Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

The 5 Best Places to Keep Your Emergency Fund

July 1, 2025

You’ve worked hard to save up an emergency fund – a nice stash of cash for life’s unexpected moments. Now the question is: where do you keep that money? Stashing it in the right place is important. You want your emergency fund to be safe (protected from loss), liquid (easy to access quickly), and if possible, earning a bit of interest (so inflation doesn’t eat it away).

Some people just leave their emergency fund sitting in their regular bank account, while others explore options like special savings accounts or even investments. In this article, we’ll go through the 5 best places to keep an emergency fund, and also mention a few places not to keep it. By the end, you’ll know exactly where to park your rainy-day funds so that the money is there for you when you need it most.

1. High-Yield Savings Account (HYSA)

Best for: Most people – this is the top choice for emergency savings.

- Safety: These accounts are typically FDIC-insured (if it’s a bank) or NCUA-insured (if a credit union) up to $250,000. That means your money is protected by the U.S. government – you won’t lose it even if the bank goes under.

- Liquidity: You can withdraw money whenever needed. Usually, you’d transfer from the savings to your checking account, which can be instant if at the same bank or 1-3 days if different banks. Some high-yield savings accounts also offer an ATM card or allow wire transfers for faster access. Because emergencies can strike anytime, having funds you can get to within a day is important.

- Interest Earnings: While the primary goal of an emergency fund isn’t to make money, why not earn a little extra? High-yield accounts often pay anywhere from 3% to 5% annual interest (as of recent rates). This helps your fund grow on its own. For example, $10,000 earning 4% will make about $400 in a year – not bad, that could offset inflation or add to your fund.

- No Fees/Minimums (in many cases): Many online savings accounts have no monthly fees and low or no minimum balance requirements. This makes them easy to open and maintain.

Example: Ally Bank, Capital One 360, Marcus by Goldman Sachs – these are a few popular high-yield savings options known for consistent rates and no fees. If your emergency fund is, say, $5,000, putting it in one of these could yield maybe $15-20 a month in interest (rates vary), all while being fully accessible.

Tips: Keep your emergency savings in a separate bank from your main checking account. This adds a slight “friction” that prevents impulsive use, yet it’s still accessible. Also, enable any features like auto transfers to seamlessly grow the fund. High-yield savings accounts are widely considered the best home for emergency funds – you really can’t go wrong with this choice.

2. Money Market Account

Best for: Those who want check-writing or debit access on their emergency fund while still earning interest.

A money market account (MMA) is like a hybrid between a savings and checking account. It’s also insured (FDIC/NCUA) and offers interest rates often comparable to high-yield savings, though some may require higher minimum balances.

The key differences:

- Liquidity & Access: Many MMAs come with a debit card and/or check-writing privileges. This means in an emergency, you might not even need to transfer funds – you could directly write a check or swipe the card to pay the expense. This immediate access can be useful for certain emergencies (e.g., paying a tow truck driver on the spot, covering an emergency room co-pay, etc.).

- Interest: Historically, money market accounts had slightly higher rates in exchange for higher minimums, but nowadays online savings and MMAs are often pretty similar in yield. You can find money market accounts with competitive rates; just compare a few.

- Considerations: Be mindful of any minimum balance requirements. Some MMAs say “to get 4% APY, keep at least $5,000 in the account” or they might charge a fee if your balance is under a threshold. Many modern ones have eliminated such fees, but check the terms.

In summary, a money market account can serve as an emergency fund home just as well as a high-yield savings. If you like the idea of directly accessing the money via checks or a card – perhaps giving you an extra sense of readiness – an MMA is a great choice. If you don’t think you’d need that, a regular high-yield savings might suffice.

Note: Don’t confuse a money market account with a money market fund. A money market fund is an investment product (offered by brokerage firms) not insured by FDIC – those are generally not recommended for your emergency fund because, while quite stable, they aren’t government-insured. Stick to accounts at banks/credit unions.

3. No-Penalty Certificates of Deposit (CDs)

Best for: Those with larger funds who won’t likely need all the cash immediately, and want to earn a bit more interest on a portion of their emergency money.

A certificate of deposit (CD) is a time deposit – you lock up an amount of money at a bank for a set term (3 months, 1 year, 5 years, etc.) and in return, you get a guaranteed interest rate. The catch: if you withdraw early, you typically pay a penalty (forfeiting some interest). That penalty aspect is why standard CDs aren’t ideal for emergency funds – because emergencies don’t care about your CD’s maturity date.

However, there are no-penalty CDs (also called “liquid CDs”) that allow you to withdraw at any time after, say, 7 days from opening, without penalty. These can be a good option to slightly boost yield while keeping accessibility:

- Higher Interest Rates: No-penalty CDs often offer interest rates a bit above regular savings accounts. For example, a bank might offer a 11-month no-penalty CD at 4.5% APY whereas their savings is 4.0%.

- Liquidity: You can withdraw the full balance any time (after the first week or so) with no fees. Usually, you can’t make partial withdrawals – you’d have to break the whole CD. But you could set up multiple smaller CDs (laddering) if needed.

- Use Case: One strategy is to keep a portion of your emergency fund (that you think is less likely to be needed urgently) in a no-penalty CD to earn extra interest, and the rest in a regular savings for immediate needs. For example, suppose you have $20k emergency fund. You could keep $15k in a savings account and $5k in a 6-month no-penalty CD at a higher rate. If a minor emergency arises, you use the savings. If a big emergency hits that requires all funds, you break the CD (no cost) and get your $5k plus interest up to that point.

- Important: Only use no-penalty CDs (or very short-term CDs if you’re staggering maturities). Traditional CDs that charge 3-6 months of interest as a penalty for early withdrawal are not as suitable – because Murphy’s Law says your emergency would happen right after you lock your money up.

Banks like Ally, Marcus, and others frequently offer no-penalty CD options. They can be a nice middle-ground to squeeze a bit more earnings from your emergency stash without sacrificing the ability to get to it.

4. Treasury Bills or “I-Bonds” (Advanced Option)

Best for: Those with a fully funded emergency stash who want to protect against inflation or earn extra, and who can handle a bit of complexity. Also for people who likely wouldn’t need the money for smaller emergencies.

This is a more advanced option, and optional – you certainly don’t need to do this. But some financially savvy folks use U.S. Treasury bills or Series I Savings Bonds as part of their emergency fund strategy:

Treasury Bills (T-Bills):

These are short-term government bonds that mature in 4, 8, 13, 26, or 52 weeks. They are ultra-safe (backed by the U.S. government). You can buy them through TreasuryDirect or a brokerage. For emergency funds, you might use a T-Bill ladder – for example, buy a 4-week bill that rolls over each month, or stagger some 8-week and 12-week ones so something is maturing frequently.

The idea is you’d have frequent access points (when each bill matures, you can choose not to reinvest and take the cash). T-bills often yield competitive rates. However, if you needed to cash out before maturity, you’d have to sell it (which could be slightly less convenient, though short duration means price changes are minimal).

Series I Bonds (I-Bonds):

These are savings bonds that adjust with inflation. They have a catch: you cannot redeem them in the first 12 months after purchase, and if you redeem within 5 years, you lose the last 3 months of interest as a penalty. Because of that 1-year lockup, I-Bonds aren’t accessible for true emergencies during that first year.

Some people still use them as a long-term emergency reserve that doubles as inflation-protected savings. For example, they might keep $10k in I-Bonds as a “backup to the backup” that also earns interest indexed to inflation. After year 1, it becomes accessible (with the small interest penalty if before 5 years).

Considerations:

Using these instruments makes your emergency fund a bit less liquid and more complicated to manage. It’s generally not recommended for your primary emergency fund unless you really know what you’re doing and are okay with possibly not having immediate access. They could make sense if your fund is large and you want to hedge against inflation or eke out more return.

For instance, during times of high inflation, I-Bonds have yielded 7-9%, which outpaces any bank account – very tempting to protect your fund’s value. A prudent approach: only put money into I-Bonds that you won’t need for at least a year (maybe the last portion of a 6-month fund once you have other parts covered).

In summary, Treasury bills and I-Bonds are super safe in terms of credit risk, but less liquid. They’re optional tools to increase interest earnings on part of your emergency money. If simplicity and guaranteed access are your priorities, sticking with high-yield savings or MMAs is perfectly fine. These government securities are just extra arrows in the quiver for those comfortable with them.

5. Traditional Checking or Cash (Small Amounts Only)

Best for: Short-term parking or keeping a tiny immediate stash; not ideal for the bulk of your fund.

Your everyday checking account or plain cash at home might seem convenient for emergency money – after all, what’s more accessible than your wallet or a quick ATM withdrawal? But there are downsides to using these as the main home for an emergency fund:

- Checking Account: It’s very liquid, yes. However, most checking accounts pay little to no interest. Your money won’t grow and might even lose value to inflation. Also, having a large sum in checking can be tempting to spend or accidentally dip into since it’s mixed with your regular spending money. One advantage is instant access – you swipe your debit card or write a check and you’re done. But you can simulate that by linking a savings account to checking for quick transfers. Some people keep a month’s worth of expenses in checking as a buffer (which doubles as mini emergency fund), but beyond that it’s better to earn interest elsewhere.

- Cash at Home: It’s wise to have some physical cash for emergencies (like power outages, natural disasters, or situations where digital banking is down). However, cash earns nothing and can be lost (theft, fire, etc.). So, you might keep a few hundred dollars hidden in a safe place at home for immediate needs, but not thousands. For example, $300 in cash can pay for a night in a motel, a tank of gas, and some food if you evacuate during a hurricane – that’s useful. But $5,000 in cash sitting around is risky and losing purchasing power over time.

Bottom line: Use checking and physical cash only for short-term or small emergency funds. If you’re just starting out and only have $500 saved, it’s okay to keep it in checking for now (the priority is having it available). But once your fund grows, move it into higher-yield savings. And maintain a small cash stash for true immediate-access scenarios, but keep the bulk of funds in an insured account where it’s safe and not tempting to spend.

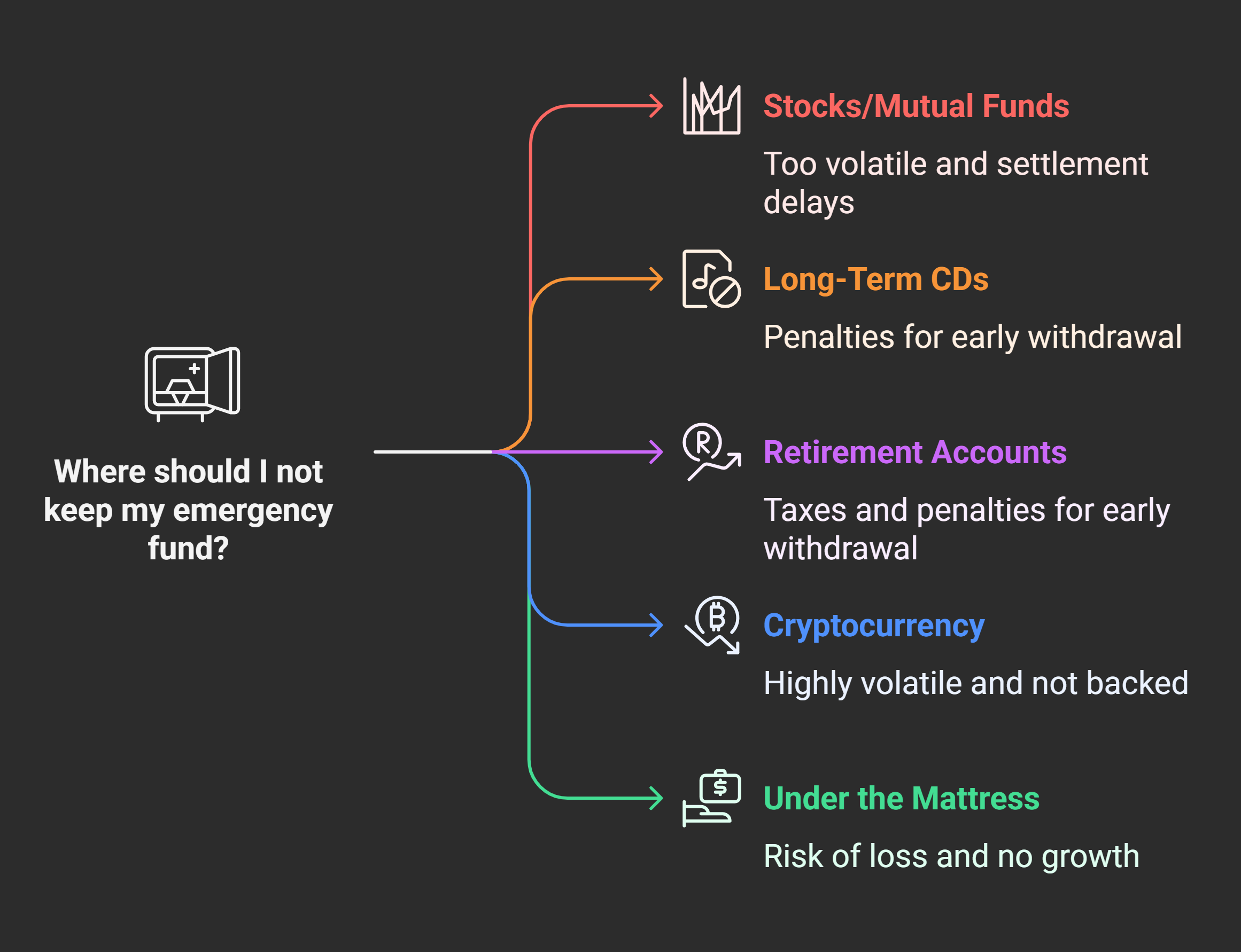

Places Not to Keep Your Emergency Fund

Just as important as where to keep your fund is where not to keep it. We’ve hinted at some, but let’s make it explicit:

- Stocks or Stock Mutual Funds: These are too volatile. A market downturn could shrink your emergency fund right when you need it most. Plus, selling investments can take a couple of days for settlement.

- Long-Term CDs (without no-penalty): Locking your only emergency money in a 5-year CD, for example, is not wise. The penalties will eat your money if you break it early, and you can’t predict timing of emergencies.

- Retirement Accounts (401k, IRA): You should generally not rely on a 401k or IRA as an emergency fund. Withdrawing early often incurs taxes and penalties, and it hampers your retirement. There are some exceptions (like Roth IRAs, you can withdraw contributions without penalty), but it’s best to keep emergency savings separate from retirement nest eggs.

- Cryptocurrency: Crypto is highly volatile and not backed by anything. It’s definitely not a store for emergency savings you need to be stable. A 30% price swing in a month is not what you want for your safety net.

- Under the Mattress (for large sums): We covered cash – safe for a little, not for a lot. Under the mattress or buried in the yard might feel old-school safe, but you risk loss (and no growth). The bank insurance exists for a reason – use it.

In short, keep your emergency fund boring. That usually means a bank account of some sort. Boring is good when it comes to money you absolutely need to be there in an emergency.

Making a Choice and Combining Options

You don’t necessarily have to pick just one of the above options – sometimes a combination works best. For example, a popular setup is:

- Majority in High-Yield Savings: e.g., 70% of your fund in an online savings account (for easy access and solid interest).

- Some in a No-Penalty CD or MMA: e.g., 20% in a no-penalty CD to get a bit more yield or an MMA for check access.

- Small amount in Checking/Cash: e.g., 10% or a few hundred dollars in your checking or as cash for immediate needs.

This way, you’ve covered all bases: instant access for very urgent things, quick access for most emergencies, and a little extra earning on a portion of funds.

However, if this feels too complicated, don’t worry – sticking 100% of your emergency fund in a single high-yield savings account is absolutely fine and probably what most people should do. It checks all the main boxes.

The key is that you’ve saved this money to protect yourself, so ensure it’s in a place where it will be there for you 100% when needed. All the above recommended options achieve that (in different ways and with slight pros/cons). Pick what suits your comfort.

Final Thoughts

The best place for your emergency fund is one that balances security, accessibility, and earnings. For most, an FDIC-insured high-yield savings account is the winner – it’s simple and effective. Other options like money market accounts or no-penalty CDs can enhance convenience or returns for those who want them.

Take a moment to evaluate your own needs:

- Do you value having a debit card attached (MMA might be good)?

- Do you want to maximize interest (maybe a CD for part of it)?

- Are you content moving money via an app when needed (savings account is perfect)?

Once you choose a home for your emergency fund, you can set it and mostly forget it – just let it sit there until that rainy day arrives. And hopefully, many of those days won’t come. But if they do, you’ll be ready, and your money will be ready to work for you as intended.

Stay safe, and happy saving!

Emergency Fund Storage FAQs

Should I keep my emergency fund in the same bank as my checking?

There are pros and cons. Keeping your emergency fund in the same bank as your checking (just as a savings account) can make transfers instantaneous – which is great for quick access. It’s very convenient in an emergency to just move money over and use it. However, the downside is temptation and possibly lower interest. If it’s visible alongside your other accounts, you might be tempted to dip into it for non-emergencies. Also, your current bank might not offer the best interest rate on savings.

Are money market funds or investment accounts ever okay for emergency money?

Generally, it’s recommended to avoid investment accounts for your core emergency fund. A money market fund (not to be confused with money market account) is an investment product offered by brokerages – it’s usually very stable, investing in short-term debt, and often used as a cash equivalent. While money market funds are relatively safe, they are not insured by FDIC/NCUA. In rare cases, they can lose value (breaking the buck). They also might restrict access to certain times or methods (though usually you can sell anytime). Most advisors would say to keep it simple: use a bank account for emergency funds.

What about using a home equity line of credit (HELOC) or credit card instead of a stored fund?

Relying on credit (like a HELOC or credit cards) instead of an emergency fund is a risky strategy. While it’s true that a HELOC (home equity line) can provide a lump sum in an emergency, and credit cards can float expenses, they shouldn’t replace liquid savings.

How much cash should I keep at home for emergencies?

Keeping some physical cash at home is a smart part of emergency preparedness, but it should typically be a small portion of your total emergency fund. The exact amount can vary based on comfort, but common recommendations are anywhere from $100 up to maybe $1,000 at most in cash. For most scenarios, $200–$300 in various small denominations ($20s, $10s, $5s) is sufficient for immediate needs like buying food, gas, or a night in a motel. If you’re worried about larger-scale disasters (hurricanes, etc.) where ATMs might be down for days, you might keep a bit more, like $500. Keeping much more than that isn’t usually necessary and carries risks (theft, fire, etc.).

Can I split my emergency fund into multiple accounts?

Yes, you can, and many people do. Splitting your emergency fund into multiple accounts can be part of the strategy to optimize access and yield. One practical approach is a tiered emergency fund:

- Tier 1: Immediate needs – e.g., $1,000 in your checking or a very accessible savings.

- Tier 2: Main fund – e.g., 3 months expenses in a high-yield savings.

- Tier 3: Extended fund – e.g., an additional 3 months in a no-penalty CD or I-Bonds (for use in very severe or long-term emergencies).This way, smaller emergencies you handle from Tier 1 or 2 quickly, and Tier 3 is like a backup for really big situations.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)