Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Gen Z’s Guide to Credit Card Rewards: Build Credit, Earn Perks & Avoid Pitfalls

July 1, 2025

Entering the world of credit cards as a Gen Z adult can be exciting but also a little intimidating. You’ve heard the horror stories of debt, yet you see influencers flying “for free” with points. So, what’s the deal? This guide breaks down the credit card rewards basics for Gen Z – from building your credit safely to racking up points and cash back, all while steering clear of common mistakes. Consider this your Credit Cards 101, tailored for the digital generation.

Why Credit Cards Matter for Gen Z

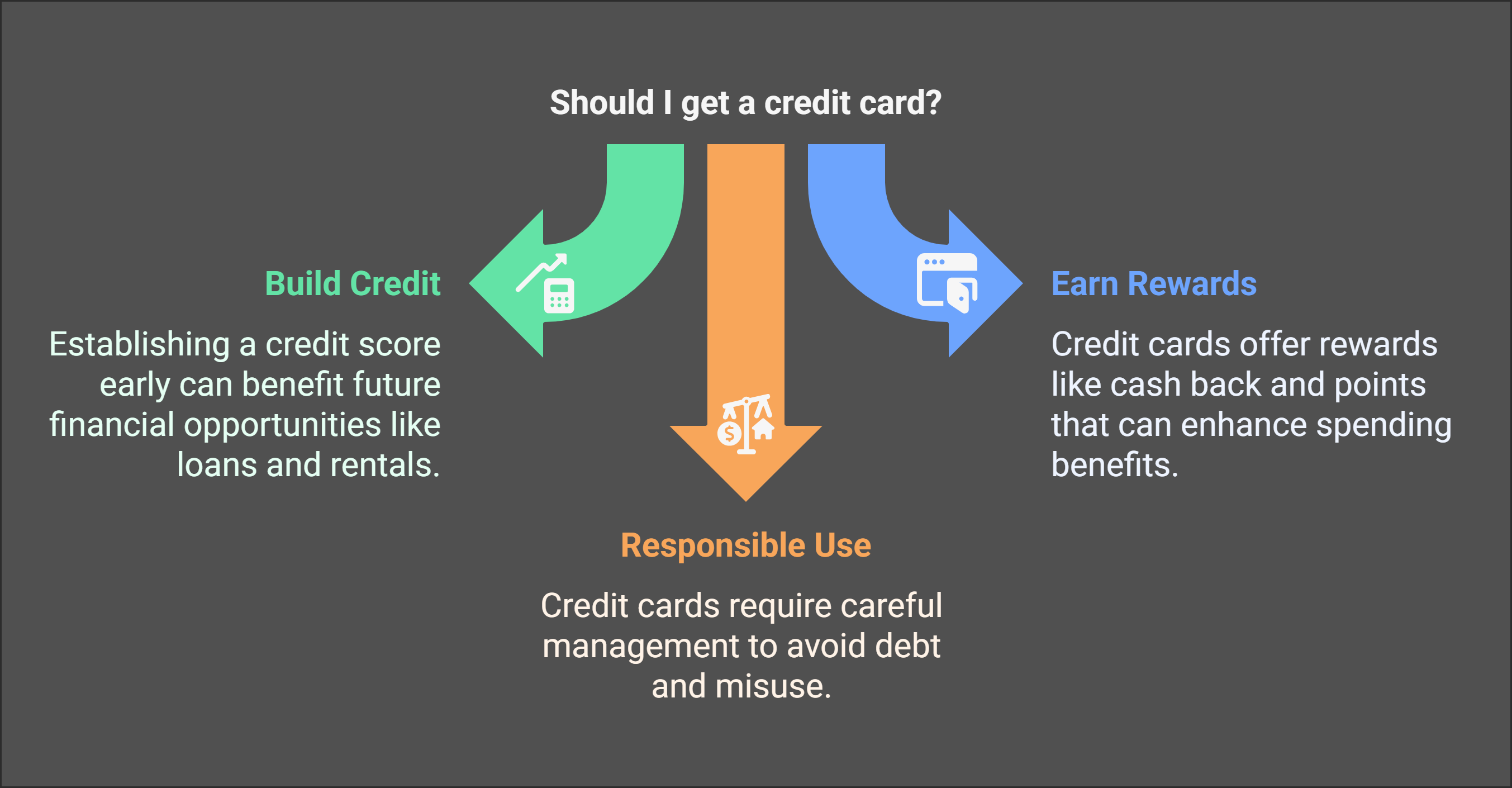

If you’re between 18 and 25, you might wonder: Do I even need a credit card? In one word: Yes (eventually). Here’s why: Credit cards help you build credit. Your credit score is like a financial GPA – it matters for renting apartments, getting car loans, and sometimes even job applications.

Starting young can give you a head start on a good score by the time you’re in your mid-20s. Plus, credit cards offer rewards (cash back, points, miles) that debit cards and cash don’t. Used wisely, they literally pay you back on your spending. Many Gen Zers are misinformed about credit but in reality, the earlier you start building responsible credit habits, the better off you’ll be. That said, credit cards are a tool, not free money. This guide will show you how to wield that tool to your advantage.

Step 1: Build Your Credit (Without Going Into Debt)

Before worrying about rewards, establishing good credit is priority #1. Here’s how:

- Start with a beginner-friendly card: Look at student credit cards or secured cards if you have no credit. These have high approval odds for first-timers. For example, a student card might have a $500 limit – use it for small purchases. Even a secured card (where you put down a deposit) can be a stepping stone; some secured cards, like Discover it Secured, actually earn cash back while you build credit.

- Use the card regularly, but lightly: Aim to spend under 30% of your credit limit in a given month (under 10% is even better for your score). So if you have a $500 limit, keep your statement balance below ~$150. This shows you’re not maxing out credit and is good for your credit utilization ratio.

- Pay on time, always: This is non-negotiable. Even one 30-day late payment can tank your credit score for years. Set up autopay for at least the minimum due, so you never miss a payment. Pay in full if you can (more on that in a second). Payment history is the #1 factor in your credit score. Nail this, and you’re golden.

- Don’t carry a balance thinking it builds credit – it doesn’t. There’s a persistent myth (perhaps your friend or even parent told you) that carrying a small balance month-to-month improves your score. False! 66% of Gen Z believes you must carry a balance to build credit – but that’s a myth. You can (and should) pay off your balance in full each month. You’ll build credit just by using the card and paying on time; you do not need to incur interest. In fact, paying in full helps you avoid debt and keeps your utilization low, both good for your score.

- Set a low credit limit for yourself mentally: When you get a card, you might suddenly have a $1,000 limit – woohoo! But pretend your limit is something like $200 or whatever you know you can pay off. This way you won’t overspend. It’s easy to swipe now and worry later; avoid that trap by budgeting.

- Monitor your credit: Use free tools (Credit Karma, Experian app, etc.) or your card’s free FICO score feature to track your credit score. It might start around thin credit range (maybe no score until you have six months history, then perhaps in the 600s). Over a year or two of good behavior, you’ll see it climb. This feedback is motivating! Also, check your credit report for errors once a year (annualcreditreport.com) – identity theft can happen, and as digital natives Gen Z should be vigilant.

By building credit early, you set yourself up for better financial opportunities. And you’ll qualify for cards with higher rewards down the line. Think of it as leveling up in a game – you have to grind a bit at first (with a starter card) to unlock the really cool stuff (premium reward cards).

Step 2: Earn Rewards on Everyday Spending

Once you have a card (or once you’re comfortable with the idea of using one regularly), make sure you’re earning something back. Most beginner cards offer cash back because it’s straightforward. For example, 1% or 2% back on purchases, or bonus categories like 5% on gas or groceries.

If you got a student card or a secured card, check its rewards program. Some secured cards give no rewards – if so, use it to build credit for ~6-12 months, then try to upgrade to an unsecured rewards card.

How to maximize those everyday rewards:

- Put as many of your normal expenses on the card as possible (without overspending). If you normally spend $200 a month on things like groceries, gas, Netflix, and Starbucks, putting that on a 1.5% cash back card yields $3 back. That’s a few free coffees a year for doing nothing extra. If your card has 5% rotating bonuses, make note of when it’s 5% for categories you use – and lean in.

- Use your card for bills that accept credit with no fee. Many Gen Z handle subscriptions (Spotify, Hulu, gym, etc.). Put them on your card to rack up monthly rewards and then set your card on auto-pay. It’s a set-and-forget way to earn. Just watch out for any bills that charge a processing fee for credit cards (some utilities or tuition payments do – in those cases, it might not be worth the fee).

- Pay in full each month (repeating this because it’s so crucial). If you pay in full, the rewards you earn are pure gain. If you don’t, you’ll get interest charges. Think of it this way: carrying a balance is the opposite of a reward, it’s a penalty.

- Watch out for welcome bonuses you can handle: If your first card has a sign-up bonus for spending, say, $500 in 3 months and that aligns with your budget, go for it! That could be $50-$200 extra in rewards – a great jumpstart. But never spend extra or buy things just to hit a bonus. Only use bonuses that naturally fit your planned spending.

- Track your rewards and celebrate milestones: It’s fun to see your cash back tally grow or your points stack up. Some apps or the card’s site will show your rewards balance. When you hit a milestone (like $100 cash back or enough points for a free flight), celebrate it! Maybe redeem for something nice. This positive reinforcement keeps you engaged and using the card responsibly.

In short, make your credit card your financial sidekick. It’s there for virtually all your regular transactions, quietly earning while you focus on life. With pay-in-full and mindful spending, you’ll never pay a dime of interest, and you’ll accumulate rewards in the background.

Step 3: Avoid Common Pitfalls (Don’t Let Rewards Trick You)

Credit card companies dangle rewards because they want you to use the card – and possibly slip up. Here are some pitfalls Gen Z should dodge:

Overspending for rewards:

It’s psychologically proven that people tend to spend more on cards than cash. And when you attach rewards (“I’ll get 5% back if I buy this!”), it can encourage extra spending. Don’t let the tail wag the dog. A good hack: still budget in real terms. If you’re using a credit card, maintain a separate log or app that deducts from your checking account each time you swipe, as if you paid cash.

This keeps you grounded so you’re not blindsided by the bill. Remember, if you spend $100 to get $5 back, you still spent $95. Ensure that $95 was something you actually needed or wanted and could afford.

Carrying a balance (again, because it’s the biggest pitfall).

We addressed this, but to reinforce: carrying a balance not only incurs interest, it can also hurt your credit if it gets too high relative to your limit. A large balance relative to your limit (even if you’re paying on time) can increase your credit utilization and lower your score. Many Gen Zers saw parents struggle with credit card debt; learn from that and keep balances low.

If you ever do find yourself unable to pay in full, make at least the minimum payment by the due date to protect your credit, then formulate a plan to get rid of that debt. Maybe cut back next month or use savings to knock it out. Also stop using that card until you’re back to zero, to avoid digging deeper.

Applying for too many cards too fast:

When you first discover credit cards and their rewards, it might be tempting to apply for a bunch (so many bonuses! so many different perks!). But slow down. Each application can slightly ding your credit score with a hard inquiry. Plus, handling multiple new accounts is tricky.

Space out your credit card applications – a good rule is no more than one every 6 months while you’re new to credit. That way you can build a solid history on each and not confuse your budgeting. It’s true that having multiple cards can maximize rewards (as we discussed in other articles), but in your first couple years of credit, 1-2 cards are plenty. Give yourself time to adapt.

Ignoring terms and fees:

Gen Z is known to be digitally savvy but sometimes skims fine print. Take a few minutes to know your card’s terms. Does it have an annual fee after the first year? (Some student cards might introduce one later, though most no-fee cards are truly no fee.) What’s the late fee? What’s the foreign transaction fee if you travel abroad? Knowing these prevents unpleasant surprises.

Also, if you ever slip (say, you miss a payment by a day), many cards have one-time late fee waivers or will forgive if you call – as a first-time cardholder, customer service might cut you slack. Don’t be afraid to ask. Just don’t make it a habit.

Not upgrading when the time is right:

A pitfall can also be sticking with an entry-level card too long and missing out on better rewards as your credit improves. If you started on a secured card or a basic student card, check after a year or so: you might be eligible to upgrade to a better product. Many issuers let you “product change” a student card to a regular card post-graduation, or a secured card to an unsecured (and they refund your deposit).

If your income and credit score have risen, you might snag a card with a bigger bonus or higher rewards now. Periodically evaluate if your current card still fits you. Don’t cancel old cards (especially if no fee) because their credit history length helps your score, but consider adding or upgrading to match your now adulting lifestyle.

Redemption mistakes:

Another pitfall is using your hard-earned rewards poorly. Example: using points for something like a $25 gift card when you could’ve gotten $25 cash – always take the cash unless the gift card is at a rare higher rate. Or redeeming points for merchandise (banks often overprice merchandise in points).

As a beginner, the simplest redemption is cash back statement credits, or using miles/points for travel through official channels. Avoid the flashy but poor value options (like trading points for sweepstakes entries or stuff from a catalog). If unsure, do a quick Google search: “best way to redeem XYZ points.” You’ll likely find advice.

In summary, be mindful that credit cards are a double-edged sword. The sharp edge (rewards, convenience, credit-building) can benefit you greatly – but the dull edge (debt, fees, overspending) can hurt if you fall on it. The fact you’re reading this means you’re educating yourself, which is the best defense. Now, onto the fun part: perks!

Gen Z Perks: New-Age Benefits to Know About

Credit cards have evolved. Beyond generic points, many now come with perks that resonate with Gen Z values and lifestyle.

Here are a few cool ones to watch for when choosing or using a card:

- Streaming Subscription Credits: Some cards offer monthly or annual credits for streaming services like Netflix, Spotify, Disney+, etc. For example, a card might reimburse $7 each month for a streaming service. If you’re already paying for Spotify, imagine getting that $7 back – that’s $84/year saved. Check if your card has this (it would be in the benefits guide). If so, make sure you’re charging that subscription to the card and that you’ve activated any required offer. This essentially boosts your rewards (because you’re getting value beyond cash back).

- Travel and Experiences for Young Travelers: A lot of Gen Zers are adventurous travelers. Some cards cater to this with perks like no foreign transaction fees (saving ~3% on each purchase abroad), travel insurance (coverage for trip cancellations or interruptions – super useful if a cheap flight gets canceled), or even membership to youth travel programs. They also often come with little perks like a free checked bag (on airline cards) or travel discounts.

- Purchase Protection and Warranty: Gen Z loves gadgets – phone, laptop, etc. Many credit cards automatically provide purchase protection (insuring new items against theft or damage for 90-120 days) and extended warranty (adding an extra year to the manufacturer’s warranty). So if you buy, say, a new pair of AirPods on your credit card and they get stolen a month later, you could potentially file a claim and get reimbursed – that’s like an invisible benefit worth $150+. Or if your PlayStation breaks after the 1-year warranty, your card’s extended warranty could cover repair in year 2. These perks are not top-of-mind until something bad happens – but when it does, you’ll be glad you used your card instead of cash. Always use a credit card (over debit) for major electronics purchases for this reason.

- Event Access and VIP experiences: Some cards (often those targeted at millennials/Gen Z or those from certain issuers) give access to presales for concert tickets, exclusive events, or special experiences. For example, an issuer might host cardholder-only events at a music festival or give you early access to buy Olivia Rodrigo tickets. If you see “entertainment access” mentioned in your card perks, that’s what it refers to. Take advantage of it for things you care about. It’s hard to put a monetary value on skipping the virtual line for hot tickets, but it sure feels rewarding when you snag that seat and others couldn’t.

- Cash Back Offers (Targeted): Gen Z is very online, so issuers often send targeted offers via email or app to encourage spending in certain categories. For instance, “Get 10% back at Starbucks this month, up to $5” or “Earn 5x points on your next $100 at Nike.” These are essentially mini promotions. They’re easy to overlook (since they might come as an email you delete), but try to pay attention. Activating these offers (usually a one-click action) and using them can amplify your rewards. It’s like limited-time quests in a game – optional but worth doing for bonus loot.

- Financial Management Tools: Many card issuers now provide tools that appeal to younger users: spending tracking, budgeting features, or even the ability to split purchases with friends (social payment features). For example, some apps let you tag transactions and split or request money from others – useful for roomies splitting utilities or friends sharing a trip cost. Using these built-in tools can help you stay on top of spending while enjoying the card. A huge part of maximizing credit (and avoiding pitfalls) is staying organized, and thankfully, modern credit card apps are much better at this than the stodgy interfaces of the past.

Putting It All Together

Let’s illustrate with a quick story: Meet Alex, age 20, a college sophomore. Alex gets a $500-limit student credit card (no annual fee, 1% cash back). Alex puts all grocery and coffee purchases on it, totaling ~$100 a month, and pays it off via auto-pay. By end of semester, Alex’s credit score is building nicely from consistent payments. Alex earned maybe $5-6 in cash back – not a lot, but Alex redeems it as a statement credit (essentially free money towards the bill). More importantly, Alex has built a habit of using the card responsibly.

Now Alex turns 21, gets a part-time internship, and decides to upgrade rewards. Alex applies for a cash back card that offers 5% in categories (and a $200 bonus for $500 spend). Alex uses this card for a $600 new laptop purchase for school (earns the $200 bonus + 5% back as electronics fell under a 5% category = $30, so $230 rewards). But Alex didn’t have $600 at once, so used savings to pay the card immediately, avoiding interest. That $230 effectively made the $600 laptop cost only $370 – a huge win. Encouraged, Alex continues to use the card wisely, sometimes using the older card for small stuff to keep it active.

By 23, Alex’s credit score is 750+. Alex lands a full-time job post-grad and gets a travel rewards card with a 50k point bonus. Alex’s dream is to go to Japan. Over the next year, Alex uses the travel card for all expenses, hits the bonus, and accumulates ~70k points total. Using tips learned, Alex finds a great award flight deal: round-trip to Tokyo for 70k points (would’ve cost $1,000). Boom – free trip (just pay taxes <$100). Because Alex had also read the perks, the card’s travel insurance covers a missed connection during that trip at no extra cost, saving a $200 rebooking fee.

This scenario shows how, step by step, Gen Z can go from zero credit to fully leveraging rewards for meaningful benefits, all while avoiding debt. Each stage, Alex avoided the common mistakes: didn’t carry a balance, didn’t overspend for rewards, checked perks (got that insurance benefit), and used tools (tracked spending, used sign-up bonuses).

You can do the same. It’s a marathon, not a sprint – the earlier you start good habits, the more they compound. By the time you’re in your late 20s, you could have an excellent credit score (Gen Z’s average is still catching up to older folks, but you can be ahead of the curve) and a stash of rewards that saved you thousands on travel or purchases.

Remember, Kudos is here to help along the way. It’s like a cheat code for maximizing rewards – reminding you which card to use and pointing out perks you might otherwise forget. And it’s free, which appeals to our frugal Gen Z mindset.

FAQs

Is it better to get a cash back card or a travel rewards card as a young adult?

For most Gen Z beginners, a cash back card is better to start. Cash back is flexible and easy to use – you can apply it to any expense or even directly to your bank account. Travel cards (points/miles) can offer more value per point, but that’s only useful if you actually redeem for travel and understand the somewhat complex rules.

How fast can I build a good credit score with a new credit card?

You’ll typically see a credit score after about 6 months of credit history. At that point, if you’ve done everything right (on-time payments, low utilization), you might have a decent starter score (perhaps in the high 600s). Within 12 months of consistent good behavior, it could be in the 700s. Many Gen Z who start at 18 with a card can achieve a 750+ FICO by age 20 or 21 by simply never missing payments and keeping balances low. The biggest leaps in score come from continuing these habits over time – length of credit history is a factor, so at the one-year mark you’re doing well, at the two-year mark even better, etc.

What should I do if I overspend or can’t pay the full bill?

First, don’t panic. It happens – life might throw a curveball or maybe you went a bit too hard on that shopping sale. If you find yourself unable to pay the full statement balance, here’s what to do: always pay at least the minimum due by the due date to avoid late fees and derogatory marks. Next, reassess your budget – figure out the maximum you can pay (maybe you can’t pay $500 in full, but you can pay $300, leaving $200 to carry). Pay as much as possible to reduce how much incurs interest. Then, stop using the card until you’ve paid it off. Switch to cash or debit for new spending so you don’t compound the issue. Create a get-out-of-debt plan: can you cut some discretionary spending for a month or two to funnel more money to the card? Perhaps pick up a few extra hours at work or a side gig temporarily to wipe it out. The goal is to clear the balance quickly so interest charges are minimized.

Will checking my credit score hurt my credit?

Not at all – checking your own credit score or report is considered a “soft inquiry” and has zero impact on your credit. In fact, Gen Z should take advantage of the many free ways to check credit. Most card issuers now show a free FICO or VantageScore in their app or online account. Using Credit Karma or similar services is fine too (just note those provide estimates that can differ from your FICO, but they’re still useful). Hard inquiries – the ones that can ding your score slightly – only occur when you apply for new credit (like a loan or credit card). Simply checking does nothing harmful. You could check your score every day if you wanted and it wouldn’t change it (though no need to do it that often!).

How can Kudos help me as a new credit card user?

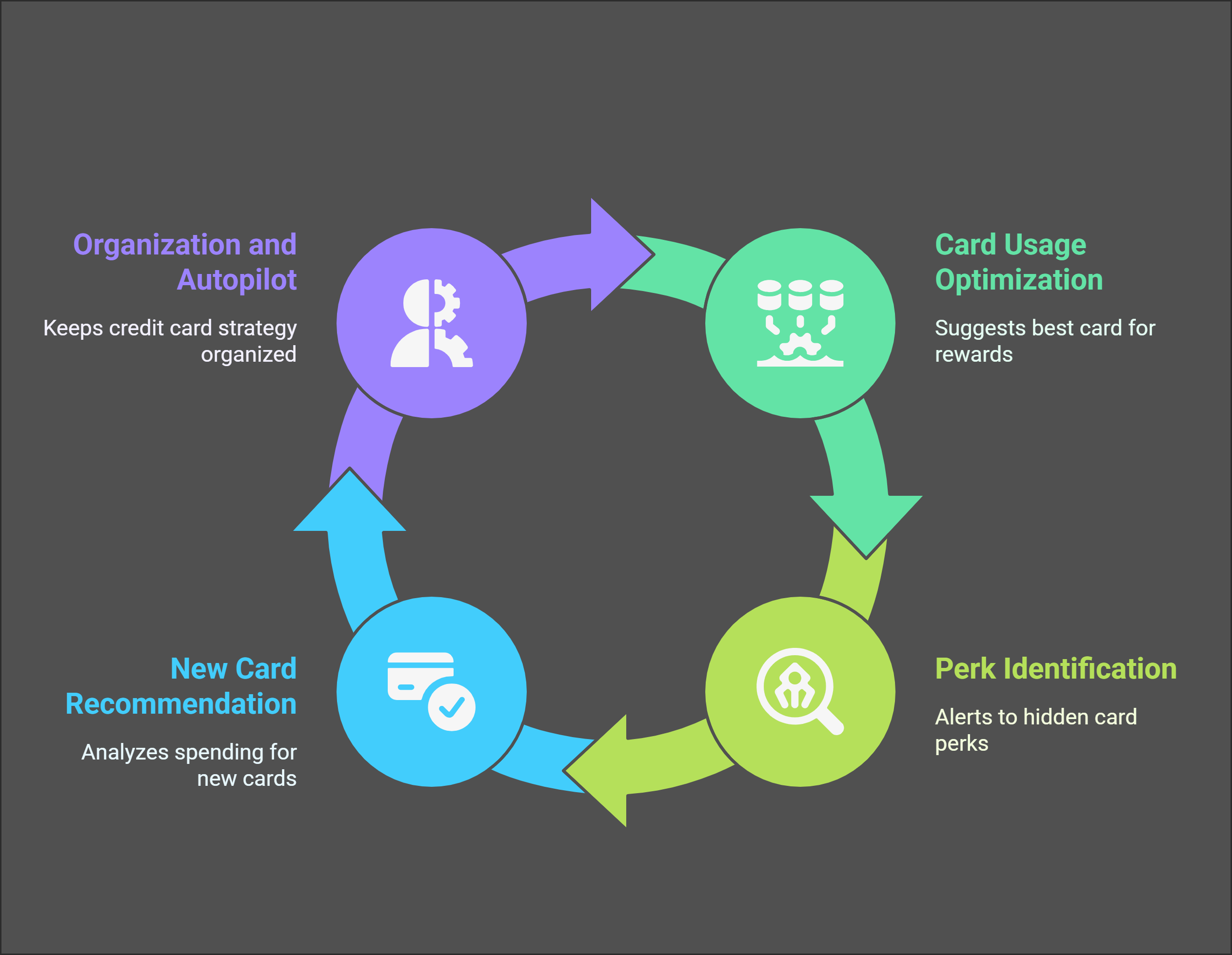

Kudos is a free tool that can be a game-changer in your credit card journey. As a Gen Z user, you’re used to smart apps that simplify life – Kudos does that for credit cards. Here’s how it helps:

- At checkout, it tells you which of your cards to use to get the most rewards.

- It alerts you to hidden perks: Maybe you’re booking a rental car and don’t realize your credit card offers free rental insurance if you use it. Kudos can highlight that, so you know which card gives you that protection.

- Helps you find the right new card: If you’re thinking of getting another card, Kudos can analyze your spending and show which card might suit you (and how many rewards you’d earn). It uses AI, so it’s like having a personal finance advisor on-demand. Instead of combing through blogs or reviews, you get personalized suggestions.

- Keeps it all organized: Rather than you maintaining a spreadsheet of which card to use for what (which, let’s face it, most of us won’t do), Kudos is the organizational brain. You can just rely on its prompts and focus your brainpower on other things. It’s like putting your credit card strategy on autopilot.

For a new credit card user, this is like training wheels that actually boost your speed. You’ll learn from it too (“Oh, I didn’t realize my card was best for this category, good to know!”). And because Kudos is free and secure, there’s really no downside. It aligns perfectly with Gen Z’s ethos of using tech to simplify finances (the same way many use budgeting apps or investment apps).

Think of Kudos as your friendly guide that makes sure you never miss out – whether it’s $5 cash back or a $50 perk. Maximizing rewards and perks can feel like a part-time job if you try to do it manually; Kudos takes on that job for you so you can enjoy the rewards without the hassle. Plus, who doesn’t like getting an extra $20 (with code GET20) just for trying it out? It’s literally paying you to be a smarter spender.

In conclusion, navigating credit cards doesn’t have to be scary or complicated for Gen Z. With the right knowledge and tools, you can build credit, earn great rewards, and stay out of trouble. Use this guide as a reference as you start your journey. Before long, you’ll not only be achieving financial “firsts” (first apartment, first car loan with a low rate thanks to your credit score), but you’ll also be flexing on how your credit card paid for your last vacation or scored you a sweet cashback that you invested for future goals. Welcome to the world of credit card rewards – you’ve got this!

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)