Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Is Dental Insurance Worth It? An Honest Look at Costs, Benefits & Alternatives (2026)

July 1, 2025

Dental Insurance's Worth In 2025

Dental insurance promises to save us money on dentist bills – but does it really? If you’ve ever paid premiums all year and only used two free cleanings, you might wonder, “Is dental insurance even worth it?” The answer isn’t one-size-fits-all.

In this friendly guide, we’ll examine the pros and cons of dental insurance in 2025, including how much it costs, what it typically covers (and doesn’t), and scenarios where you might actually save more by not having insurance.

We’ll also explore alternatives like dental discount plans, paying cash, or using tax-advantaged accounts. By the end, you’ll have a clear sense of whether dental insurance is a smart investment for you – or if your money is better kept in your own pocket for that rainy (toothache) day.

What Does Dental Insurance Really Cover (and What’s the Catch)?

Dental insurance is different from health insurance. Key things to know:

- Preventive care is covered 100% in most plans (cleanings, exams, X-rays).

- Basic procedures like fillings or simple extractions are often covered around 70–80%. You’ll pay the rest.

- Major work is usually covered at 50% or sometimes less, after a waiting period of up to 6-12 months on new policies.

- Orthodontics and cosmetic dentistry are typically not covered by standard adult plans.

- Crucially, dental plans have annual maximums – often $1,000 to $1,500. That’s the most the insurer will pay in a year. If you have a $4,000 dental implant, your insurance might pay $1,000 and then it’s “maxed out,” leaving you with the rest.

In short, dental insurance is best at covering routine, preventive care and some common fixes. It is not designed to cover catastrophic dental costs in full. If you have unusually high dental needs in a year, you may quickly hit the cap.

When Dental Insurance is Worth It

- You get it super cheap (or free) through work: Many employers offer dental insurance and often subsidize part of the premium. If your payroll deduction is, say, $10 a month for a decent plan, it’s almost a no-brainer.

- You or your kids need significant dental work: Planning braces for your teenager? Got a couple of crowns on the horizon? Insurance can greatly reduce those costs.

- You like regular maintenance and checkups: If you’re disciplined about visiting the dentist twice a year and maybe an occasional filling, insurance keeps your costs predictable. You might pay $30/month in premiums, and get about $400 worth of cleanings and X-rays covered, plus have coverage if a surprise cavity comes up.

- Your dentist’s prices are high: This sounds odd, but if you live in a high-cost area where a cleaning is $200 and a filling $300, having insurance negotiated rates and coverage can save a lot. Dental insurers negotiate lower fees with in-network dentists.

When Dental Insurance May NOT Be Worth It

- You have very healthy teeth and rarely need work: If you’re one of the lucky ones who only goes for cleanings and hasn’t had a cavity in years, you might be paying more in premiums than you get back.

- The plan’s network or coverage is poor: Some cheap plans have limited dentist networks. If you end up going out-of-network, the insurance might reimburse very little, so you’re effectively paying most costs yourself.

- You’re self-employed with high premiums: Individual dental plans can cost $40+/month for decent coverage. If you only use, say, $300 of services a year, you paid more than you got. Over a few years, if an emergency happens you might catch up on value, but it’s not guaranteed.

- Waiting periods and exclusions don’t align with your needs: If you just signed up but then find out you need a root canal next month, your plan might not help due to a waiting period. If you suspect you need major work soon, a no-waiting-period plan or alternative financing might be better than a standard insurance plan that won’t kick in when you need it.

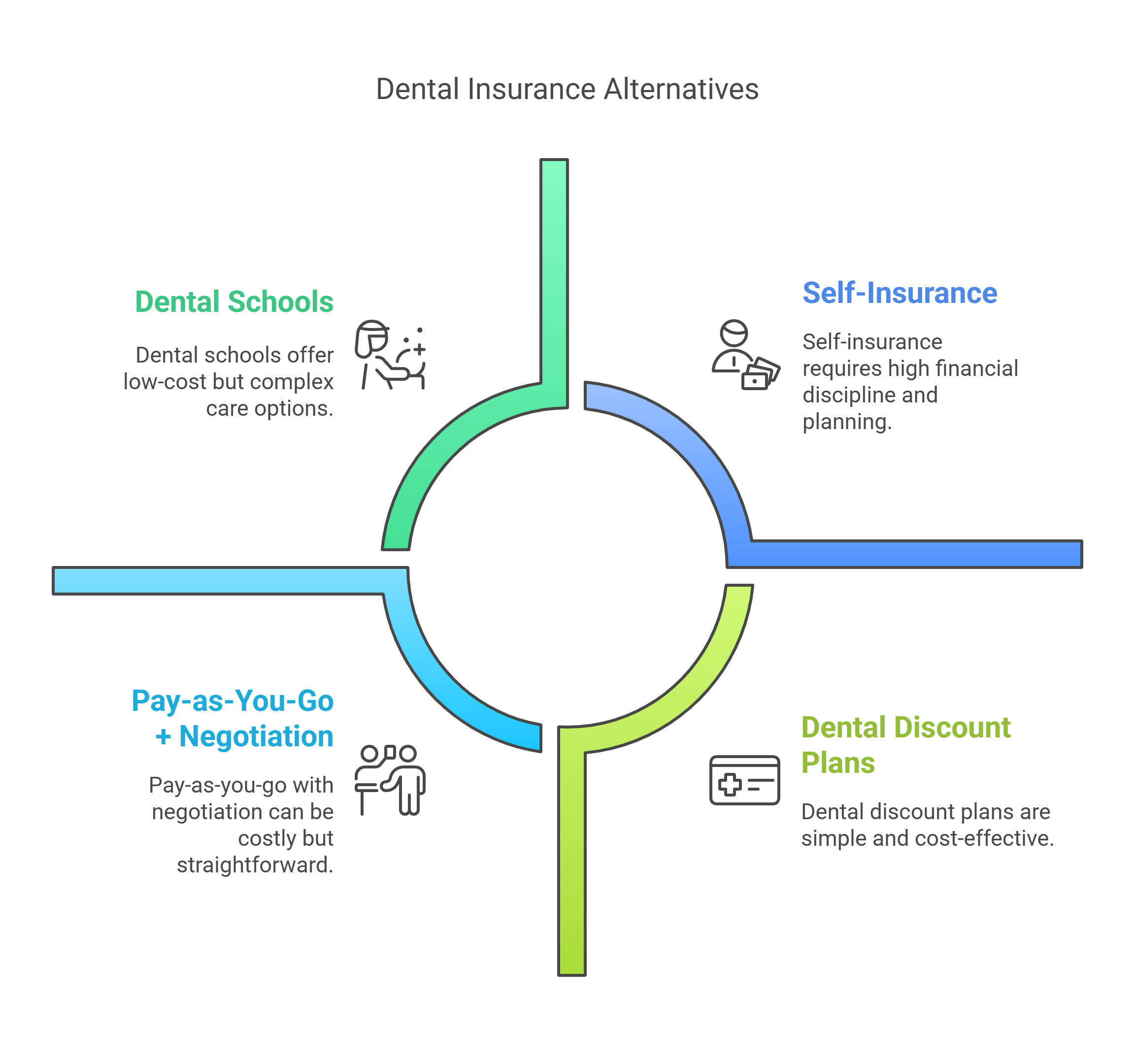

Alternatives to Traditional Dental Insurance

If you decide dental insurance isn’t for you (or you just want to explore other options), consider these alternatives:

- Dental Discount Plans: As mentioned earlier, these are membership programs that give you reduced rates at the dentist. There’s no coverage per se; you just pay a lower fee. This can save 20-50% on procedures.

- Self-Insurance (Saving Money Yourself): One strategy is to take the money you’d spend on premiums and set it aside in a dedicated savings account (or an HSA if you have a high-deductible health plan). This works best if you’re disciplined and have decent financial cushion for a worst-case scenario (like needing multiple root canals – rare, but could be costly).

- Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): If your employer offers an FSA, you can put pre-tax dollars aside for dental care. This effectively gives you a discount equal to your tax bracket on any dental work. HSAs (if you have one) similarly can be used for dental expenses tax-free.

- Pay-as-You-Go + Negotiation: Many dentists will work with patients who don’t have insurance. You can ask for a cash payment discount (since it saves them claim filing). Some dentists offer in-house membership plans: e.g., pay $300/year to the office and get two cleanings, exams, and X-rays included, plus 20% off any other work.

- Dental Schools: If you live near a dental school, they often offer low-cost care for those willing to have a supervised student or resident do the work. This isn’t a long-term strategy for everyone, but for big procedures, it’s an alternative way to reduce cost if insurance isn’t covering you.

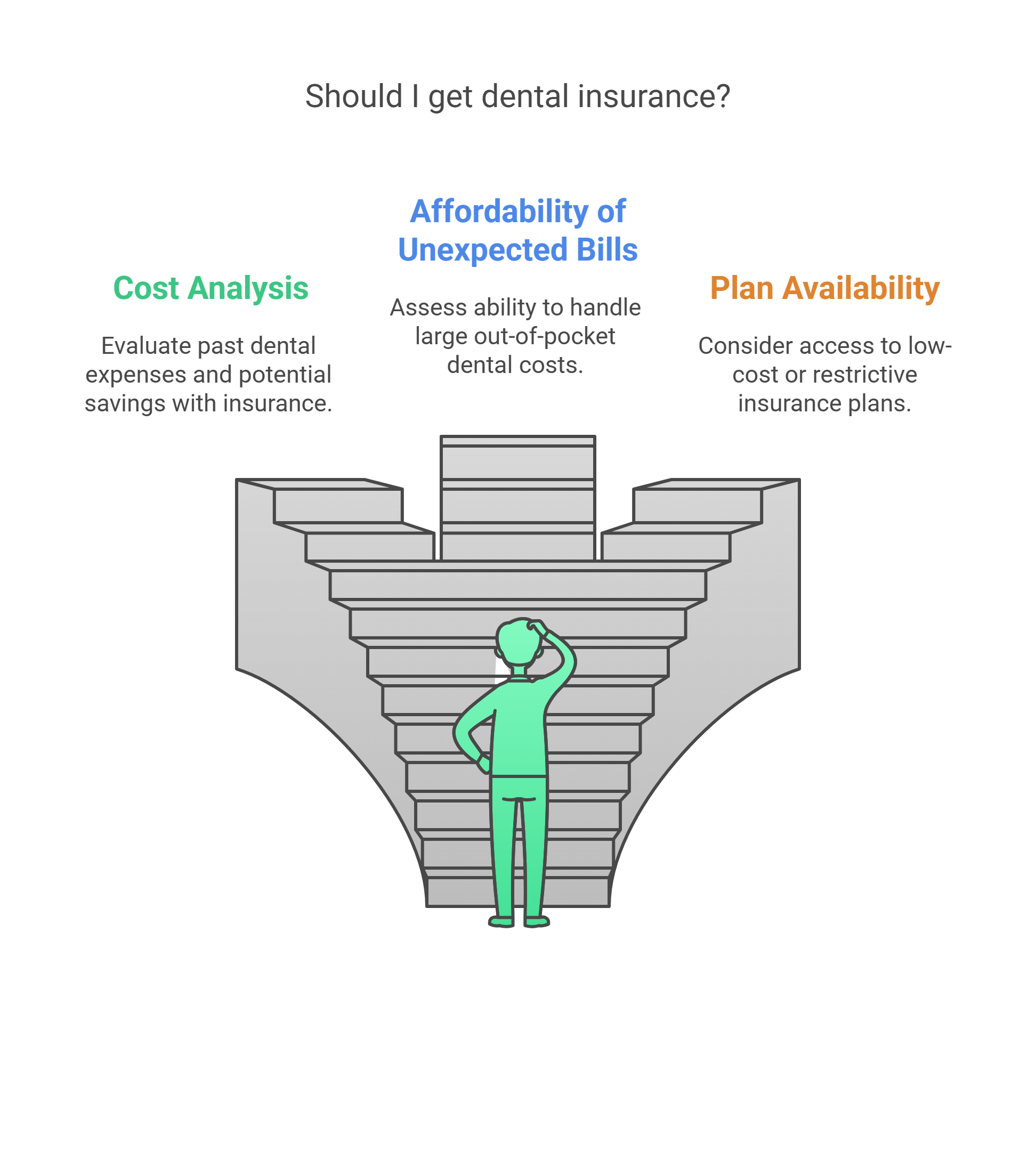

So, Is It Worth It? Making Your Decision

Ask yourself a few questions:

- How much did I spend on dental care in the past 2-3 years, and how much would insurance have saved me? If you had a year with a couple of cavities and a crown, insurance probably helped. If you only had cleanings, you might have paid more for insurance than the care itself.

- Can I afford an unexpected $1000+ dental bill out-of-pocket? If not, insurance is a way to mitigate that risk (somewhat – keeping in mind the cap).

- Do I have access to a low-cost plan (through work or elsewhere)? If yes, it tilts towards “get the insurance.” If the only plans available to you are pricey and restrictive, you might lean “skip it and save money on your own.”

For many people, a middle ground works: get a basic inexpensive insurance for the routine stuff and be prepared to pay some out-of-pocket for bigger things. Think of dental insurance less as catastrophic coverage and more as a prepaid maintenance plan with some break on bigger repairs.

If you decide it’s not worth it, that’s okay too. Just have a plan – maybe set aside a bit each month as your “dental fund” and use a discount card. The key is not to ignore dental health; untreated dental problems can become far more costly (and harmful to your health) down the line.

Put Your Cards to Work with Kudos

Whether you carry dental insurance or not, managing dental expenses smartly is important. Kudos can help you optimize how you pay for dental care. Suppose you choose to self-insure and have saved up $1000 for a procedure – paying with the right credit card could fetch you $20-$30 back in rewards or even 0% interest to spread payments out.

If you do have insurance, you’re likely still paying some portion; use Kudos to find a card that maybe offers extra points on healthcare expenses or use a card’s sign-up bonus to offset that big dental bill. Kudos automatically suggests the best card at checkout.

That means if your dentist or insurer’s website takes credit cards, Kudos ensures you’re getting the maximum reward or savings for it. Over time, those kickbacks add up – effectively making your dental care dollars go further. It’s like an extra insurance policy…for your wallet’s health!

FAQs: Dental Insurance Value

Do most people really use the full value of their dental insurance?

Not always. In fact, a significant number of dental insurance policyholders do not use more in services than they pay in premiums each year. For many, it’s an even trade – the insurance covers their cleanings and maybe one small filling, roughly equal to what their yearly premium cost. Only about 20-30% of people hit their annual maximum in a given year.

What is the average cost of dental insurance in 2025?

The average cost for an individual dental insurance plan in 2025 is around $30 to $45 per month for a plan with decent coverage. Family plans average about $50 to $90 per month, depending on family size and coverage level. There are cheaper plans that cover very basic care, and more expensive onesthat have higher annual maximums or special features like orthodontic coverage. W

If I don’t have dental insurance, how can I save on dental expenses?

There are a few savvy moves if you’re going without insurance: (1) Dental discount plans – as discussed, these can save a significant percentage off every visit for a relatively small annual fee. (2) Negotiate or shop around – dentists sometimes offer cash-paying patients a lower rate or a payment plan. (3) Preventive care – maintain good oral hygiene and get checkups (you can pay for cleanings out-of-pocket; it’s cheaper to catch a small cavity than fix a big one later). (4) Clinics and dental schools – community health clinics offer sliding scale fees, and dental schools provide supervised care at lower costs.

Is dental insurance worth it for seniors on Medicare?

Medicare (Original Medicare Parts A and B) generally does NOT cover routine dental care. Many seniors therefore consider either a Medicare Advantage plan that includes dental benefits or a separate dental insurance policy. For seniors, it can be worth it if they have ongoing dental needs (for example, periodontal maintenance, dentures, etc.). Some Medicare Advantage plans include dental at no extra cost – those are usually worth taking advantage of, though they might have limits. If a senior has minimal dental issues and is on a tight budget, they might skip insurance and pay out-of-pocket for occasional cleanings.

Can I cancel dental insurance any time if I feel it’s not worth it?

If you bought an individual dental plan, you can usually cancel at the end of your coverage period. Some plans let you cancel mid-year, but you’d want to check if there’s an obligatory initial term. Employer-provided dental usually is locked in for the benefit year unless you have a qualifying life event. If you decide it’s not worth it, the best approach is often to finish out the year you paid for, and then simply not renew for the next year.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)