you accelerate your financial progress. There’s no wrong answer – just make sure the leftover money is put to use in a way that aligns with your goals (and doesn’t just mysteriously disappear on something unplanned!).

Is it okay to use a credit card while doing cash stuffing?

You can, but you need to be careful. The pure form of cash stuffing avoids cards to prevent overspending and debt. However, you can incorporate credit cards strategically:

- Use your card for categories not in your cash system (like paying utility bills or online purchases) while still using cash for your envelope categories.

- Or, if you use a card for an envelope expense (say you had to order something online for “clothing”), deduct that amount from the envelope immediately and set it aside to pay the card bill. This keeps you within budget and you can pay off that charge right away.

- If you’re confident in your discipline, you might do a hybrid as mentioned: track your envelope balances but spend on a card and regularly pay it down. The key is: never spend on the card beyond what your envelope budget allows, and always pay the card off to avoid interest. Some cash stuffers do this to earn points or cashback on purchases while still sticking to the plan. It requires a bit more effort, but it can work. Just make sure the convenience of the card doesn’t tempt you to overspend what’s in your envelopes.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)