Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

How Much Does Disability Insurance Cost, and Is It Worth It?

July 1, 2025

If you’re considering protecting your income with insurance, a big question is: what will it cost? We insure our cars, homes, and health – but insuring our paycheck (through disability insurance) often gets overlooked. Part of the reason is people assume it’s expensive.

The truth: disability insurance does come at a cost, but it might be more affordable than you think – and the protection it provides can be priceless if you ever need it. This article breaks down how much short-term and long-term disability insurance typically cost, the factors that influence the price, and whether disability coverage is truly worth the expense.

Typical Cost of Disability Insurance (Short-Term & Long-Term)

You might expect long-term disability insurance to cost a lot more than short-term (since it can pay out much more in benefits if you become disabled). Interestingly, the premiums for short-term (STD) and long-term (LTD) disability insurance are often in the same ballpark. For an individual purchasing coverage, both tend to cost about 1% to 3% of your annual income in premiums.

Let’s put that into real numbers. Suppose you earn $60,000 a year. One percent of that is $600, three percent is $1,800. Spread over 12 months, that’s roughly $50 to $150 per month for disability insurance. If you earn $100,000, 1–3% is $1,000 to $3,000 per year (approximately $80 to $250 per month in premiums). These are rough ranges – your actual quotes may fall outside this depending on various factors, but it gives you a sense.

It’s worth noting that if you get disability insurance through your employer, you might pay less than these figures (group rates can be lower, or your employer might pay part of the premium). In some cases, employers fully cover short-term disability, and offer long-term at a discount or with company contributions. On the other hand, if you’re buying an individual policy on your own, you’ll bear the full cost.

Short-term vs Long-term cost: Generally, short-term disability isn’t much cheaper than long-term. In fact, one industry tidbit is that a short-term policy can cost nearly the same as a long-term policy for an individual. Why? Because you’re more likely to use short-term insurance (many people have a short disability at some point, like a few weeks out for surgery or maternity leave), whereas long-term disabilities are less common. Insurers price the risk accordingly.

So dollar for dollar, long-term gives more potential benefit (years of coverage) for similar cost, making it a better value. If you’re paying out-of-pocket and budgeting, that’s one reason experts often say get long-term coverage; use other means for short-term needs if necessary.

Bottom line: Expect to pay somewhere in the low single-digit percentages of your salary for a disability insurance policy. If your policy is through work or you’re younger and very healthy, costs might be on the lower end. If you have a risky occupation or buy a lot of extra coverage, it might be on the higher end of that 1–3% range.

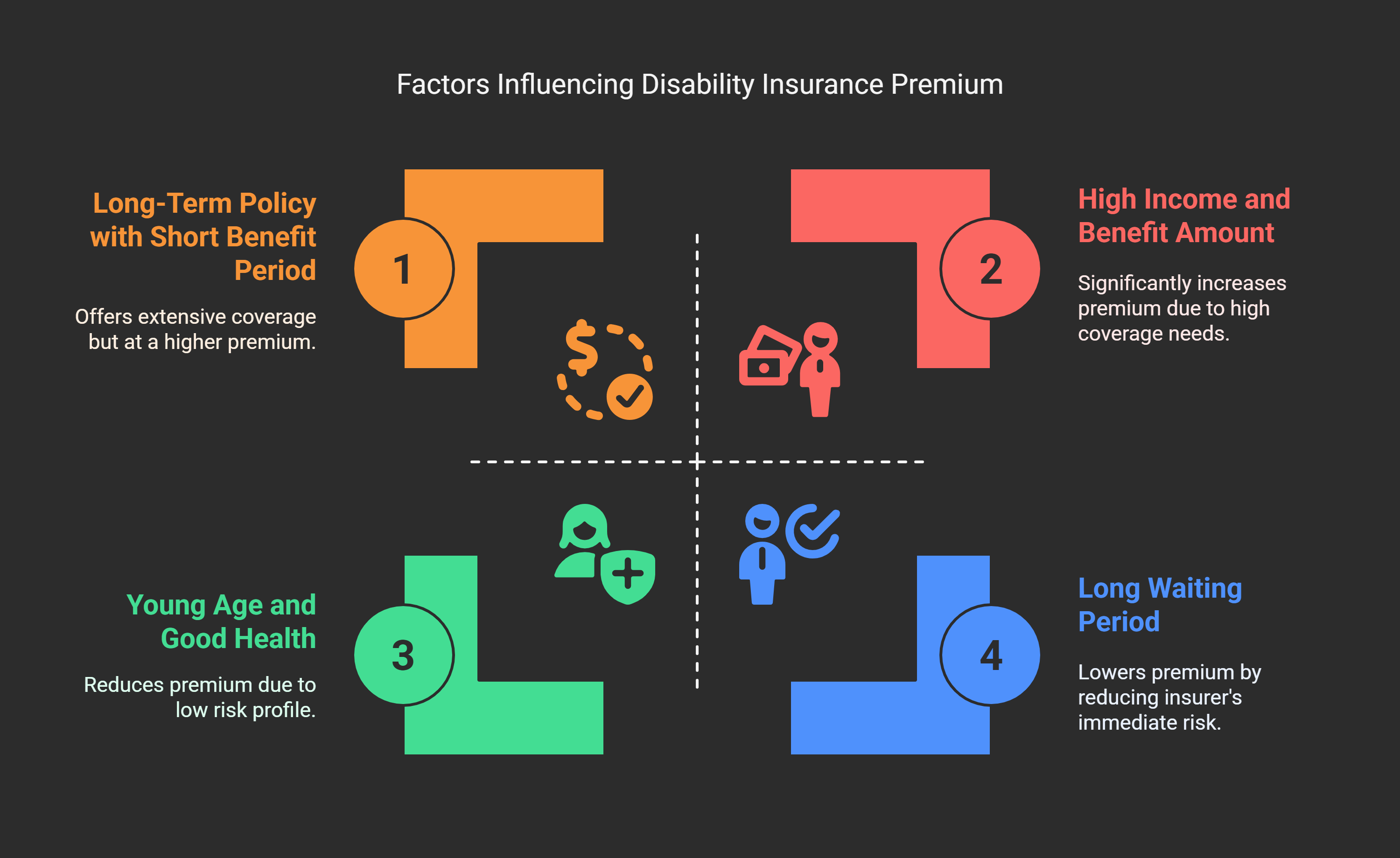

Factors That Affect Your Disability Insurance Premium

Just like other insurance, disability insurance premiums depend on several variables. Here are the key factors that will influence how much you pay:

Your Income and Benefit Amount:

The more income you need to insure, the higher the premium. A policy that would pay you $3,000 a month will cost less than one that would pay $6,000 a month, obviously. Most insurers cap the benefit at around 60-70% of your income. You don’t necessarily choose the dollar amount arbitrarily – it’s usually based on your current earnings. But if you opt for a lower replacement (say 50% instead of 60%), that could reduce cost (though most people want the max coverage they’re eligible for).

Short-Term vs Long-Term Policy:

A short-term policy (paying for, say, up to 6 months) versus a long-term policy (paying years) might have similar costs, but if you were to get only short-term or only long-term, sometimes the long-term is just slightly more. The main cost difference comes from benefit duration. Some long-term policies allow you to choose a shorter benefit period (like 5 years instead of until age 65) to save on premium – that could lower cost, but it also limits protection.

Waiting Period (Elimination Period):

is a big lever on cost. A longer waiting period (the time you have to be disabled before benefits start) will reduce your premium. For example, a policy with a 180-day elimination period will cost less than one with a 90-day period, which costs less than a 30-day wait. Why? Because if you agree to cover the first X days of disability yourself (through savings or other means), the insurer’s risk is lower.

Choosing around a 90-day elimination period is a common balance – it lowers cost versus a 30-day wait, but isn’t as hard to cover as a 180-day wait. Short-term policies usually have short waits by nature (like 7 or 14 days), whereas long-term policies often have 90 days. If you have a good emergency fund, you might opt for even 120 or 180 days waiting on the long-term to save money on premiums.

Your Age and Health:

The younger and healthier you are when you buy the policy, the cheaper it will generally be. Premiums are lower at age 25 than at 45. Health conditions can affect insurability – insurers might charge more or exclude certain pre-existing conditions. Buying earlier in life locks in coverage before health issues develop. Many policies are level-premium (your rate stays the same each year once you buy). So getting it young can secure a low rate for life. Smokers, unfortunately, pay more (tobacco use is a factor for higher premiums, as with life insurance).

Occupation and Risk Factors:

What you do for a living matters. Insurers group occupations into classes by risk. A desk job (low risk of injury) will get a better rate than a construction worker or a surgeon (surgeons have high incomes but also a higher chance of hand injuries, etc., that could cause disability). Some hobbies (like skydiving, for instance) might also raise eyebrows. But mainly, job risk and income type factor in. Mental health coverage can sometimes be limited in policies (e.g. some policies only pay up to 2 years for mental health-related disabilities unless you pay extra), which indirectly affects cost too.

Policy Riders and Add-Ons:

You can customize with riders – each typically adds a bit to the premium. Common riders include:

- Cost of Living Adjustment (COLA): increases your benefit annually if you’re on claim, to keep up with inflation. Helpful for a long-lasting disability, but it will cost extra.

- Guaranteed Insurability: lets you increase coverage later without medical exams as your income rises. This costs extra now for that flexibility later.

- Own-Occupation Definition: as mentioned, if you choose a true own-occupation definition for long-term, it might raise your cost some, but gives better coverage.

- Residual or Partial Disability Rider: allows partial benefits if you can work part-time or at a reduced capacity. Good for scenarios where you’re not totally unable to work, but maybe your income drops due to a disability.

- Additional riders: There are others (like a rider that continues contributions to your retirement plan, or a catastrophic disability benefit, etc.). Each rider might add a small percentage to the premium.

Length of Benefit Period:

For long-term policies, choosing a shorter maximum benefit period (like benefits last 5 years instead of to age 65) will lower the premium. However, this also greatly reduces the protection – a permanent disability in your 30s could easily last more than 5 years. Many people opt for the longest benefit period (to retirement age) despite the higher premium, because that’s the whole point of “long-term” coverage.

Is Disability Insurance Worth the Cost?

Paying an extra bill every month for something you might never need can give anyone pause. So, is disability insurance really worth it? Consider these points:

Your income is your biggest financial asset.

Without your salary, how long could you comfortably pay for rent/mortgage, groceries, and other expenses? For most, it’s not very long. Disability insurance essentially insures your future paychecks. Over your career, you might earn millions of dollars – that is worth protecting. One analysis by the Social Security Administration shows that a 35-year-old worker with a $50k salary who suffers a permanent disability could lose up to $1.5 million in future earnings by age 65. Spending a small percentage of your income on insurance to safeguard that earning potential is a wise trade-off for many.

Disability is more common than we think:

As mentioned, roughly 25% of young workers will experience a disabling injury or illness lasting at least 90 days before retirement. That’s a pretty high likelihood. We often insure against events like car accidents or house fires which are statistically less common. Losing your income for an extended period is a real risk.

Consequences of not having it are severe:

If you become unable to work for, say, a year or two, the financial fallout can be huge – draining savings, racking up debt, potentially defaulting on loans or even losing assets. Bankruptcy due to medical issues and loss of income is not rare. Disability insurance prevents that worst-case scenario by providing a financial lifeline when you’re most vulnerable.

It’s not as expensive as many assume:

As we calculated, a typical cost might be around $100 a month (varies by person). Think about other expenses: many people spend more on daily coffee or streaming subscriptions in a month. For the price of a gym membership, you could protect thousands of dollars of monthly income. When weighed against what you stand to lose (your entire income), it’s relatively modest. Plus, you can often pay through payroll deduction which makes it feel easier.

Peace of mind:

There’s also the intangible value. Knowing that you have a safety net if the worst happens can relieve a lot of financial anxiety. You can focus on recovery and health without the constant fear of how you’ll keep the lights on. That peace of mind is worth something in itself.

Who might skip it:

If you’re wealthy enough that you could live off investments or passive income without working, or you’re very close to retirement with substantial savings, you might not need disability insurance. Also, if you have a very robust social support (for example, some people might rely on a spouse’s income), the urgency is lower. But for the vast majority who depend on their paycheck, it’s a crucial protection.

Consider employer coverage and gaps:

Many employers provide some disability insurance, but check how much. Some only cover 50% of salary or have short benefit durations. It might be worth getting a supplemental policy to fill gaps. Also, employer-paid long-term benefits are typically taxable when you receive them (since the premium was paid pre-tax or by employer), meaning the 50-60% replacement might shrink after taxes. An individual policy you pay for is tax-free when received, which provides true 60% of income. These nuances affect the real “worth” of what you have.

Alternatives are limited:

As mentioned, government benefits like SSDI are hard to get and not enough to live on for most. If you’re thinking “I have savings so I don’t need it,” be sure you truly have enough. Financial planners often say you’d need many years of expenses saved to self-insure long-term disability risk – far more than an emergency fund. Few people are at that level unless they’re financially independent already.

In conclusion, for most working people, disability insurance is absolutely worth the cost. It’s one of those things that seems optional until suddenly it isn’t. If you never need to use it, you’ll be glad nothing bad happened.

If you do need to use it, it could literally save you from financial ruin. As the saying goes, “hope for the best, plan for the worst.” A disability policy is planning for the worst, and it can make all the difference if life throws you a curveball.

Tips to Save on Disability Insurance

If cost is a concern, here are a few tips to manage the expense while still getting protected:

- Get coverage through work if possible: Group plans are often cheaper and sometimes subsidized. Even if you have to pay the premium, group rates can be 10-20% lower than individual.

- Opt for a longer elimination period: If you have a solid emergency fund, choosing a 90 or 180-day waiting period for long-term disability will cut premiums significantly compared to a 30-day wait.

- Choose core coverage first: You don’t necessarily need every rider. For instance, you might skip COLA if you’re near retirement (less worry about decades of inflation), or skip certain riders to trim cost. Make sure you have the basics – adequate benefit amount and benefit period – then add riders only if budget allows.

- Buy young and lock it in: The younger you are when you start, the cheaper it is and you can often keep that rate. Some policies even offer discounts for females if bought at certain ages (since historically claims differ, etc.), or discounts if you’re in a low-risk profession. Starting early avoids future health issues making it pricier or uninsurable.

- Consider policy through professional associations: If you’re self-employed or your job doesn’t offer coverage, check organizations you belong to. They might have a group plan you can join.

- Review your coverage periodically: If you get a policy at 25 when making $40k, and now you’re 35 making $100k, update your coverage if needed. Many policies have options to increase coverage (especially if you added a future increase rider).

The Value Proposition

Ultimately, when deciding if disability insurance is “worth it,” think of it this way: For a few dollars a day, you safeguard your largest financial resource – your ability to earn an income. If an illness or injury knocks you down, your policy steps in and says, “Don’t worry, we’ve got income coming in for you.” That can be the difference between a temporary setback and a permanent financial disaster.

Kudos makes comparing auto insurance rates simple, helping you quickly find the best rate for your needs. The service is completely free and easy to use. Just as you'd shop around for disability insurance to protect your income, it's wise to compare your auto insurance options.

With Kudos, you can make sure you're getting the right coverage without overpaying – all at no cost to you.

Frequently Asked Questions (FAQs)

How much does long-term disability insurance cost on average?

On average, a long-term disability (LTD) policy costs about 1-3% of your annual income in premiums. For many people, that might be in the range of $50 to $150 per month, depending on income and coverage. For example, a person earning $80,000 might pay roughly $70 to $200 monthly for a robust long-term policy. Costs can vary based on age, occupation, health, the waiting period, and benefit amount.

Why is short-term disability insurance often not “worth it” to buy privately?

It’s not that short-term disability isn’t valuable – it certainly is if you need it – but buying a private short-term policy can be expensive relative to the benefit you’d receive. Private short-term policies can cost as much as long-term ones, yet only pay out for a few months if you claim. Many financial planners suggest using an emergency fund to cover short-term needs (a few months of no income), and investing your insurance dollars in a long-term policy which covers the bigger risk of an extended disability.

Are disability insurance premiums tax-deductible?

For individual (personal) disability insurance policies, premiums are not tax-deductible in most cases. However, the upside is that if you ever collect benefits, those benefits will be tax-free (because you paid the premiums with after-tax money). For employer-provided plans: if your employer pays the premium (or you pay with pretax payroll deductions), you cannot deduct the premium and any benefits you receive would be subject to income tax.

What if I can’t afford the recommended amount of disability coverage?

Some coverage is better than none. If you can’t afford to cover, say, 60% of your income, consider getting a smaller benefit or opting for a longer waiting period to reduce premiums. For example, maybe you insure 40% of your income or choose a 180-day elimination period – this will lower cost. You could also start with just a long-term policy (skip short-term) to focus your budget on covering a catastrophic scenario.

Does disability insurance cover all illnesses or injuries? Are there exclusions?

Disability insurance covers you for injuries and illnesses that render you unable to work, but policies can have exclusions or limitations. Common exclusions might include disabilities due to pre-existing conditions (usually for a period of time after the policy starts, e.g. no coverage for a condition you already have for the first 12 months). Some policies limit or exclude claims related to mental health or substance abuse (for example, they might only pay benefits for up to 24 months for mental health disabilities, unless you pay extra for a rider).

Injuries sustained during criminal activities or perhaps dangerous hobbies might be excluded. Pregnancy is covered under short-term plans but usually not under long-term unless complications extend into long-term disability. Always read the policy details. The good news is most common causes of disability (like musculoskeletal problems, back injuries, cancer, heart disease, etc.) are covered.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)