Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

When and Why You Should Downgrade Your Credit Card

July 1, 2025

Dropping an expensive credit card doesn’t always mean you have to close the account. In many cases, downgrading your credit card – switching to a no-annual-fee or lower-tier card with the same issuer – can be a an be a practical move than outright canceling. This lets you avoid hefty fees while keeping your credit line open. But when exactly does downgrading make sense, and why should you consider it? Let’s explore when and why you should downgrade your credit card, how to do it, and what to watch out for.

What Does It Mean to Downgrade a Credit Card?

Downgrading (also called a product change) means exchanging your current credit card for a different card within the same issuer’s portfolio. For example, if you have a premium rewards card with an annual fee, you might request to switch it to a basic no-fee version. Importantly, downgrading keeps your account open – you maintain the same account number and credit history, but with a new card product.

Why downgrade instead of cancel? When you downgrade, you typically avoid a new credit inquiry (since you’re not applying for a brand-new card) and you preserve your credit history on that account. The issuer simply updates your account to the new card. This can help you sidestep the potential credit score dip that might come from closing an account. In short, downgrading lets you stop paying for a card you no longer want without the downsides of canceling.

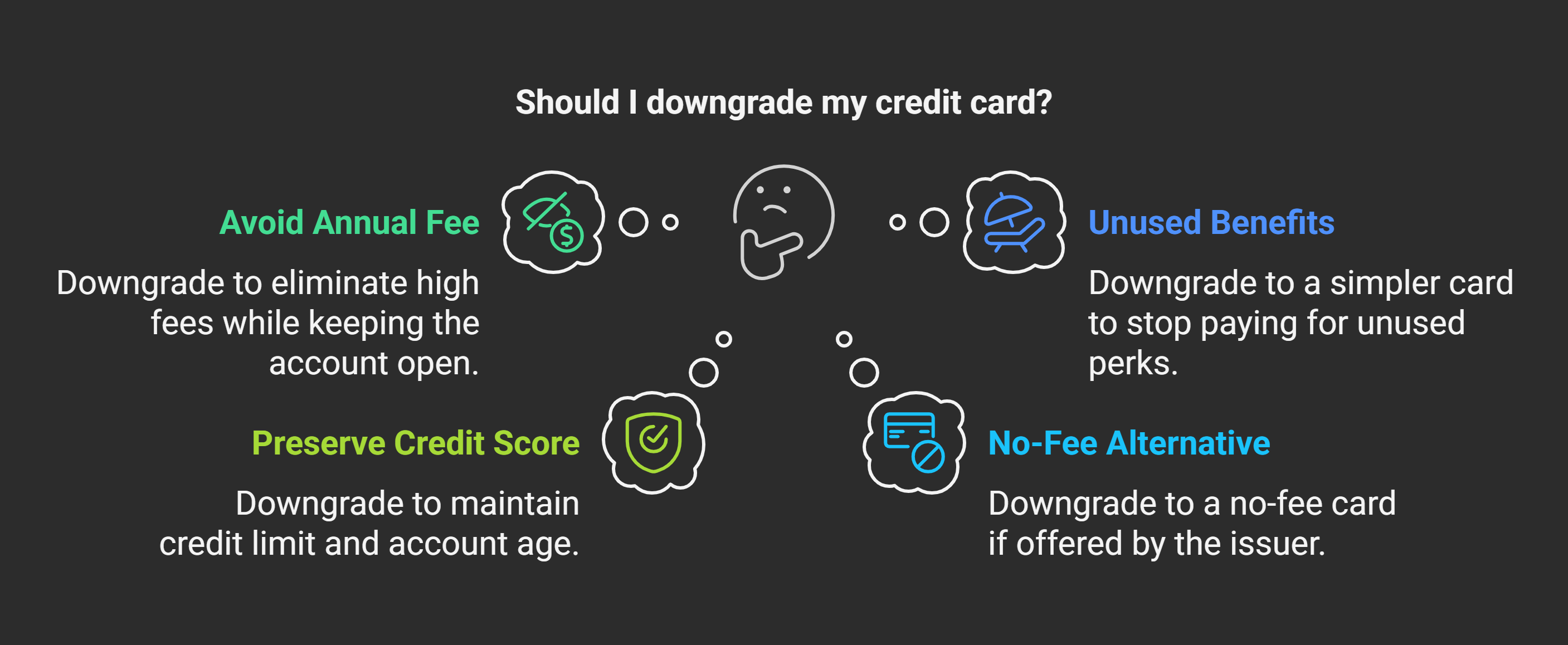

Key Reasons to Consider Downgrading Your Card

- You want to avoid an annual fee. The most common reason to downgrade a card is to get rid of a high annual fee. If your card’s yearly fee no longer feels worth it – maybe your spending habits changed or the perks aren’t useful – downgrading to a no-annual-fee card lets you ditch the fee while keeping your account open. For instance, many premium travel cards have no-fee “little sibling” cards you can switch to. This can help you avoid additional annual fees while keeping the account open.

- You’re not using the card’s benefits enough. Perhaps you originally got a card for its airport lounge access or bonus categories, but now you barely use those perks. Rather than paying for features you’re not using, you can downgrade to a simpler card. You’ll lose the fancy benefits, but you’ll stop paying for something you don’t utilize. It’s a practical move if your lifestyle or spending focus has changed.

- You want to preserve your credit score. Closing a credit card can potentially impact your credit score by reducing your total available credit and eventually shortening your length of credit history. Downgrading avoids those issues. By keeping the account open, you maintain your credit limit (helping your credit utilization ratio) and retain the age of the account on your credit report. In other words, you get rid of the unwanted card product but keep the positive credit effects of having that long-standing account.

- There’s a suitable no-fee alternative from your issuer. Downgrading is only possible if your bank offers another card you’re eligible to switch to. If such an option exists (and it often does for mainstream issuers), it’s an easy way out.

- You’re maxed out on accounts with that issuer. Some banks limit how many credit card accounts you can have with them. If you’re at the cap and eyeing a new card, downgrading one of your existing cards (especially one with a fee you don’t want) could free up your ability to get another product without closing an account. This is a less common scenario, but it can matter for avid card users.

When Is Downgrading Better Than Canceling?

Many people wonder, “Is it better to downgrade or cancel a credit card?” In most cases, downgrading is better if you have a choice, because it lets you retain credit history and avoid credit score pitfalls.

You should downgrade instead of cancel when:

- The card has an annual fee that you can no longer justify paying, but you still want to keep the credit line open. By downgrading, you lose the fee and keep your account.

- You’ve had the card for a long time or it’s one of your older cards. You likely don’t want to close one of your oldest accounts. Downgrading protects that long credit history.

- You don’t need the card’s high-end perks but could use a basic card. For example, you aren’t traveling enough to use a travel card’s benefits – a cashback or no-frills card from the same issuer might suit you now.

- You’re concerned about your credit score impact. If you cancel, your available credit drops and it could affect your score. Downgrade to avoid that.

On the other hand, if no downgrade option exists (not all cards have a lower-tier version), then you may have to consider canceling. Also, if the card in question is relatively new (less than a year old), some issuers might not allow a downgrade immediately. In that case you might wait until the one-year mark passes (to comply with issuer policies and the CARD Act) before downgrading.

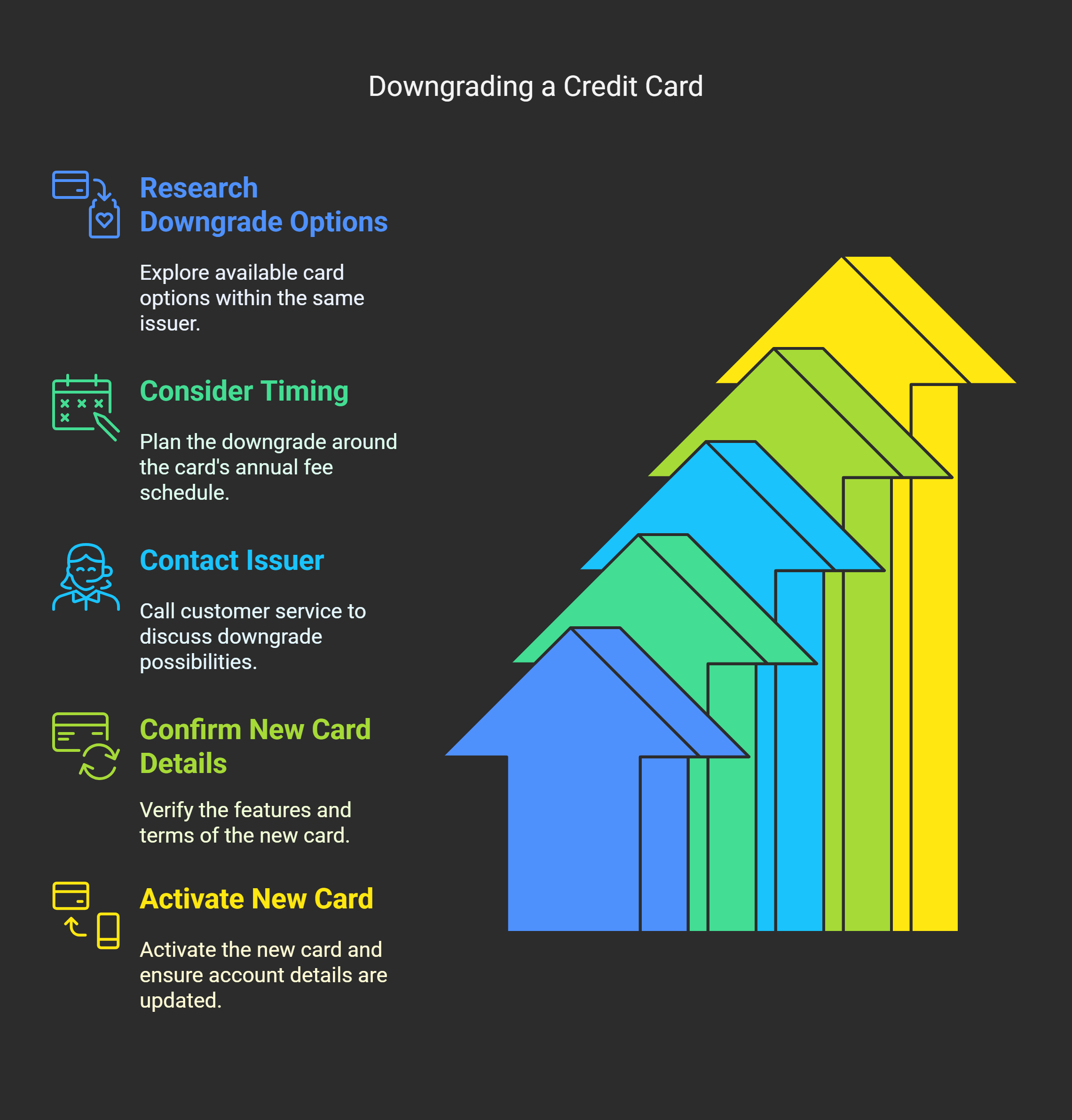

How to Downgrade Your Credit Card

- Research your downgrade options: First, find out what cards you can change to. Typically, you must stay within the same issuer (you can’t downgrade an Amex to a Visa, for example) and often within the same brand or family. For instance, a travel airline card might downgrade to that airline’s no-fee card, or a bank’s rewards card to another of its rewards cards. Check the issuer’s website or call customer service to see available downgrade options.

- Timing matters: Plan the timing around your card’s annual fee. If your fee is about to post (or just posted), downgrading before or shortly after the fee hits could save you from paying it. Many banks will refund an annual fee if you cancel or downgrade within a short window (often 30 days) after the fee posts. So don’t procrastinate once you’ve decided to switch.

- Contact the issuer: Call the customer service number on the back of your card and tell them you’re thinking of canceling because of the annual fee or another reason – but ask if there are no-fee alternatives or a downgrade option. Representatives are usually happy to help move you to a different product if available. You might say, “I’d like to keep my account open but switch to a card with no annual fee.” They’ll walk you through the process if it’s possible.

- Confirm details of the new card: When downgrading, make sure you understand the new card’s features. Ask about the credit limit (it’s usually the same as before), whether any existing balance or rewards transfer over (they typically do), and if there will be any fees or changes. Also ask if downgrading will impact your rewards points – in most cases, points or cash back you’ve earned carry over to the new card, especially if it’s within the same rewards program.

- Activate your new card: The issuer will send you a new card for the product you downgraded to. Once it arrives, activate it and double-check that your old account number now reflects the new card on your online banking. Your account history should remain intact, just under the new card name.

Potential Drawbacks and Things to Watch Out For

While downgrading is often advantageous, be aware of a few trade-offs:

No new customer bonus:

When you downgrade, you’re not opening a new account, so you won’t get any sign-up bonus or introductory 0% APR deal that new applicants might receive. If you were to cancel and open a brand new card instead, you could potentially earn a welcome bonus – but with a downgrade, you forgo that. Weigh this if a big bonus is on the table for a new card; sometimes canceling (and later applying fresh) might be worth it, but often issuers have rules preventing getting a bonus on a card you’ve already had.

You might be ineligible for that card’s bonus in the future:

Related to the above, note that some issuers treat a product change as having “had” the new card. For example, American Express has a once-per-lifetime rule on bonuses; if you downgrade to an Amex card, it could count as you having that card, thus barring you from ever getting its new-member bonus. If earning a new card’s bonus is important to you, consider this before downgrading.

Loss of perks:

Downgrading means you’ll lose any premium benefits of the original card. Ensure you’re okay giving up those perks. For instance, if your current card gives airport lounge access or annual travel credits, the no-fee version certainly will not. Make sure you won’t regret losing those. (On the flip side, if you weren’t using them anyway, it’s no big loss.)

Different rewards structure:

The card you downgrade to may earn different rewards (cash back instead of miles, or lower earn rates). Take note of how your spending rewards will change. You may need to adjust which card you use for certain purchases after the switch.

Check on points and benefits:

If your card is part of a bank’s transferable points program or a hotel/airline program, confirm what happens to your existing points when you downgrade. Generally, points you’ve already transferred to an external loyalty account are safe. Points in the bank’s program should remain if you still have any card that earns that currency.

Issuer restrictions:

Occasionally, an issuer might not allow a direct downgrade if the product types are too different (say, a business card to a personal card, or a co-branded card to a generic card). You cannot change between certain card families (e.g. you usually can’t downgrade a co-branded hotel credit card to a non-hotel card). Know your options are sometimes limited.

Despite these considerations, the drawbacks of downgrading are usually minor compared to closing a card. In most cases, you’re simply trading one card for another that better fits your current needs, and that’s a net positive.

Make the Most of Your Cards After Downgrading

If you do choose to downgrade, you’ll likely end up with a card (or multiple cards) that have no annual fee. Now is the time to maximize those cards’ value. Kudos is a free financial companion that helps you use your cards more effectively by tracking perks and suggesting suitable options.

It’s completely free—Use code GET20 to receive a $20 statement credit after your first eligible Boost purchase (terms apply). By using a tool like Kudos, you can help you continue getting value from your no-fee or downgraded cards. It will remind you of any remaining benefits on your cards and recommend the optimal card for each purchase so you’re never leaving rewards on the table.

For example, if you downgraded from a premium travel card to a basic cashback card, Kudos can help identify which of your cards (downgraded or others in your wallet) to use for groceries versus gas to make the most of your cashback potential.

FAQs: Credit Card Downgrades

Does downgrading a credit card hurt my credit score?

Generally, no. One of the biggest advantages of downgrading is that it should not significantly hurt your credit score. You are keeping the same account open, so your credit history length for that account remains and you maintain your credit limit (helping your utilization ratio).

In contrast, canceling a card could reduce your available credit and eventually shorten your credit history on active accounts, which can ding your score. Just make sure your issuer doesn’t require a new hard inquiry for a product change (most don’t for downgrades). Always confirm with the bank, but typically a downgrade is credit-score friendly.

What happens to my rewards points or cash back when I downgrade?

In most cases, your rewards will carry over to the new card, especially if you stay within the same rewards family. For example, if you downgrade within Chase’s cards, your Chase points remain intact in your account. If you have a co-branded card (like an airline card), miles you’ve already earned in the airline’s program are unaffected by the card change – they’re safe in your airline frequent flyer account.

Just verify if any unused cash back or points on the card itself will roll into the new product (they usually do). It’s wise to redeem or transfer points before downgrading if you’re unsure, but generally banks won’t rob you of rewards just because you switched products.

Can I get a new sign-up bonus when I downgrade to another card?

No, downgrading does not make you eligible for a new sign-up bonus on the card you switch into. Since you aren’t a “new applicant,” the issuer won’t grant the welcome offer. If a big bonus is your goal, you’d have to apply for that card separately as a new account (which might mean canceling your current card or just adding the new one outright).

How do I know if my card has a downgrade option?

Most major issuers provide downgrade or product change options, especially if they offer multiple cards in a series. To know for sure, you can call your card’s customer support and ask, or do a bit of online research (many personal finance sites list known downgrade paths).

For example, Visa Signature travel cards often have a Visa Platinum no-fee version. If you find no information, just call the bank and inquire about “no annual fee alternatives” for your card. They will tell you what’s available. If none exist (rare, but possible), then you might have to decide between keeping the card or cancelling it.

Can I upgrade the card again later if I want to?

Often, yes. Downgrading now doesn’t mean you’re stuck forever. If you later decide you miss the perks, you can request an upgrade back to the original card or another higher-tier card (provided you qualify and the issuer approves). Alternatively, you could apply for a completely new card if that makes more sense.

Keep in mind if you upgrade or re-open a card, you usually won’t get the new customer bonus if it’s the same card you had before. But the flexibility is there – many people downgrade during lean times and upgrade when their situation changes. Just maintain good standing on your account to keep these options open.

By downgrading a credit card instead of canceling, you can save money on fees and keep your credit profile healthy. It’s a valuable strategy in your financial toolkit. Always evaluate your card’s worth to you each year – if it’s not pulling its weight, downgrading is often the win-win solution that lets you bow out of the fee without closing any doors.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)