Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

What Is Subscription Creep and How to Avoid It in 2026

July 1, 2025

The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

Subscription services make life convenient – until you realize you’re paying for dozens you barely use. “Subscription creep” is the sneaky budget killer of the digital age. In this guide, we explain what subscription creep is, why it happens, and how to stop it in 2025 so you can keep more money in your pocket.

What is “Subscription Creep”?

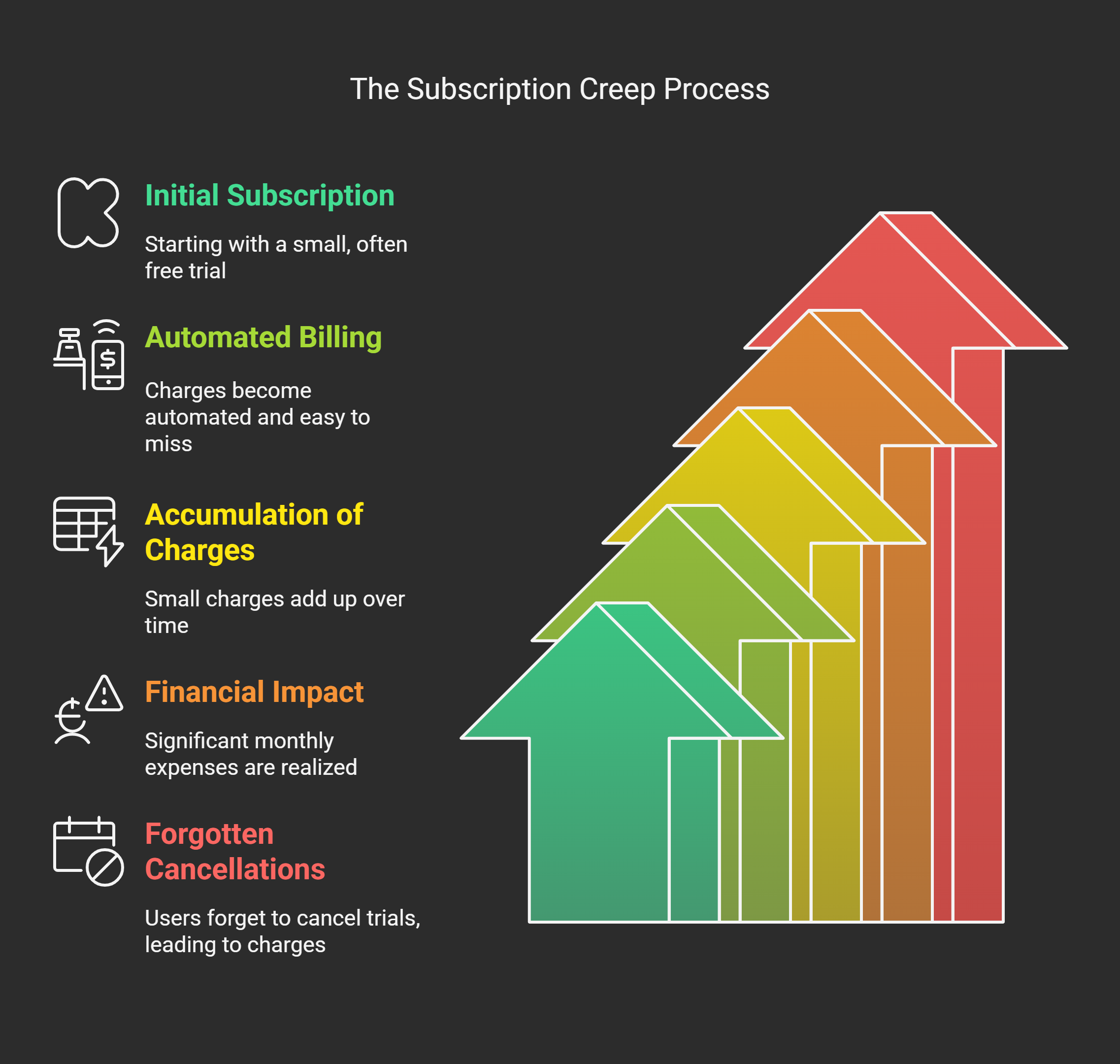

“Subscription creep” refers to the gradual accumulation of subscriptions over time that “creep up” on your finances without you fully noticing. It often starts innocently: a few $5 or $10 monthly trials here and there. But these small charges are automated and easy to overlook.

Before you know it, you might be paying $300+ per month for services you barely use. In fact, an exclusive 2024 CNET survey found U.S. adults spend $91 on subscriptions each month on average – over $1,000 a year – and 48% have forgotten to cancel a free trial before it rolled into a paid plan.

Not all subscriptions are “bad” – many provide real value (we’ll cover that later). The danger is when subscriptions pile up unnoticed or outlive their usefulness. It’s the Netflix account you haven’t watched in months, the meal kit that delivers more than you can cook, or the “free trial” of a premium app that quietly started billing you weekly. Over time, this subscription creep can drain your budget with “death by a thousand cuts”, as one expert described.

Why Does Subscription Creep Happen?

There are several reasons this phenomenon has become so common in the subscription economy of 2025:

Everything is a Subscription Now:

The subscription business model is more popular than ever for everyday products and services. Beyond streaming and gyms, we have subscription boxes for snacks, beauty products, pet toys – you name it. Companies love subscriptions because they lock in repeat customers until we actively cancel. For consumers, this means we’re inundated with offers to “subscribe and save” on every corner of the internet.

Easy to Start, Hard to Cancel:

Signing up is frictionless – often just a click, sometimes incentivized by a free or $1 trial. But canceling can be convoluted. Businesses bank on people forgetting to cancel or finding it too much hassle. Have you ever had to call a customer service line or navigate five screens to cancel a membership? You’re not alone. This deliberate inconvenience leads many to put off cancellations, allowing unused services to linger.

Set It and Forget It (Autopay):

Most subscriptions are on autopay. While auto-renewal ensures uninterrupted service, it also means “out of sight, out of mind.” You don’t actively approve each charge, so it’s easy to lose track. With no physical bills, a $9.99 charge can slip by unnoticed among other expenses. Many people only realize how much they’re spending on subscriptions when they check annual credit card summaries or bank statements.

Small Costs Add Up:

Psychologically, we tend to shrug off small monthly fees. $5 here, $12 there doesn’t feel like much day-to-day. But multiply those by 12 months – that $12 turns into $144 per year. One study found consumers underestimate their monthly subscription spending by $133 on average. We also adjust to price increases; 67% of people saw at least one subscription raise its price in the past year, often with minimal notification. These factors combined make it hard to gauge the true impact on our budget until it’s already strained.

In short, subscription creep happens because it’s extremely easy to accumulate services under “set-and-forget” billing. The convenience and low entry cost mask the long-term expense.

Why Subscription Creep Hurts Your Budget

If unchecked, subscription creep can wreak havoc on your finances:

Blows Your Budget:

Recurring expenses can silently devour the portion of your budget meant for savings or essential bills. For instance, paying an extra $100/month on barely-used services could have been $1,200 toward an emergency fund or credit card debt. In a recent survey, 12% of consumers admitted their subscriptions are outside their budget – they can’t truly afford them but pay anyway. This often leads to running up credit card balances.

Credit Card Consequences:

Many people put subscriptions on credit cards. If you’re not paying the card in full, these small charges can contribute to interest-bearing debt. Even if you do pay in full, having numerous auto-charges can inflate your credit utilization (the percentage of your credit limit used), which accounts for 30% of your FICO score. As one financial counselor noted, “if you’re paying more subscriptions than you realize, it can both hurt your budget and impact your credit utilization ratio”. In short, forgotten subscriptions could indirectly ding your credit score if they lead to higher balances relative to your limit.

Opportunity Cost:

Every dollar spent on an unused subscription is a dollar not spent on something you value. That could be investing, travel, a hobby, or even a higher-value subscription. People often lament “I can’t afford X” while unknowingly shelling out for subscriptions they’ve forgotten. By trimming the fat, you free up money for things that truly matter – whether that’s a gym you actually attend, or simply boosting your monthly savings.

Clutter and Stress:

Beyond money, there’s mental clutter in juggling too many services. You might get overlapping benefits (e.g., three streaming platforms with the same movies) or constantly sift through subscription emails. There can be anxiety in the back of your mind (“Am I still paying for that app?”). Simplifying and taking control of your subscriptions can bring peace of mind as well as financial relief.

Now that we understand the scope of the problem, let’s turn to solutions. How can you stop subscription creep and maybe even reverse it? It starts with a good old-fashioned audit.

5 Ways to Stop Subscription Creep

Taming subscription creep is very achievable with some proactive steps. Here are five strategies to regain control in 2025:

1. Conduct a Subscription Audit

Your first mission: identify all your recurring charges. This is Subscription Creep Cleanup 101. Go through the last 12 months of bank and credit card statements (to catch annual renewals). Make a list of every subscription or membership, from Netflix down to that cloud storage plan or meal kit. Don’t ignore annual bills and “offline” subs (gym, lawn service, etc.). Some credit card dashboards help by highlighting recurring transactions, which can speed this up. The goal is to see the full picture in one place. Many people are surprised at the final tally – but now you know what you’re dealing with.

2. “Multiply by 12” to Shock Yourself

Once you list out the services and their monthly cost, multiply each by 12 (or use the annual cost if billed yearly). Seeing your “$30/month music and gaming bundles” as “$360/year” can be eye-opening. For any you suspect you’ll keep for years, project 5 years out. This exercise makes the long-term cost crystal clear. A few $20-$30 subs can easily be $1,000+ a year as a bundle. Use this reality check to ask: Is this subscription still worth it to me? You might find you’d rather have that money for other goals.

3. Prune the Unused and Redundant

Now for the tough love: cancel anything that no longer provides value. Be honest: if you haven’t logged into an app or service in 3 months, you likely won’t miss it. Common culprits are unused gym memberships (the classic “I’ll go next month” trap), extra cloud storage you don’t need, or overlapping entertainment platforms.

Check for redundancies: do you need Spotify and Apple Music? Netflix, Hulu, Prime Video, and HBO Max? If you’re paying for cable but also multiple streaming services, there’s likely overlap. Pick your favorites and drop the rest – you can always rotate them (subscribe to one service at a time, then switch next month). Canceling a subscription doesn’t have to be permanent; think of it as “pausing” spending on something that isn’t providing enough value right now. Many services let you re-subscribe anytime.

4. “Subscription Detox”

Try a bold approach recommended by some experts: cancel everything non-essential, at least temporarily. Yes, everything that isn’t absolutely needed (keep your insurance and maybe one or two core services). This “subscription detox” lets you see what you truly miss. Over the next month or two, note which services you really wish you had. You might find you don’t miss half of those subscriptions at all. Then slowly add back only the ones you genuinely value. This method can reset your habits and ensure each subscription you resume is intentional. It’s like spring-cleaning for your finances.

5. Set Traps for Your Subscriptions

Make it hard for subscription creep to sneak up again. Some tips:

- Calendar Reminders: Whenever you do sign up for a trial or short-term subscription, immediately put a reminder in your calendar a few days before the renewal date. For example, if a free trial ends on June 30, set an alert on June 28 saying “Cancel X if not using.” This way you won’t lapse into a paid plan by accident.

- Use One Payment Method: Consider putting all your recurring charges on a single credit card or bank account. This concentrates them on one statement, making review easier each month. If you check that statement and see charges you don’t recognize or need, you can address them immediately. (Bonus: many credit cards categorize or flag subscription transactions, simplifying tracking).

- Leverage Tools: Utilize apps that specialize in subscription tracking. Free or low-cost apps like Rocket Money (formerly Truebill) or Trim can scan your accounts, list all your subscriptions, and even help cancel unwanted ones. Your bank or budgeting app might also have features to alert you of recurring payments. Even using a spreadsheet to log subscriptions and renewal dates can help you stay on top of them.

- Avoid Card-on-File Trials: If you’re prone to forget, adopt a rule: no free trials that require a credit card. Many experts suggest this to prevent the forgetfulness trap. If a service is truly worth it, you can always sign up when you’re ready to commit.

By implementing these steps, you’ll significantly curb subscription creep. Many readers who follow these tips find immediate savings – money that can be redirected to a rainy-day fund or a treat you actually want.

Don’t Feel Bad – Some Subscriptions Are Worth It

After an audit, you might decide that some subscriptions do earn their keep. And that’s perfectly fine! The goal isn’t to cancel everything fun in the name of frugality. It’s to be intentional and get value for the money you spend.

Ask yourself for each service: “If I cancel this, what do I lose? Does it save me time, money, or improve my life significantly?” If a meal kit subscription genuinely leads you to eat healthier or avoid takeout, it might be worth the $40/week. If your Spotify family plan brings you daily joy, keep it and cut something else that matters less. Subscriptions can be great when they add value – for example, a software subscription that helps you earn money, or Amazon Prime’s bundle of shipping, video, and music that you use heavily.

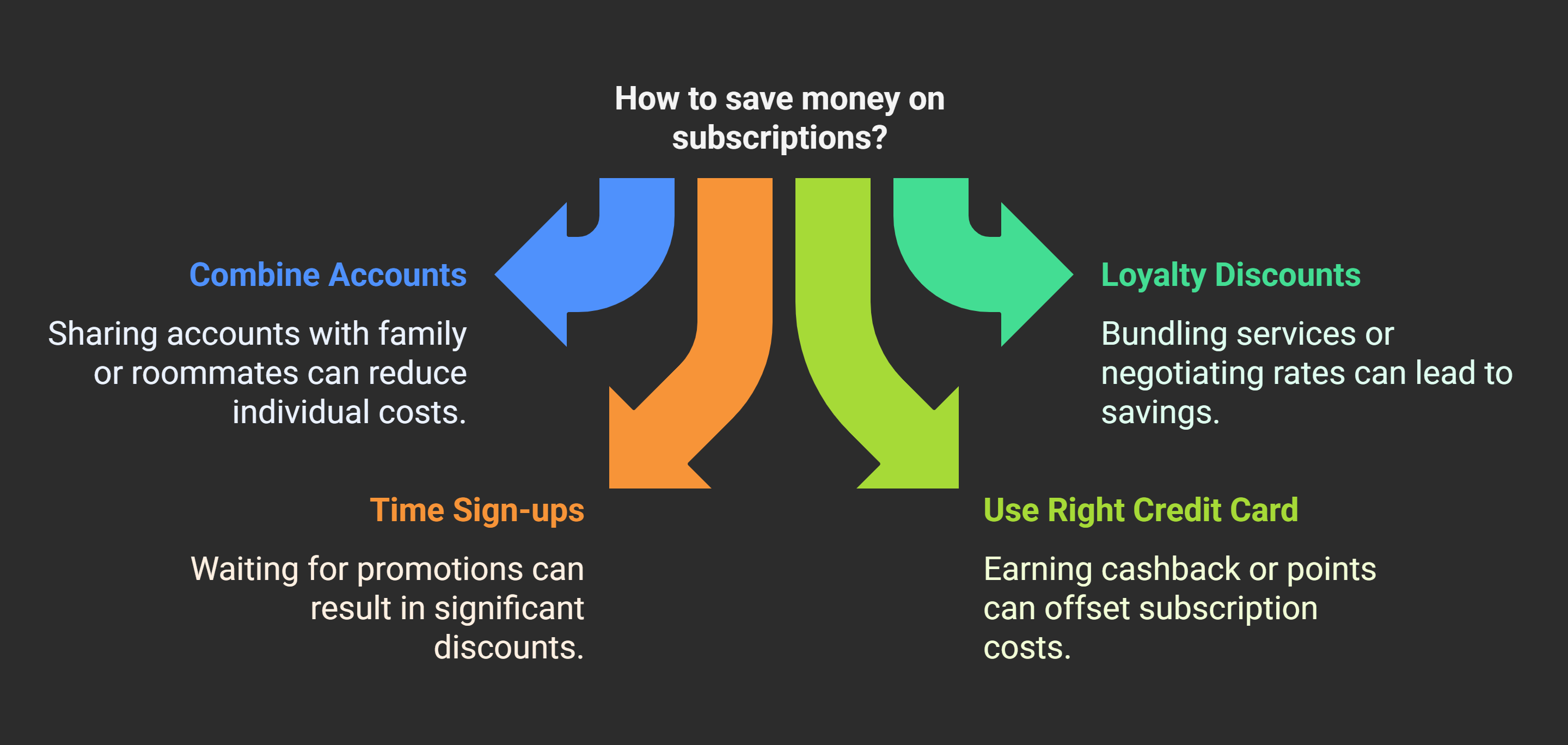

Also, consider sharing or discounts before canceling outright:

- Many services offer family or multi-user plans – are you and your roommate or sibling paying separately for the same thing? Combining accounts could cut the cost per person (e.g., YouTube TV family sharing, Spotify Duo).

- Look for loyalty discounts or bundles: Some subscriptions come free with others (a credit card might give free Disney+; a phone plan might include Netflix). Or, simply call and ask – occasionally you can negotiate a lower rate, especially for utility-like subscriptions (internet, cable).

- Time your sign-ups for deals. If you canceled a service, you might resubscribe when they have a promotion. For instance, one expert mentions scoring Hulu for $1/month during a Black Friday sale. Always be on the lookout for seasonal discounts or coupon codes for subscriptions.

- Use the right credit card for remaining subs. Some cards offer cashback or credits for certain subscriptions (e.g., streaming services). If you’re going to pay for it, you might as well get 5% back or earn points.

The bottom line: after cutting the dead weight, you should feel good about the subscriptions you keep. They’re in your budget, you’re aware of them, and they’re delivering value to you in proportion to their cost.

Maximize Your Savings with Kudos

Once you’ve trimmed down to the subscriptions and services you truly use, make sure every dollar you spend is working hard for you. That’s where Kudos can help. Kudos is a free browser tool that automatically helps you earn the most rewards on your spending – it’s like a smart companion for your wallet.

Kudos helps you earn significantly higher rewards – up to 2–3× more than other portals, giving you 100% of the commission back. In practice, that means when you pay for something online (say your monthly essentials or a remaining subscription), Kudos makes sure you get all the cashback or points you deserve, stacked with your credit card rewards.

It’s completely free to use, and as a bonus for new users, you can use code GET20 to get $20 after your first purchase through Kudos (talk about instant savings!). By using tools like Kudos, the money you save from canceling subscription creep can stretch even further – you’ll earn rewards on the services you keep or any other online shopping, offsetting costs and boosting your budget.

FAQs – Subscription Creep & Saving Money

How often should I review my subscriptions?

At minimum, do a subscription audit twice a year (for example, New Year and mid-year). If you have many subscriptions, consider a quarterly review. Frequent check-ins ensure you catch trials before they become paid and spot price increases. Also review whenever there’s a major life change (moving, new job, etc.), as your needs may change.

I forgot about a free trial and got charged – what now?

If it’s a one-time slip, you might contact customer support and politely ask for a refund – some services will accommodate a first-time forgetful customer. If not, set an immediate cancellation so it doesn’t recur next period. Use this as a lesson to always set a cancellation reminder right when you begin a trial. Going forward, consider avoiding trials that require a card, or use a prepaid card with limited funds to prevent charges.

Are there tools that cancel subscriptions for me?

Yes, apps like Rocket Money and Trim specialize in finding and canceling unwanted subscriptions. They connect to your bank/credit accounts (securely read-only) and flag recurring charges. Rocket Money can even cancel subscriptions on your behalf with a tap, and Trim’s bot can negotiate some bills down. Keep in mind some of these services may charge a fee or a percentage of the savings for bill negotiation. Always weigh if the convenience is worth it (for many, recovering hundreds of dollars in forgotten subs is indeed worth it).

Can subscription payments improve my credit score?

Simply paying for subscriptions doesn’t directly build credit, but how you pay for them can. If you put them on a credit card and pay that card on time, you’re building a positive payment history. In fact, when managed responsibly, recurring charges paid in full each month can help establish a good credit history. The key is not to overextend – keep your credit utilization low. There are also new services that report certain subscription payments (like Netflix, utilities, etc.) to credit bureaus as an added history – though these have limited impact compared to major loans/credit lines.

What if I cancel something and later regret it?

You can always re-subscribe. Most services retain your account data for a while. If you realize after a month that you truly miss that subscription box or streaming service, feel free to sign up again. However, use that experience to be more mindful – maybe there’s a smaller plan or a promotional rate you can take advantage of when you return. And next time, ensure it fits comfortably in your budget before adding it back.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)