Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

How to Budget for Recurring Subscription Expenses in 2026

July 1, 2025

The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

Recurring bills used to mean the electric, phone, and maybe a cable bill. Now, from Netflix to meal kits to monthly beauty boxes, our budgets face a new challenge: dozens of subscription payments. This article shows you how to seamlessly integrate subscriptions into your budget, so you can enjoy your services without overspending. Let’s make a 2025 budget that tames those recurring charges!

The Rise of Subscriptions in Our Budgets

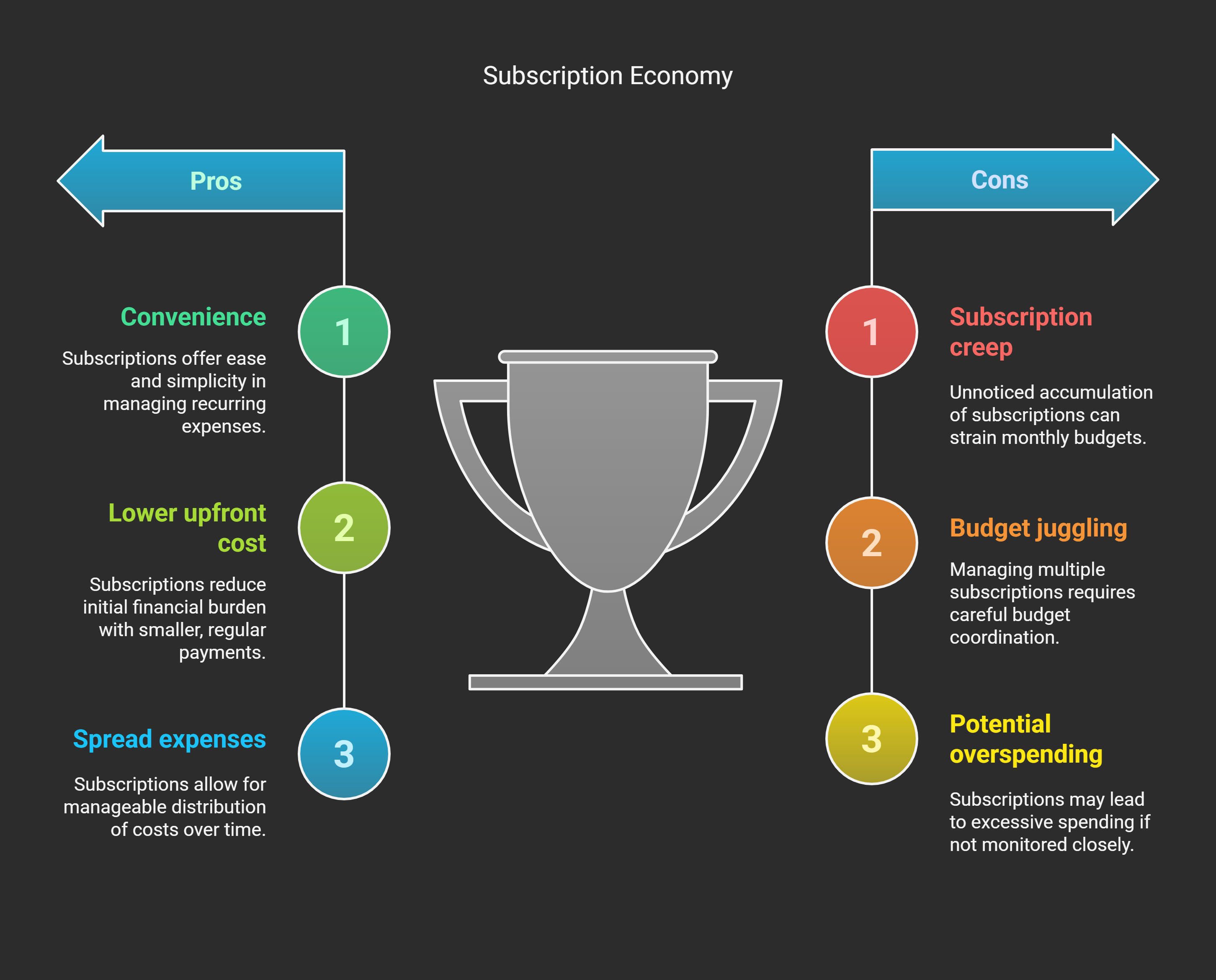

In 2025, subscriptions aren’t just an occasional expense – they’re a way of life. Media, software, groceries, gyms, even car maintenance plans now use subscription models. The subscription economy has exploded, with consumer spending on subscriptions climbing steadily each year. In fact, surveys show the average American has around 4 to 5 paid subscriptions and spends roughly $900-$1,000 per year on them. That’s a significant chunk of annual expenses!

Why the surge? Subscriptions offer convenience and often a lower upfront cost. Instead of a large one-time payment, we pay smaller amounts over time. This can help spread out expenses – but it also means we must juggle many mini-bills in our monthly budget. It’s easy to lose track, which can lead to “subscription creep” (those sneaky accumulations we discussed above).

The good news is that with some planning, you can accommodate your favorite subscriptions into a responsible budget. The key is to be deliberate: know what you’re subscribed to, decide how much you want to spend on subscriptions, and adjust as needed. Treat your “Subscriptions” like any other important budget category.

Step 1: List All Your Recurring Subscriptions and Bills

Start by making a comprehensive list of every recurring expense you have. This includes:

- Digital subscriptions: Streaming services (Netflix, Hulu, etc.), music apps, cloud storage (Dropbox, iCloud), software (Adobe Creative Cloud, Office 365), news or learning apps, gaming subscriptions, etc.

- Memberships: Gym membership, yoga class package, monthly massage club, etc.

- Subscription boxes: Meal kits (HelloFresh), beauty boxes, pet treat boxes – any monthly shipment programs.

- Annual subscriptions: Maybe Amazon Prime (annual option), Costco membership, AAA, etc. (They might bill once a year, but you should account for them monthly.)

- Recurring bills (fixed): Don’t forget “classic” recurring bills like internet, phone, insurance, utility averages – these are also subscriptions in a sense (though essential). It’s good to list them here for a full picture, even if you categorize them separately in your budget later.

Write all of these down with their monthly cost. For annual ones, convert to a monthly equivalent (e.g., a $120/year service is $10/month in your budget plan). If some vary, you can use an average or the last amount billed.

This master list is similar to the “audit” step for fighting subscription creep, but here our goal is budgeting. Once you see everything in one place, you might be surprised how many line items your money is going to each month.

Step 2: Categorize: Needs vs. Wants

Next, categorize each subscription as a “Need” or a “Want.” This is a classic budgeting principle, often drawn from the 50/30/20 rule (where ~50% of your income goes to needs, ~30% to wants, ~20% to savings/debt).

Needs:

Essential recurring expenses you must pay to maintain your life or work. This typically includes utilities, phone, internet (especially if needed for work or school), insurance, and maybe one car-related subscription if it’s necessary. A new category of “need” might be cloud storage if you rely on it professionally, or a key software for your job (e.g., an Adobe subscription for a graphic designer).

Wants:

Discretionary subscriptions that improve your lifestyle but aren’t strictly necessary. Most entertainment subscriptions (video, music, gaming), subscription boxes, premium app memberships, and gym or clubs (unless prescribed for health) fall here. For example, Netflix = want, Spotify = want, meal kit = could be need or want depending on if it replaces groceries or is just convenience.

Be honest with yourself here. It’s not to say you must cut all “wants” – not at all. It’s to identify which ones could be trimmed if money gets tight, and which ones should absolutely be prioritized. You might also find some “wants” that have become very important to you (e.g., a fitness app aiding your health). You can flag those as high-priority wants.

Step 3: Set a Subscriptions Budget (Cap Your Total Spend)

Now decide how much you’re comfortable spending on subscriptions overall each month. This is somewhat personal, but here are two approaches:

Percentage approach:

If following a budgeting framework like 50/30/20, allocate part of your “wants” 30% bucket to subscriptions. For example, if your take-home pay is $3,000, 30% is $900 for all wants. Maybe you decide no more than half of that ($450) should go to subscriptions, leaving the rest for other wants (like dining out, shopping, etc.).

Zero-based approach:

Assign each subscription a place in your budget categories and ensure your income minus expenses equals zero. For instance, $100 for streaming/TV, $30 for music, $60 for apps/software, $50 for hobby boxes, etc., plus your needs like $70 for internet, $10 for Prime, etc. Add them up and see if it’s affordable. Adjust until the total fits comfortably in your income minus other obligations.

Whichever method, it helps to put a hard cap on discretionary subscriptions. E.g., “I will spend no more than $200/month on non-essential subscriptions.” This forces choices. If you’re at $220 and a new tempting service comes along, you know you need to cancel or downgrade something first (or decide the new one isn’t worth busting the budget). This discipline prevents overshooting your means.

Remember to factor in yearly subscriptions: If you have a $120 annual membership, set aside $10 each month for it. Good budgeting apps or techniques treat annual bills as monthly “sinking funds” – you reserve a bit each month so when the bill arrives, it’s already budgeted.

Step 4: Optimize and Adjust Your Subscriptions

With a cap in mind, it’s time to optimize. This goes hand-in-hand with fighting subscription creep, but from a budgeting lens, consider these adjustments:

Cut or Pause

Cut or Pause low-value subscriptions (especially if your list exceeds your budget cap). Look back at your “wants” list – is there anything you wouldn’t miss much? Perhaps you rotate services: cancel a streaming service you’re bored with for now, and add a different one next month in its place without increasing total spend. If you’re over budget, start cuts from the bottom of your priority list and work up until you’re within limit.

Downgrade Plans

Many services have tiers. Maybe you’re on a premium plan with bells and whistles you don’t use. For instance, if you pay $15 for ad-free Hulu but don’t mind an ad or two, dropping to the $7 plan could save you $8/month. Or switching from family plan to individual on a service if you’re not actually sharing it. Ensure you’re not overpaying for unused benefits.

Bundle Where Possible

Sometimes bundling services can save money. For example, Disney+, Hulu, and ESPN+ bundle is cheaper than paying each separately. Or if you have multiple services from one provider (like Apple One bundles music, TV, cloud, etc.), it might offer a discount. Just be careful bundling doesn’t make you keep things you wouldn’t otherwise.

Annual Pay if It Saves

If (and only if) you have the savings to handle it, consider paying annually for subscriptions that offer a good discount for upfront payment. Many services give ~10-20% off for annual billing. If you know you’ll use it for the full year, you could save in the long run. But make sure to budget the lump sum – perhaps set aside money each month so when the annual renewal hits, it’s not a surprise. (In your budget, you would still treat it as a monthly cost internally).

Keep an Eye on Price Changes

Prices for subscriptions can change, often via a small email you might miss. Make it a habit to read any “We’re updating our Terms/pricing” emails. If a price increases significantly, re-evaluate that service immediately. A jump from $10 to $15 a month means $60 more per year out of your budget. You might find it no longer worth the new price.

Use Prepaid Cards for Certain Subs

Here’s a clever budgeting hack: for some discretionary subscriptions, you can use a prepaid debit card or gift card. For instance, load a prepaid card with your set monthly subscription budget amount. Use that card for all your fun subscriptions. If it runs out, that’s it – you can’t accidentally overspend because the card will decline further charges. This is advanced and not necessary for everyone, but it’s a tool that enforces limits.

After optimizing, your subscription lineup should align with your budget. You’ve allocated a purpose to each dollar, and ideally trimmed any truly wasteful spending.

Step 5: Monitor Monthly and Plan for Annual Charges

Incorporate your subscriptions into your normal budget tracking. If you budget by category, have a “Subscriptions” category (you can break it into subcategories like Entertainment, Lifestyle, Utilities, etc., or keep it consolidated). Each month, check the actual charges against what you planned.

- Set alerts for upcoming big charges. For example, if you pay car insurance or a professional membership annually, set a reminder a month before so you remember it’s coming (and can shop around if needed).

- If you use a budgeting app like Mint, YNAB, or PocketGuard, make sure all your subscriptions are tagged or accounted for. Some apps will even alert you to recurring payments and their total.

- Adjust regularly: Budgets are not set in stone. You might decide after a while that you’re not using one service and you’d rather allocate those funds elsewhere. Or maybe you get a raise and decide you can afford an extra fun subscription – great, just adjust your budget to include it. The key is it’s a conscious choice, not an accident.

A smart move is to treat subscription spending somewhat like a fixed expense but review it like a variable expense. In other words, plan for it, but don’t set and forget – revisit if your financial situation or priorities change.

Using Kudos to Boost Your Budget’s Bottom Line

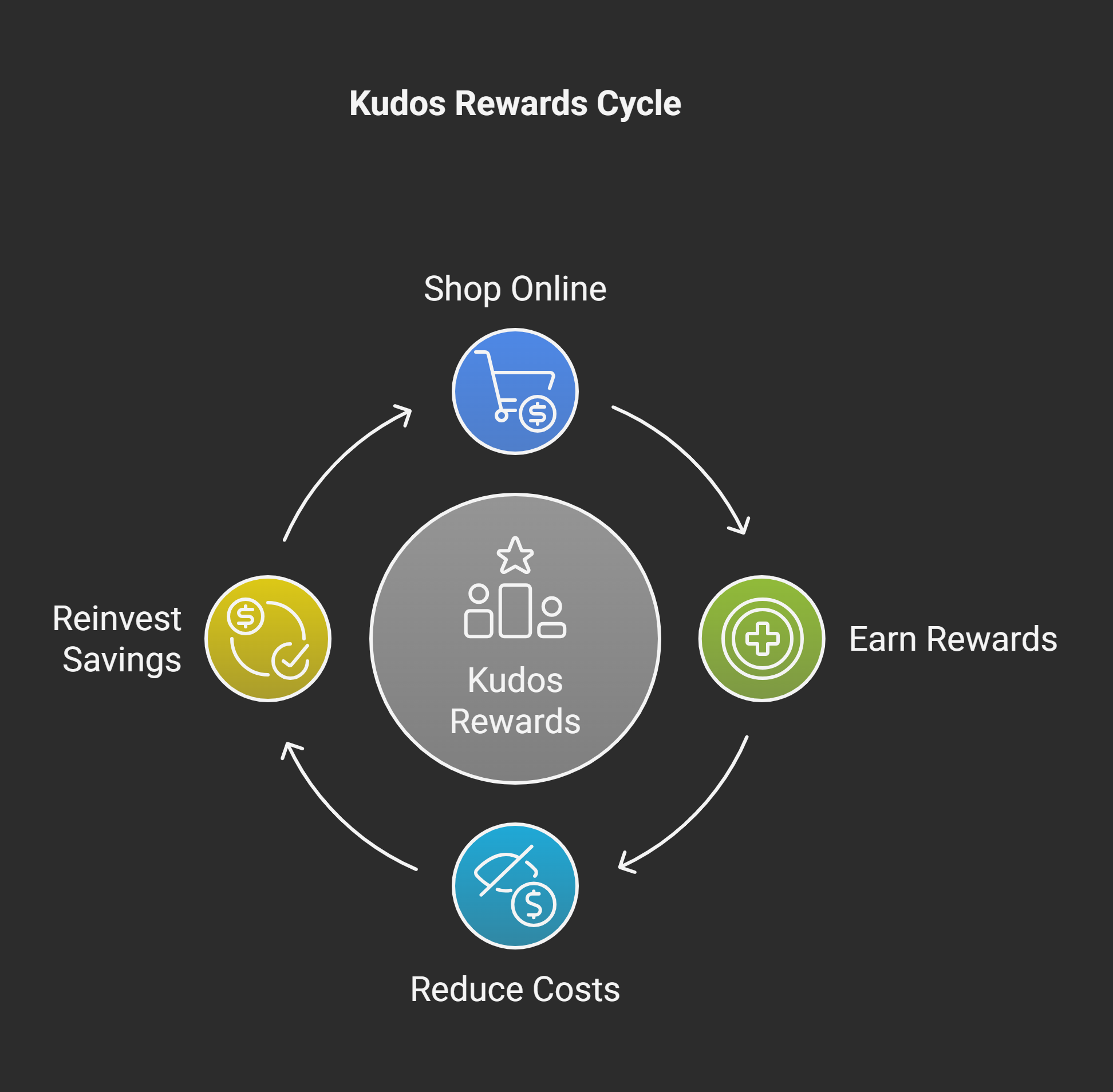

Sticking to a subscription budget is about making your money work efficiently – and that’s exactly what Kudos helps you do with all your other spending. Kudos is a free tool that maximizes your rewards when you shop online or pay for services. Think of it as extra money flowing back into your budget.

For example, if you’ve budgeted $50 for a particular subscription or online purchase, using Kudos could earn you cashback or points worth a few dollars – effectively lowering the net cost. Kudos gives you 100% of the commission back on purchases (unlike other shopping portals that keep a cut), meaning you can earn 2–3× higher rewards on average.

Over a year, these extra rewards can add up and even cover one of your subscription bills! And it’s totally free. If you’re new, use code GET20 to snag $20 after your first Kudos purchase – that could pay for two months of a music streaming service right there. By integrating Kudos into your buying routine, you ensure that even while paying for necessary subscriptions, you’re getting a little “thank you” cash back each time, which you can put right back into your budget or savings.

FAQs – Subscription Budgeting

Is there a guideline for how much of my income should go to subscriptions?

There’s no one-size-fits-all rule, but many subscriptions are “wants” and fall under discretionary spending. A popular guideline, the 50/30/20 rule, suggests about 30% of take-home pay for “wants,” which includes subscriptions, dining out, hobbies, etc. You might aim to keep subscriptions at 10-15% of your take-home pay at most, especially if you have other significant wants.

How do I handle annual subscriptions in my monthly budget?

Treat annual expenses as if they were monthly by setting aside money each month. This is often called a sinking fund. For instance, if Disney+ is $80 per year, allocate ~$6.67 per month in your budget for it. You can put that cash in a savings account or just mentally earmark it. When the yearly bill hits, you’ll have the funds ready. Some budgeting apps automate this process, showing you a prorated monthly “expense” for annual bills so you’re not caught off guard.

Should I use a separate account or card just for subscriptions?

It’s not necessary, but it can help some people. Using one credit card for all subscriptions can simplify tracking (one statement to review). Just make sure that card has a limit high enough to handle fluctuations and always pay it off monthly to avoid interest. Some even open a separate bank account for bills & subscriptions, depositing a set amount there to cover all auto-pays. This way your spending money is separate from bill money. It adds a bit of complexity but also safeguards that your bill funds won’t be accidentally spent elsewhere.

What if an emergency happens – can I pause subscriptions to save money?

Absolutely. Many subscriptions (especially streaming or memberships) allow you to pause or cancel and rejoin later. If you face a job loss or an unexpected large expense, subscriptions are often the first place to trim the budget. Since they’re typically monthly, you can cut them quickly and reinstate when your finances recover. For example, pause your Netflix for a couple of months – your profile stays intact for a while. Just don’t forget to resume payments when you’re ready to use it again.

Are “subscribe and save” deals (like Amazon Subscribe & Save) good for my budget?

They can be, if used wisely. “Subscribe and Save” on Amazon, for instance, gives up to 15% off household items if you subscribe to regular deliveries. This can save money on things you’d buy anyway (like toiletries, pet food). Just ensure the schedule matches your usage (so you’re not oversupplied) and that it truly is a product you need regularly. Treat those like any other subscription in your budget. They fall under groceries/household category, so account for them there. The discount is nice, but if you start subscribing to too many items due to convenience, it could inflate your budget – so review these periodically too.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)