Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Commercial Umbrella Insurance 101: What Is It & Why You Need It (2026)

July 1, 2025

Commercial umbrella insurance is an extra layer of liability protection for your business – it kicks in when a major claim exceeds the limits of your other insurance policies. In other words, it’s a financial safety net that guards your company against catastrophic losses that would otherwise go beyond the coverage of standard policies.

If 2025 has taught business owners anything, it’s that lawsuits and large claims can happen unexpectedly – and that’s exactly when an umbrella insurance policy becomes invaluable.

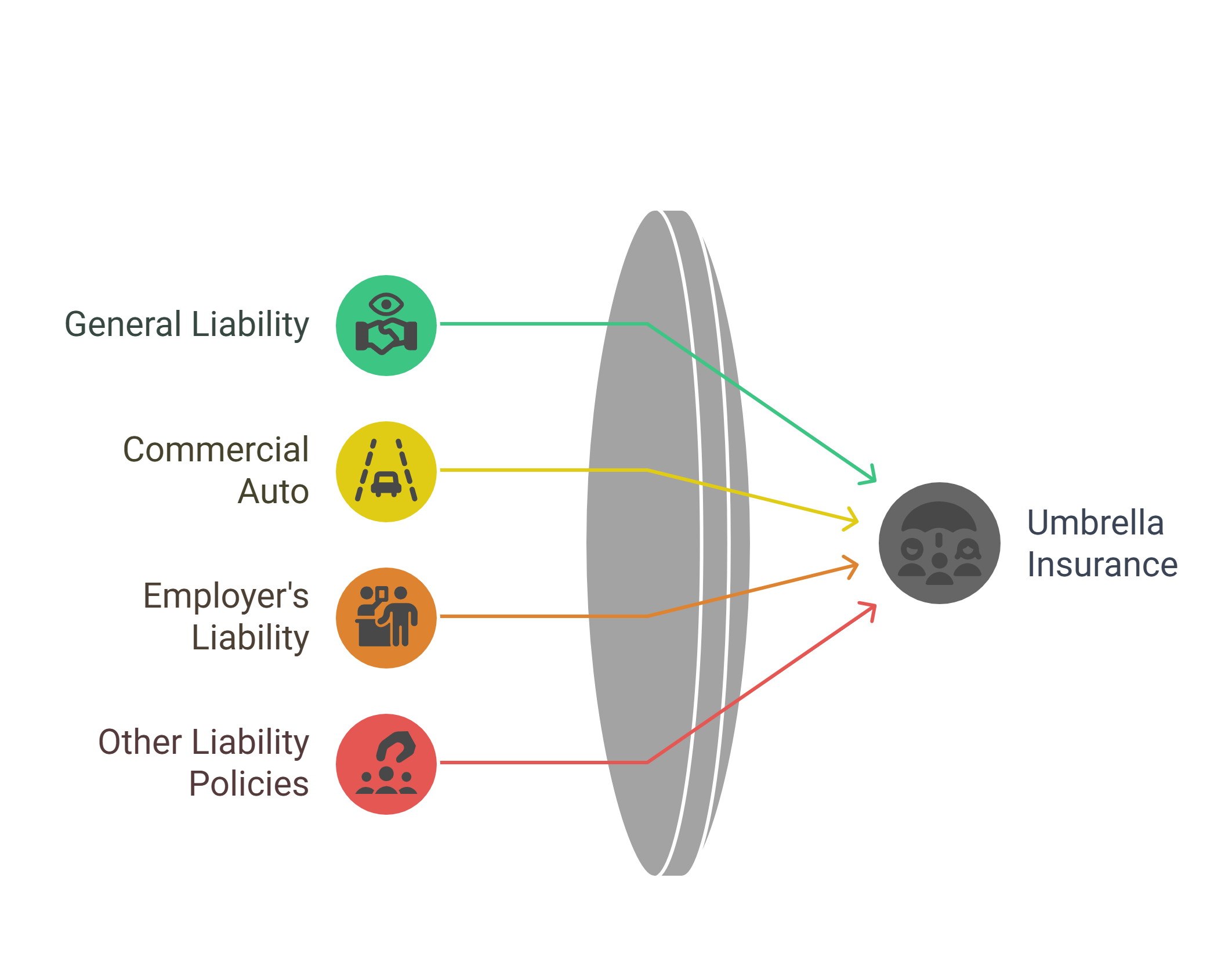

How Commercial Umbrella Insurance Works (Beyond Your Basic Policies)

Think of commercial umbrella insurance as a backup to your primary insurance. It doesn’t stand alone; instead, it sits on top of other policies like general liability, commercial auto, or employer’s liability insurance.

Here’s how it works in practice:

Exceeding a Policy Limit

Suppose your business faces a severe lawsuit – for example, a customer injury at your premises leads to a lawsuit for $1.5 million in damages. If your general liability insurance has a $1 million per-claim limit, it would pay out that $1M, and without an umbrella policy, you’d be on the hook for the remaining $500,000.

With a commercial umbrella policy, that extra $500K would be covered (up to the umbrella’s limit). In this way, the umbrella policy picks up where your primary policy left off, preventing a huge out-of-pocket loss.

Multiple Claims Aggregate

Umbrella insurance also protects against the scenario of multiple smaller claims exhausting your regular coverage. For instance, if you have a series of lawsuits or claims in one year that max out the annual aggregate limit of your underlying policy, the umbrella coverage can step in to cover claims beyond that aggregate cap.

Broader Coverage in Some Cases

In certain situations, a commercial umbrella policy might cover a claim that wasn’t explicitly covered by an underlying policy. (This is not common, and terms vary by insurer.) Umbrella insurance can act as a gap-filler for unusual liability scenarios — however, note that it’s not a catch-all for everything (more on exclusions below).

In essence, an umbrella policy extends and expands your protection. It’s important to know that you typically must carry “underlying” insurance (like a general liability policy, etc.) to purchase umbrella insurance – you can’t just buy an umbrella alone with no base coverage. Insurers require underlying policies and certain minimum liability limits on those before the umbrella kicks in.

What Does a Commercial Umbrella Policy Cover (and Not Cover)?

A commercial umbrella policy covers liability costs that exceed your other policy limits, up to the umbrella’s own limit. Here are the main things it does cover:

1. Major Liability Lawsuits

If your business is liable for someone’s injuries, property damage, or other third-party losses, umbrella insurance covers the legal expenses, court judgments, settlements, and medical bills that go beyond your primary policy’s coverage.

2. Multiple Claim Events

As mentioned, even if no single claim is huge, several mid-sized claims in the same policy period could add up to more than your general liability or other policy covers. Umbrella insurance would cover those excess amounts once the aggregate limit of the underlying policy is reached.

3. Coverage Across Multiple Policies

A big benefit is that one umbrella policy can extend over several types of liability policies. A single umbrella can bolster your general liability, your commercial auto liability, and your employer’s liability (workers comp/employer liability) all at once. This means if any one of those underlying coverages runs out, the umbrella kicks in. It’s like having one big umbrella shielding you over various rainy scenarios.

However, commercial umbrella insurance does NOT cover everything. Despite the name “umbrella,” it has its own exclusions and limits. Common things not covered include:

- Professional Errors: Mistakes in professional services (those are covered by E&O or malpractice insurance, not by umbrella).

- Property Damage to Your Own Property: Umbrella policies won’t cover damage to your business’s own property or equipment – that’s what commercial property insurance is for.

- Contractual Liability and Warranty Issues: If something is not covered in an underlying policy at all (outside normal liability tort claims), umbrella likely won’t cover it either. It generally follows the coverage terms of your primary policies.

- Intentional or Illegal Acts: No insurance, including umbrella, will cover intentional harm or fraudulent acts. Umbrella is meant for accidents and unforeseen liabilities, not willful misconduct.

In short, a commercial umbrella policy extends coverage, but doesn’t invent new coverage that you didn’t have. If in doubt about a particular scenario, check with your insurer on whether it’d be covered by umbrella or if you need a different type of policy.

Why Your Business Might Need Umbrella Insurance in 2025

You might be thinking, “I already have general liability and other policies… do I really need an umbrella on top?” For many businesses, the answer is yes – especially as we see rising lawsuit costs.

Here are key reasons why umbrella insurance is a smart move:

1. Lawsuits Are More Common (and Costly) Than Ever

We live in a litigious society. Roughly 36% to 53% of small businesses are involved in litigation in a given year. Even if your business is careful, you could be hit with a surprise lawsuit that seeks an amount far beyond your insurance limits. Large jury awards and settlements are becoming more frequent. Umbrella insurance provides peace of mind that one freak incident won’t bankrupt your company.

2. Extra Protection for High-Risk Businesses

Some businesses inherently face greater liability risks. For example, if you have a premises open to the public (foot traffic), like a retail store or restaurant, the chance of a customer injury (and a big claim) is higher. Or if your employees work on clients’ properties (contractors, cleaners, repair services), you could accidentally cause expensive damage and be liable for it.

3. Coverage for Serious Auto Accidents

Commercial auto policies have limits – if your delivery truck causes a multi-car pileup, the lawsuits could exceed your auto liability coverage. Umbrella insurance would cover the overflow. Businesses with fleets or drivers on the road a lot (delivery services, trucking, etc.) should have umbrella coverage as a safeguard, given the high cost of severe auto accidents.

4. It’s Required or Expected in Contracts

You might have clients or contracts that require you to carry umbrella insurance. This is common in government contracts or large corporate clients – they want assurance you have X million in coverage. Often, you can meet the requirement by combining base coverage with an umbrella.

5. Relatively Low Cost for High Coverage

Considering the protection it offers, umbrella insurance is affordable for the amount of coverage you get. (We’ll dive into specific costs in a later article, but in many cases $1 million of umbrella coverage can cost a small business under $1,000 per year – which is a fraction of a single large claim’s cost.) This cost-benefit makes it a no-brainer for many businesses – essentially trading a small certain expense for coverage against a potentially business-ending event.

6. Covers Multiple Bases at Once

Instead of raising the limits on each of your individual policies (which can be costly per policy), one umbrella policy can boost all of them. This one policy blanket approach is often simpler and more cost-effective to get higher overall coverage.

Protecting your business is crucial – and it’s also a great time to review your other insurance. For example, while thinking about liability coverage, make sure your personal policies are in order too. Kudos simplifies comparing auto insurance rates, quickly finding the best rate tailored for you. It’s easy and completely free. With your business and personal assets both shielded by the right insurance, you can focus on growth with peace of mind.

How Commercial Umbrella Insurance Fits Into Your Insurance Plan

Commercial umbrella insurance isn’t a standalone fix; it’s part of a holistic risk management plan. You should already have primary insurance like:

- General Liability Insurance: Covers bodily injury or property damage claims from third parties (customers, visitors).

- Commercial Auto Insurance: Covers vehicle liability if your business owns cars/trucks.

- Employer’s Liability (often part of workers’ comp): Covers certain lawsuits from employee injuries beyond workers comp.

- And any other liability policies specific to your business, such as liquor liability, etc., if applicable.

The umbrella sits on top of these. It typically comes into play only when those underlying policies hit their limit. Important: insurers will usually require you to maintain certain minimum limits on underlying policies (e.g., you might need $1M of general liability coverage and $1M auto liability coverage) in order for the umbrella to function. If you have very low primary limits, you may need to increase them to purchase umbrella coverage.

Also, umbrella coverage usually comes in $1 million increments. A common purchase for a small business might be a $1M or $2M umbrella. Larger companies or those with more risk can get $5M, $10M or even higher umbrellas (often by layering policies). The good news is that umbrella policies are flexible – you can choose the coverage amount that makes sense, and you can increase it later if needed as your business grows or faces new risks.

By adding a commercial umbrella policy, you essentially raise your liability ceiling across the board. It ensures that a bad day doesn’t turn into a financial disaster. For many business owners, that added security is worth its weight in gold (or at least worth its annual premium).

Frequently Asked Questions (FAQ)

Is commercial umbrella insurance the same as excess liability insurance?

Not exactly. Both provide coverage when a claim exceeds your primary policy limits, but excess liability applies to one specific policy (like just your general liability), whereas a commercial umbrella can cover multiple policies at once.

How much umbrella insurance coverage should I carry for my business?

It depends on your risk exposure and assets. Common guidance is to get enough to cover your worst-case scenario liability. Many small businesses get $1–5 million in umbrella coverage. If you have significant assets or operate in a high-risk industry (construction, transportation, etc.), leaning towards the higher end is wise.

Does a commercial umbrella policy have a deductible?

Typically, no separate deductible. The “deductible” for an umbrella is essentially the exhaustion of the underlying policy. In insurance lingo, umbrella policies often have a retained limit or require “underlying limits” to be paid out first. Once your primary insurance has paid its maximum, the umbrella kicks in without you paying an additional deductible.

Is commercial umbrella insurance tax deductible for my business?

In most cases, yes. Business insurance premiums, including liability and umbrella insurance, are considered a business expense. According to the IRS, you can deduct the ordinary and necessary cost of insurance for your trade or business. So the premium you pay for a commercial umbrella policy is usually tax-deductible as a business expense.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)