Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Short-Term vs Long-Term Disability Insurance: What’s the Difference?

July 1, 2025

No one plans to get hurt or fall seriously ill, but disabilities do happen – and more often than you might think. In fact, a 20-year-old worker has a 1-in-4 chance of becoming disabled before reaching retirement age. Disability insurance is designed to replace a portion of your income if you can’t work due to illness or injury.

There are two main types: short-term and long-term disability insurance. Both serve the same purpose – protecting your paycheck – but they work in different timeframes. Let’s break down how short-term and long-term disability insurance differ, how they complement each other, and how to decide which one (or both) you need for peace of mind.

What Is Short-Term Disability Insurance?

Short-term disability insurance (STD) provides income replacement for temporary disabilities. If you’re unable to work for a short period (think weeks or a few months), an STD policy kicks in to pay a portion of your salary.

Key features include:

- Benefit duration: Short-term policies typically pay benefits for 3 to 6 months, though some can extend up to about a year. For example, if you have a 6-month short-term policy and you break your leg, it would pay benefits during the months you’re out of work recovering (up until the 6-month limit).

- Waiting period (elimination period): Short-term coverage starts quickly. There’s usually only a short waiting period (often around 7 to 14 days after you become disabled) before benefits begin. This means you might use a few sick days or a couple weeks of savings, then the STD payments kick in.

- Income replacement amount: Short-term plans often replace a higher percentage of your income than long-term plans – frequently around 60% to 70% (or even up to 80%) of your gross pay. This can come close to your take-home (net) pay since taxes aren’t usually taken out of insurance benefits.

- Typical use cases: STD often covers things like recovery from surgery, short-term illnesses or injuries, and is commonly used for maternity leave (pregnancy and childbirth recovery are a major reason people use short-term disability).

- How you get it: Short-term disability is commonly offered as a benefit through employers. Many companies provide STD coverage at low or no cost to employees. It’s less common (and can be pricey) to buy an individual short-term disability policy on your own. In some states, employers are even required to provide temporary disability coverage for workers (states like California, New York, New Jersey, Rhode Island, and Hawaii have state-mandated short-term disability programs).

In summary, short-term disability insurance is a quick bridge that keeps part of your income flowing for a few months after an unexpected health issue. It’s great for those more immediate financial needs – so you can pay your rent, groceries, and bills during, say, a 3-month medical leave.

What Is Long-Term Disability Insurance?

Long-term disability insurance (LTD) is the safety net for more serious or prolonged disabilities. If you have an illness or injury that prevents you from working for many months or even years, an LTD policy will pay out benefits after the initial waiting period.

Key features of long-term disability include:

- Benefit duration: Long-term policies have benefit periods measured in years – or even decades. A typical long-term plan might pay benefits for 2, 5, or 10 years, or up to a certain age (often until age 65 or your retirement age) if the disability continues. For instance, a policy might continue paying you a portion of your salary until age 67 if you remain unable to work due to a qualifying disability.

- Waiting period: Long-term coverage usually begins after short-term ends. There is a longer elimination period (waiting time) before LTD benefits start, often 90 days is recommended. Some policies let you choose an elimination period anywhere from 30 days up to 180 days or more.

- Income replacement amount: Long-term disability typically replaces around 50% to 60% of your gross income. That might sound like less than short-term, but remember – if you’re not working, you won’t be paying income taxes on this money if you paid your premiums with after-tax dollars.

- Typical use cases: LTD is meant for serious conditions – think injuries that require long rehabilitation, chronic illnesses, or life-altering health events. For example, long-term disability insurance would be crucial if you develop a serious condition like cancer, have a major back injury, or any health issue that could keep you out of work for several months or years. It essentially protects your future earnings when you face a long road to recovery.

- How you get it: Many people get long-term disability insurance through their employer’s benefits package (often larger companies offer an LTD plan). You can also buy an individual long-term disability policy from an insurance provider or broker. Individual policies are often customizable (you choose the benefit amount, duration, waiting period, etc.) and are portable if you change jobs.

In short, long-term disability insurance is the long haul protection – it picks up where short-term leaves off, ensuring you still have some income if you’re out of work for an extended period or even permanently unable to return.

Kudos simplifies comparing auto insurance rates, quickly finding the best rate tailored for you. It’s easy and completely free. Just as you ensure your income with disability coverage, make sure you’re getting the best deal on other insurance, like auto coverage, to keep your whole financial life secure.

Short-Term vs. Long-Term: Key Differences at a Glance

Both types of disability insurance are important, but they serve different purposes. Here’s a quick comparison of key differences between short-term and long-term disability insurance:

Length of Coverage (Benefit Period):

Short-term disability typically covers you for weeks up to months (generally up to 3-6 months, sometimes 12 months max). Long-term disability covers years (it can pay out for several years or until retirement age, depending on the policy). Think of STD as a sprint, LTD as a marathon.

Waiting Period Before Benefits:

Short-term policies have a short wait – benefits often start after ~7-14 days of disability. Long-term policies have a longer wait, commonly 90 days (about 3 months), but it could be 30 days or as long as 6-12 months, depending on the policy. A longer waiting period for LTD usually lowers its premium, but you’ll need other coverage or savings in the interim.

Percentage of Income Replaced:

Short-term and long-term plans both replace a portion of your income. Short-term plans might cover a bit more of your paycheck (often around 70-80% of your income for a short period) whereas long-term plans might cover about 50-60% of your income for a longer period. In practice, both aim to bring you close to your net (after-tax) income, since long-term benefits are typically not taxed if you pay the premium yourself.

Cost/Premiums:

Surprisingly, short-term and long-term disability insurance premiums are in a similar range. Each typically costs roughly 1% to 3% of your annual salary in premiums. For example, a person earning $100,000 might pay on the order of $80–$250 per month for disability coverage. Short-term coverage provides a smaller total payout (since it only covers a few months) but isn’t necessarily much cheaper than long-term.

In fact, if you’re buying your own policy, short-term can cost about the same as a long-term policy, which makes long-term a better value (more months of protection for similar cost). Many employers subsidize short-term premiums or offer them free, which can make STD effectively cheaper if available through work.

How You Obtain Coverage:

Short-term is often employer-sponsored (or provided via state programs in a few states) – meaning many people get it automatically or at group rates. Long-term can also be employer-sponsored, but if it’s not, you’d need to purchase a private policy. It’s generally recommended to have an individual long-term policy if you can, since you control it and keep it even if you change jobs, whereas employer coverage disappears if you leave the company.

Typical Use Scenario:

Use short-term for temporary disabilities (e.g. a routine surgery recovery, maternity leave, minor injury). Use long-term for serious, prolonged disabilities (e.g. major illness, catastrophic injury). Ideally, they work together: short-term covers you initially, and if your disability extends, long-term picks up thereafter. Having both means comprehensive coverage for both the early weeks and the long haul.

In summary, the big picture is: short-term = quick help, short duration; long-term = slower to kick in, but lasts much longer. Both replace part of your income so you can keep paying bills when you can’t work.

Do You Need Both Short-Term and Long-Term Disability Insurance?

You might be wondering if it’s necessary to have both types. Here’s the bottom line:

Long-term disability insurance is the most critical.

If you rely on your paycheck (and most of us do), an LTD policy is very important to have. A long-term disability can be financially devastating without insurance – imagine no income for a year, or several years. Unfortunately, few people have enough saved to weather years of no salary.

That’s why long-term coverage is often considered essential even if it costs a bit in premiums. It’s hard to self-insure a multi-year disability. As one financial rule of thumb: just over 1 in 4 workers will face a long-term disability in their careerl, and most don’t have the savings to sustain that. Long-term insurance fills that gap.

Short-term disability insurance is nice to have (and often free through work), but you might self-insure this part.

If your employer offers a short-term disability benefit at low or no cost, it’s usually wise to opt in – it’s essentially a paid safety net for the first 3-6 months of a disability. However, buying a standalone short-term policy on the open market can be costly and often not worth the price relative to the benefit period. Because short-term policies can cost nearly as much as long-term ones, many financial advisors suggest that if you have to choose, prioritize long-term coverage.

For the short-term risk (the initial few months of no work), you can try to build an emergency fund to cover 3-6 months of expenses, which would serve the same role as a short-term policy. Essentially, if you have a healthy savings cushion or other resources to get through a few months, you may forgo paying for a private short-term policy and rely on savings for short gaps.

If short-term is provided by your job, absolutely take it.

Employer group plans are often subsidized or free. It’s a no-brainer to accept that benefit since it costs you little and would pay out if needed. Also, some states (CA, NJ, NY, etc.) automatically provide a form of short-term disability to workers via state programs, which you’re likely paying into through payroll taxes. In those cases, you effectively already have some short-term coverage by law.

Having both maximizes protection.

If budget isn’t an issue (or if one is employer-paid), having both types means you won’t worry about any gap. Short-term will pay you for the initial weeks/months of a disability. By the time it runs out (say after 6 months), your long-term policy will be ready to kick in (since most long-term policies have a 90 or 180-day waiting period that the short-term policy would cover).

This combo ensures that whether you’re out for 2 months or 2 years, you’re getting income. Many people do end up with both – often via an employer’s short-term plan and an individual long-term policy for full coverage.

Bottom line: Don’t skip long-term disability insurance. It’s not as “optional” as some think – the financial risk of a long-term disability is high. Short-term disability insurance is very useful if you can get it cheaply (especially from an employer). But if it’s not accessible or affordable, focus on an emergency fund for short-term needs and secure a long-term policy. That strategy gives you near equivalent protection.

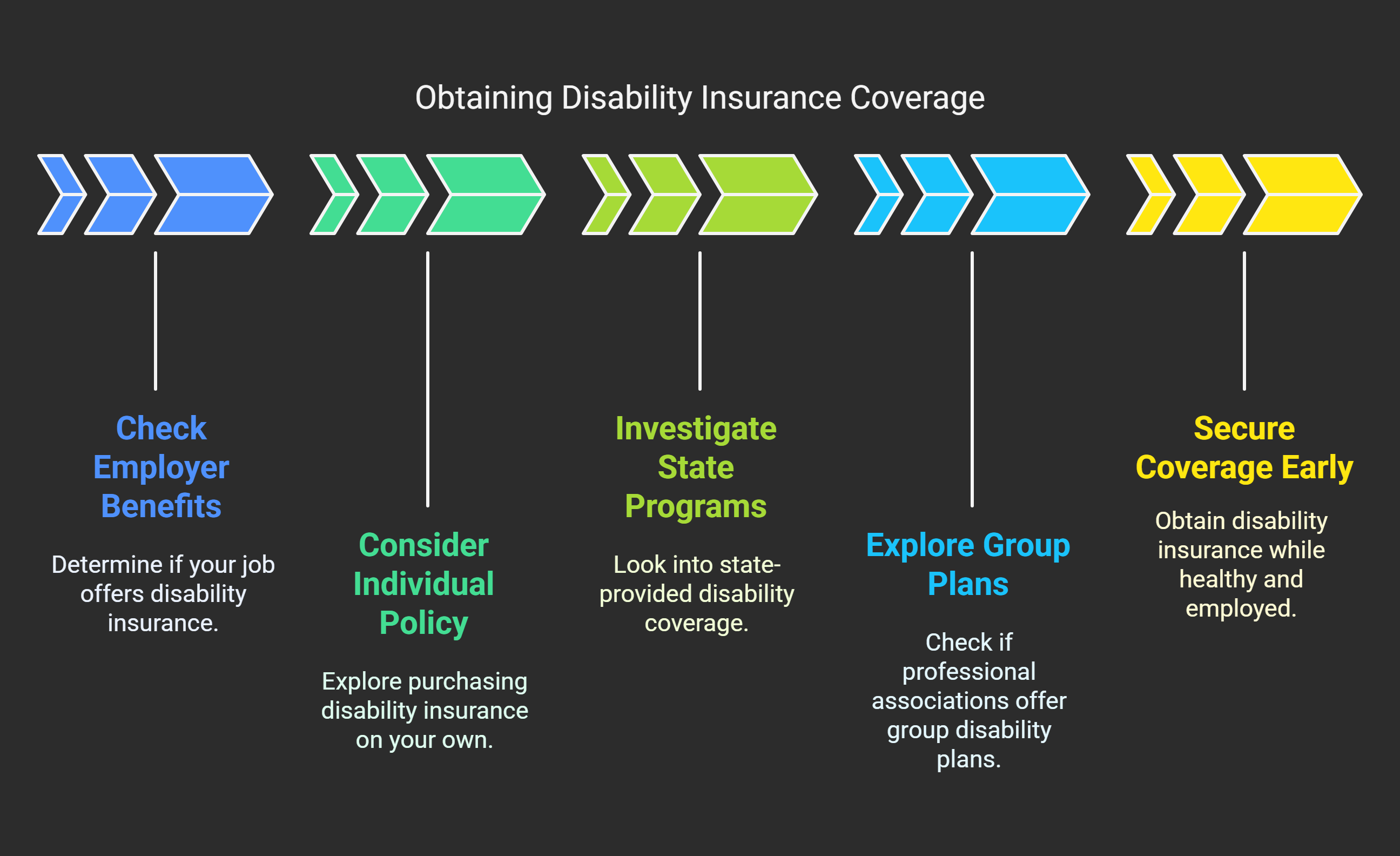

How to Get Disability Insurance Coverage

Getting coverage depends on your situation. Here are common ways to obtain short-term or long-term disability insurance:

Through Your Employer:

Check if your job offers disability insurance. Many employers provide short-term disability (often employer-paid or voluntary enrollment) and long-term disability as part of a benefits package. You may need to sign up during open enrollment. Employer plans are convenient and often cheaper than individual policies. However, keep in mind if you leave the job, you usually lose that coverage. Some employer long-term plans also cover only a base amount (e.g. 50-60% of pay) and you might consider buying an extra individual policy to top it up.

Buy an Individual Policy:

You can purchase long-term (and in some cases short-term) disability insurance on your own through insurance companies or brokers. This involves underwriting (you’ll answer health questions, maybe do a medical exam). You can tailor the policy – choose how much of your income to replace, the waiting period, and benefit period.

State Programs:

As noted, a handful of states automatically provide short-term disability coverage or allow individuals to opt into coverage. If you’re in CA, HI, NJ, NY, or RI (or Puerto Rico), look into your state’s temporary disability insurance – if you pay into it via taxes, you can claim benefits from the state for short-term disabilities. These usually cover a portion of wages for up to 26-52 weeks, depending on the state.

Group or Association Plans:

If you are self-employed or your employer doesn’t offer benefits, sometimes professional associations offer group disability plans at discounted rates. For example, membership organizations for doctors, lawyers, or freelancers might have insurance programs you can join. These can be more affordable than going solo.

When to get it:

The best time to get disability insurance is when you’re healthy and employed. Don’t wait until health issues arise – you won’t qualify for coverage at that point. Lock in a policy early in your career if possible; premiums are lower when you’re younger, and you’ll be protected as your income grows.

Taking action on disability coverage might not be as exciting as other financial moves, but it’s a cornerstone of a solid financial plan. Protecting your income is protecting everything that income pays for – your home, your groceries, your family’s needs, your future goals.

Frequently Asked Questions (FAQs)

Can I have both short-term and long-term disability insurance?

Yes – in fact, having both is ideal for full protection. Short-term and long-term disability insurance are complementary. Short-term covers you during the initial weeks or months of a disability, and then long-term takes over if your disability extends beyond the short-term period. Many employers offer short-term, and individuals often buy a long-term policy to supplement. When you have both, you ensure you’ll receive income whether you’re out for 6 weeks or 6 years.

Which is more important, short-term or long-term disability insurance?

If you must choose, long-term disability insurance is more critical. A long-term disability (lasting many months or years) can drain your savings and derail your finances without insurance. Short-term disabilities (lasting a few weeks) are easier to cover with sick leave, vacation time, or an emergency fund.

How much of my salary will disability insurance pay?

It depends on the policy. Short-term disability policies often pay around 60-70% of your gross salary (some even up to 80%). Long-term disability typically pays about 50-60% of your gross salary. The idea is that, with taxes and some work expenses gone, this benefit comes close to your normal take-home pay. You generally can’t replace 100% of your income (insurance companies want you to have some incentive to return to work).

Does short-term disability insurance cover pregnancy and maternity leave?

Yes, in most cases pregnancy, childbirth, and recovery are covered reasons for short-term disability. Many women use short-term disability benefits to receive part of their salary during maternity leave (typically covering the recovery period, e.g. 6-8 weeks for childbirth, or more if there are complications). Pregnancy is actually one of the most common claims for short-term disability.

What if I become disabled and I don’t have any disability insurance?

Unfortunately, without disability insurance, you’ll have to rely on other resources if you can’t work. This might include using up your savings, tapping into retirement funds (which can be costly), borrowing money, or depending on family. You might qualify for Social Security Disability Insurance (SSDI), but it’s hard to qualify and the benefits are limited – the average SSDI benefit in 2024 was about $1,700 per month, which for most people is much less than their salary. SSDI also has a 5-month waiting period and strict criteria. Workers’ compensation could help, but only if your disability is due to a work-related injury or illness.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)