Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Subscription Overload? 7 Ways to Get Rewards from Your Subscriptions

July 1, 2025

A typical modern household juggles numerous streaming and online subscriptions. Instead of letting these recurring charges pile up, why not make them work in your favor? Americans now pay for an average of 5+ subscription services, shelling out about $90 per month, which can feel like death by a thousand cuts.

The good news is you don’t necessarily have to cancel all the fun stuff to rein in costs – you can turn “subscription overload” into a source of rewards and savings. Here are seven savvy strategies to get rewards from your subscriptions (yes, really!), so you can enjoy them guilt-free.

1. Pay with the Right Rewards Credit Card

One of the easiest ways to get something back from your subscriptions is to put those charges on a cashback or points credit card. Many credit cards offer bonus rewards for certain subscription categories:

- Streaming services: Some cards give 6% cash back on select U.S. streaming subscriptions, cash back is received in the form of Reward Dollars that can be redeemed as a statement credit and at Amazon.com checkout.

- Entertainment & music: Cards such as Capital One Savor Cash Rewards Credit Card or Wells Fargo Autograph℠ give 3% back (or 3x points) on entertainment, including streaming and music services.

[[ CARD_LIST * {"ids": ["3041","3023"]} ]]

- Phone and internet bills: Don’t overlook these recurring subscriptions. For example, the US Bank Cash+ Visa Signature Card lets you choose categories like home utilities or TV/streaming for 5% back on up to $2,000 per quarter.

[[ SINGLE_CARD * {"id": "2353", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "No Annual Fee Card"} ]]

- App subscriptions/software: If you pay for cloud storage or software (Adobe Creative Cloud, Microsoft 365, etc.), consider a flat-rate 2% cashback card (like the Citi® Double Cash Card if no card offers specific bonuses. Two percent back on a $15/mo software sub is modest but better than 0% from a debit card.

[[ SINGLE_CARD * {"id": "580", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Everyday Spenders", "headerHint": "No Annual Fee"} ]]

- Niche subscriptions: Are you an Apple One bundle subscriber or pay for Apple TV+? The Apple Card gives 3% back on Apple subscriptions. Got an Amazon Prime membership? The Prime Visa gets 5% back on all Amazon spending (effectively giving you a 5% rebate on that Prime fee and any Prime Video channels).

[[ CARD_LIST * {"ids": ["145","79"]} ]]

Designate a single “subscriptions card” to put all recurring charges on. Not only will this maximize rewards, it also makes it easier to track your subscription spending at a glance each month (all in one statement). Many card issuers categorize or flag recurring transactions in their apps, helping you spot sneaky auto-renewals.

2. Leverage Credit Card Perks and Credits

Beyond points and cashback, some credit cards come with built-in perks that directly offset subscription costs:

- Statement credits: Premium cards often have credits for digital subscriptions. If you’re already paying for Disney+, Netflix, or The New York Times, using the Platinum essentially makes those free (up to the credit limit).

- Free subscriptions: Certain cards grant complimentary memberships. In the past, we’ve seen cards give a free year of Amazon Prime, ShopRunner, or Lyft Pink. Always check your card’s benefits page – you might discover you have a free subscription you’re not using! For instance, some Chase cards offered a year of DoorDash DashPass (subscription for free deliveries) at no charge.

- Cell phone plan bundles: Not exactly a credit card perk, but related – if your cell phone plan includes free streaming (like T-Mobile’s Netflix on Us, or Verizon’s Disney+ bundle), make sure to take advantage. It’s essentially a subscription you get without paying extra, which reduces the number of separate services you pay for. It’s part of “getting rewarded” for what you already pay (your phone bill).

Review the benefits of cards you already have – you might be surprised. If any of your subscriptions could be covered by a card’s perk, link that subscription to that card. It’s found money. For example, if you have an Amex Platinum, run all your supported streaming through it to fully utilize that $20 monthly credit.

3. Use Cashback Portals and Loyalty Programs for Sign-Ups

When starting a new subscription, don’t go directly to the service’s website without checking for cashback or points offers. Many subscription services partner with shopping portals or have referral deals:

Cashback portals (Kudos, etc.):

Kudos offers Boost rewards for signing up for services. For example, we have given bonuses like $12.50 back for signing up for Disney+, $2.50 for Hulu, or $15 for Sling TV. It’s essentially a rebate on your subscription. If you click through Kudos to subscribe, you’ll earn that cash in your account.

Airline/shop portals:

Similarly, airline mileage portals occasionally give miles for subscriptions. For instance, American Airlines’ eShopping portal might give 500 miles for an annual streaming sign-up. It pays to check CashBackMonitor or the airline portals before subscribing – you might snag some miles just for signing up via their link.

Loyalty and referral bonuses:

Some subscription services have their own loyalty or referral programs. Audible, for example, often gives you $20 credits for every friend you refer (and they get a discount too). Meal kit subscriptions like HelloFresh or Blue Apron frequently have “give $X, get $X” referral deals.

If you’re sticking with a service, refer friends or family – those credits effectively reward your subscription. Meanwhile, some services (like magazine or coffee subscriptions) have loyalty points for each renewal – don’t ignore those programs; redeem your points periodically for free boxes or months.

The key here is to treat subscribing like shopping – always ask, “Can I get a reward for signing up or paying for this?” A few minutes of checking can yield cash back or points that make the cost feel a lot better.

4. Opt for Annual Plans or Bundles (When It Makes Sense)

Many services charge less per month if you pay annually. If it’s a subscription you’re confident you’ll use for 12 months, consider switching to the annual plan to save 10-20% (common discount range). For example, a service might be $10/month or $100/year – that’s $20 saved annually.

Then, pair that with a rewards card to get cashback on that big upfront payment. You’ll get the savings and the rewards in one chunk. Just make sure the service is a keeper; it’s only a deal if you don’t end up canceling mid-year (since annual fees usually aren’t refundable).

Bundling is another powerful way to be rewarded for loyalty:

- Streaming services like Disney+, Hulu, and ESPN+ come in a bundle that is cheaper than paying each separately. If you already pay for 2 of those, the bundle essentially gives the third free.

- Amazon’s Subscribe & Save (for product subscriptions) is a form of bundle – five items in one delivery yields 15% off your whole batch. That’s a direct saving for subscribing, which is like getting a reward in advance.

- Family plans or multi-user plans: Many digital subscriptions (Spotify, YouTube Premium, Microsoft 365, etc.) have family options that drastically lower cost per person. If you can share with trusted family or friends, it’s a win-win: you each pay less. It’s not “earning rewards” in the traditional sense, but it is maximizing value – you’re getting more service per dollar. Always check if a “family/share” plan exists before everyone pays separately.

In summary, by paying smart (less frequently or in groups), you “earn” an effective return on your spending – keep an eye out for those opportunities.

5. Take Advantage of Free Trials – Strategically

Free trials are the ultimate short-term reward: a month of service for $0. However, they become anti-rewarding if you forget about them and get charged inadvertently. The strategy is to use free trials to stagger or sample subscriptions you want without overlap, and set yourself reminders to cancel in time:

- Never sign up for too many trials at once. Instead, plan them out one at a time so you can fully enjoy a service for a month, then move to the next. For example, use one month of HBO Max (free), binge what you want, cancel, then next month trial Starz or another service.

- Calendar reminder: The moment you start a trial, put an alert in your phone 2-3 days before it ends. For instance, “Cancel Amazon Music trial by Aug 29.” This way, you won’t accidentally roll into a paid month and lose money.

- If you do forget and get charged, many services will still let you cancel and refund if it’s just a day or two into the cycle – set a second reminder on the actual renewal day to catch any charges immediately.

- Use a single credit card (could be a separate one from your main subscriptions card) for trials. Some savvy users even use virtual credit card numbers that expire, so if you forget to cancel, the payment won’t go through – essentially forcing the trial to end. (This is an advanced tactic and requires a card/bank that lets you create disposable virtual card numbers).

By cycling free trials, you can enjoy a lot of content or services without paying at all for months, which is the ultimate reward. Just be organized about it. The “reward” here is savings, but think of it as getting those entertainment or service benefits free for a time – it’s like a bonus period before you start paying.

6. Look for Coupons, Discounts, and Promotions

It sounds obvious, but many people forget to treat subscriptions like any other purchase when it comes to coupons or promo codes. Before subscribing to anything, search for promo codes or deals:

- Seasonal sales: Streaming services and other subscriptions occasionally have sales (Black Friday deals, New Year’s promotions). For example, Hulu has run a Black Friday promo of

$0.99/month for a yearin the past for new subscribers. If you time it right, you could get a year of Hulu for the cost of one month – a huge win.

- Student/Teacher/Military discounts: If you fall into these categories, check if the service has a special plan. Spotify Premium Student, for instance, is cheaper and comes bundled with Hulu and Showtime (bundle reward!). Many software subscriptions have educator discounts. These special rates aren’t always heavily advertised, so it’s worth googling “[Service] student discount” etc.

- Welcome back incentives: If you cancel a subscription, don’t be surprised if you get an email a few weeks later with a “We want you back – here’s 3 months for 50% off” offer. Companies often dangle promotions to re-engage former customers. This isn’t exactly a reward you earn, but you are being rewarded for taking a break. So if you can live without a service for a while, consider cancelling and waiting for a comeback deal.

Every dollar saved via a promo is a dollar you effectively “earned.” Stack this with paying by the right card, and you’ll get a double benefit: upfront discount + rewards on the post-discount price.

7. Use Subscription Management Tools that Negotiate or Find Savings

If the tips above sound like a lot of manual effort, you’re in luck – there are apps that do some of this for you:

- Apps like Rocket Money (Truebill) or Trim can scan your bank statements and flag all your subscriptions (making it easier to see everything in one place). They can even auto-cancel ones you don’t want with a swipe. But beyond that, these apps sometimes find savings: Trim, for example, will negotiate your cable or phone bill down and take a cut of the savings. If a subscription service is overcharging you or there’s a promo rate you missed, these negotiators try to snag it for you.

- Some management tools alert you of price increases. Subscription prices creeping up is common (think Netflix price hikes). A tool that says “Your bill for X will increase next month” is giving you a chance to react – either cancel or call the company and ask for a retention deal (which often works! Companies would rather give you a temporary discount than lose you).

- Even your bank or credit card may offer this: for instance, certain banks’ apps have a feature that lists “Recurring payments” so you don’t have to hunt. Use these free features to stay on top of what you’re paying for.

While these apps might charge a small fee or take a commission, they can be worth it if you’re too busy. Consider any savings or refunded charges they secure as rewards for you. Just be sure to weigh the cost – if an app charges $5 a month but helps you cancel $50 of unwanted subs and saves you $10 on a bill, that’s a net gain.

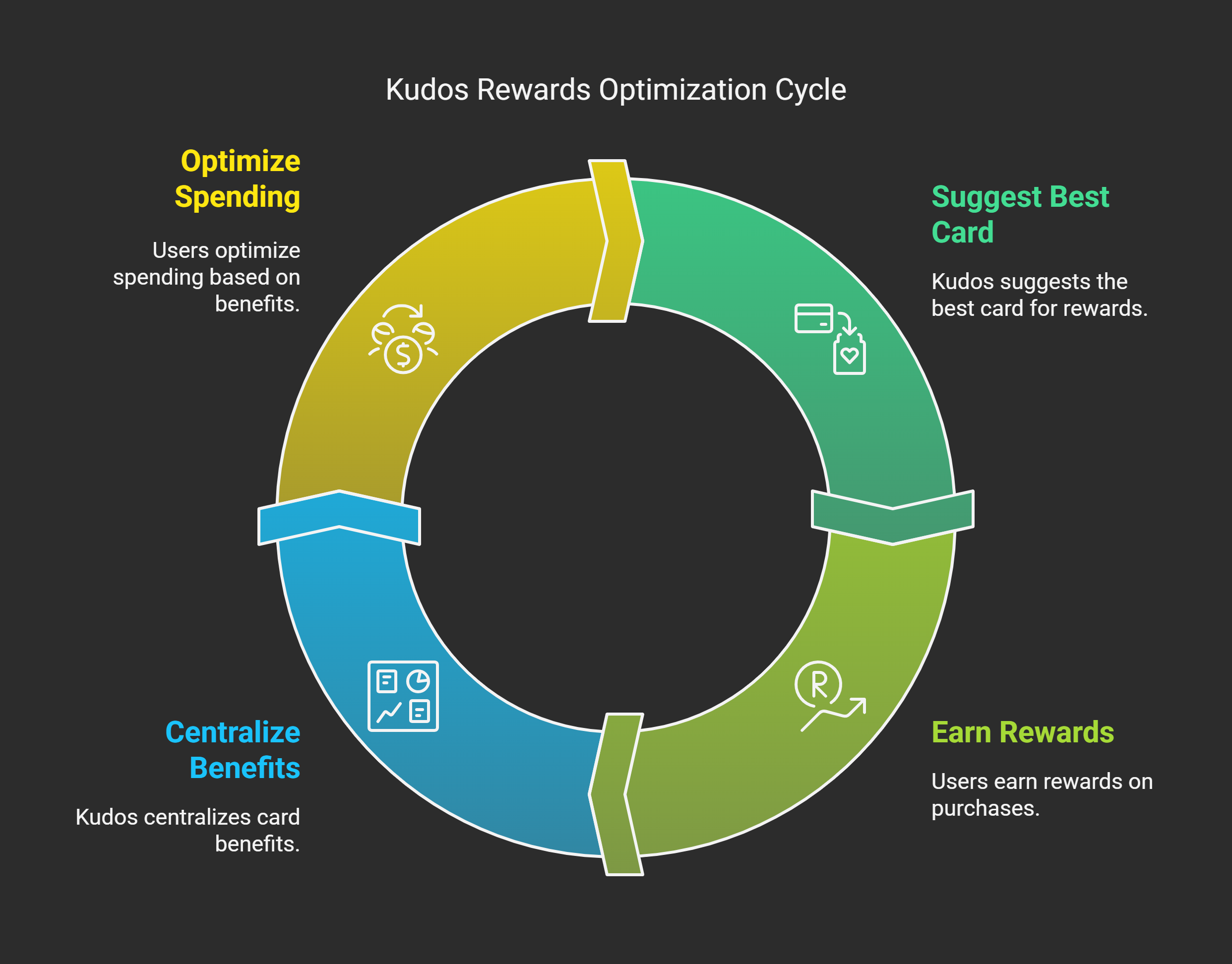

Speaking of helpful tools, have you tried Kudos? Kudos is a free browser extension that can be your secret weapon in this battle. While you’re shopping or managing accounts online, Kudos automatically suggests the credit card that will earn you the most rewards for that purchase – including subscriptions. So, when you’re about to pay for a subscription, Kudos might pop up and say “Hey, use Card X for 5% back.” It’s like having a personal rewards advisor.

It also centralizes your card benefits, so you’ll never miss out on a streaming credit or offer. This way, you ensure every subscription you keep is paid in the smartest way possible. (We’re biased, but our users report earning hundreds in extra rewards by optimizing their spending with Kudos!)

By implementing these strategies, you can tame your subscription overload and even feel good about the ones you keep. Instead of silently draining your bank account, your subscriptions will start pulling their weight by delivering cashback, points, and discounts. Remember, the goal is to be intentional: subscribe to what you love, cancel what you don’t, and maximize rewards on every dollar spent. With a little effort (and smart tools like Kudos in your corner), you’ll transform from subscription overload to subscription optimized. Happy streaming/shopping/reading – and happy rewarding!

Frequently Asked Questions

Can I really save a lot by getting rewards on subscriptions?

Absolutely – it adds up. Think of it this way: If you spend $100 a month on various subscriptions and put it all on a 5% cashback card, that’s $5 back each month, or $60 a year. Add any sign-up cashback deals (say you got $20 from Rakuten for a yearly sign-up) and maybe a $50 streaming credit from a card, and you’ve easily clawed back over $100 in value annually. That’s real money. Plus, if you optimize with sharing plans or annual discounts, the savings compound. It won’t make you rich overnight, but it can easily cover the cost of one or two of your subscriptions each year, effectively making them free for you.

Isn’t it better to just cancel subscriptions I don’t use?

Of course! The first step is always to cut the subscriptions you don’t value – no rewards trick can make a completely unused gym membership worth paying for. We always recommend doing a subscription audit (check the last 12 months statements for what you’re paying) and cancel anything you haven’t used in a month or two. That said, for the ones you do use and love, the tips in this article help you keep them at a lower net cost. It’s all about getting value. Cancel the duds, optimize the keepers.

Are there any risks to putting all my subscriptions on a credit card?

The main thing to watch out for is carrying a balance. Ideally, you should pay off your credit card in full each month, so the rewards aren’t negated by interest charges. If you’re someone who tends to forget payments, one idea is to set your credit card to autopay from your bank account for at least the minimum (or full amount). That way you won’t miss a payment even with many subscriptions on it.

The content on this page is accurate as of the posting date; some offers may have expired.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)