Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

When Should I Get a Credit Card With My Partner?

July 1, 2025

Paying the bills as a couple isn’t easy. Either you use separate cards and are constantly calculating the difference, have two bank accounts for various direct debits, or one of you manages paying the bills and the other has to make regular e-transfers to compensate.

This can be a stressful way to manage finances for some couples since you aren’t drawing from one consolidated pool of funds. That’s why many consider signing up for a joint credit card since it makes sharing finances much simpler.

It isn’t a solution suitable for every couple, though, as it does come with new problems such as shared liability. This guide will explore the joint card as a way to manage your shared finances and whether it makes sense for you right now.

What Is a Joint Credit Card?

There are three different types of joint credit cards that can grant couples access to perks, sign-up bonuses, and more.

Signing up for a joint card doesn’t have to mean two people registering for a single account and both parties assuming full liability for the funds.

The term ‘joint credit card’ is falling out of favor since, these days, it’s rare for banks to offer a credit card specifically for two people. Today, many banks prefer for the liability of the card to lie solely with one person.

So how does a credit card work between two partners?

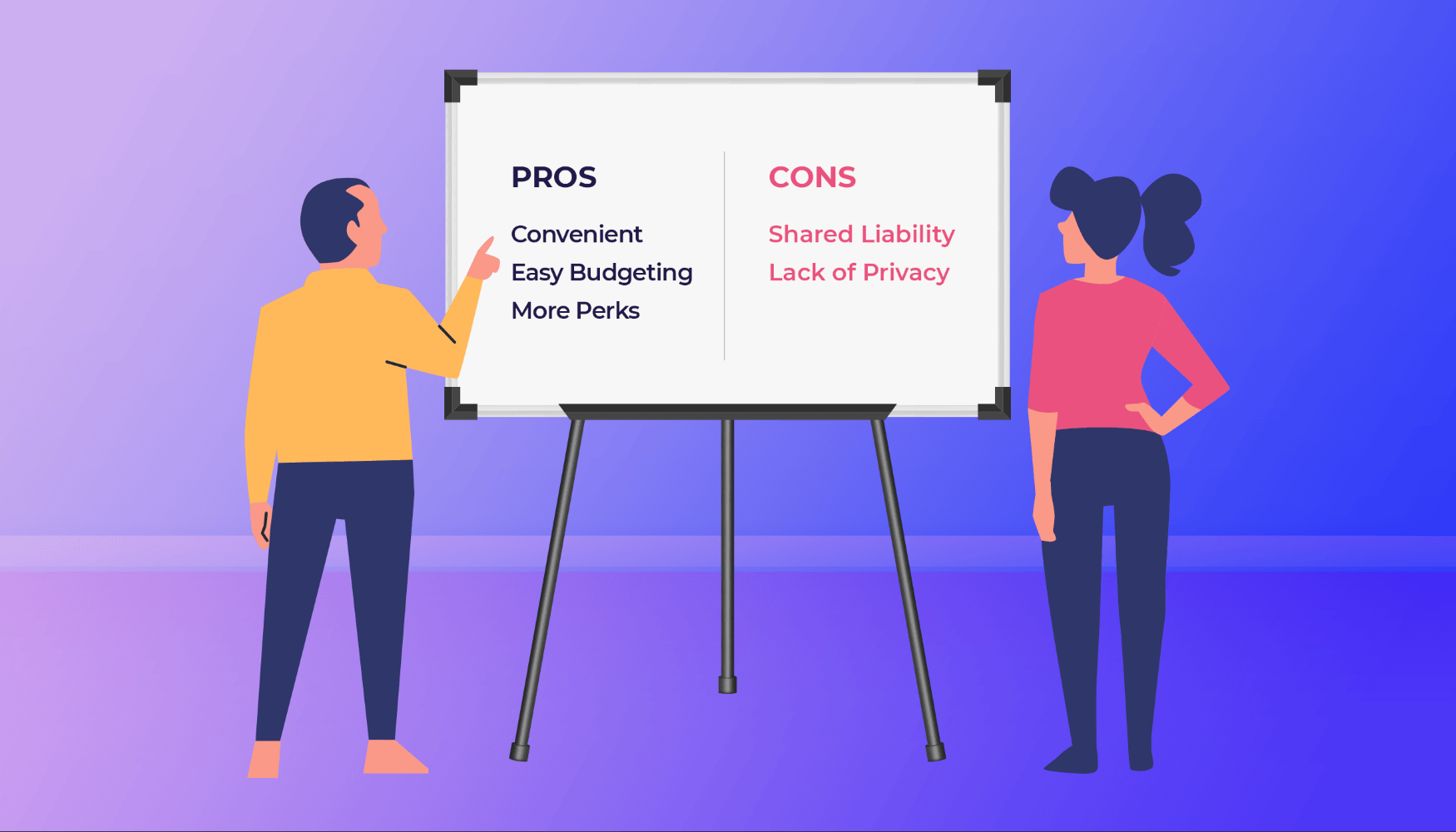

Pros and Cons of Joint Credit Cards

Here is each card category you can use to manage your shared finances:

Shared

Most people think of the shared credit card when they hear the term ‘joint credit card.’ It’s joint ownership in the truest sense of the phrase: both partners are listed on the account, have cards, and ultimately share full liability.

To apply for a shared credit card, both you and your partner will be subject to a hard credit check which will determine whether you qualify and perhaps also the terms you can get the card on.

Closing a shared account is a case of calling your credit card issuer and asking to have the account deactivated. Following this, both account holders will need to pay off any outstanding credit card debt according to the terms agreed upon when signing up for the account.

Co-Signed

A co-signed card allows one of you to be the primary cardholder with access to credit upto the card spending limit. The other partner in this scenario would co-sign and declare that they would bail out the primary cardholder should they default on payments.

The main reason to take this route is if one partner has a poor credit history, as this will limit their options to credit.

There aren’t many banks that issue co-signing as an option for their credit cards, but for those that do, you’ll be able to provide the co-signer’s details with your credit card applications.

Removing the co-signer can be tricky. Provided the primary cardholder has made payments on time, the co-signer might only need to contact the card issuer and ask to be removed. However, if the primary cardholder hasn’t kept up with their payments, it won’t be so straightforward.

Authorized User

The final option is to add your partner as an authorized user on your account. That way, you’ll both be listed on the account with your own cards. The only difference from the shared account is that the authorized user will have limited to no liability and won’t have the information filed on their credit report.

To add someone as an authorized user, find a credit card that allows this option, and have the partner with the highest credit score apply for a more favorable rate and credit cards with high limits.

During the registration process, you’ll come across the option to authorize a user, which is when you would enter your partner’s details. This may require additional service fees.

You can usually have an authorized user taken off the account by calling the number on the back of the card and requesting that they be removed.

Pros and Cons of Joint Credit Cards

Now that you know more about what a joint credit card is and what types there are, what are the main pros and cons of applying for one?

Pros

- Convenience: For many couples, finances are already shared equally. It’s just that the system for sharing the financial burden of their lives is inadequate. If this is the case, the benefit of getting a joint credit card is obvious: it streamlines the process of sharing finances, so the couple doesn’t have to stress about making sure they’re both contributing equally.

- Simple budgeting: When you have a plethora of incomings and outgoings to consider for two partners, making a budget according to each category can seem impossible. With a joint credit card, the process is simple since you can see your combined finances at a glance and use that information to inform your budget.

- Get additional perks faster: When you have a credit card, it can take a long time to qualify for a perk or bonus you wanted when you signed up, such as gift cards or air miles. With a joint account that has more than one holder, it can be much easier to enjoy the credit card benefits since, in theory, there’ll be much more spending.

Cons

- Your credit score could be affected: For each of the joint credit card options, one or both partners could put themselves at risk of taking a hit to their credit score. If you choose a shared credit card, both of you will assume full liability for any debts you accrue. If you default on a payment due to your partner overspending compared to your budget, you run the risk of damaging your credit score. With a co-signed account, the co-signer puts their strong credit rating at risk since they are tying their financial status to that of their partner.

- Shared liability: The primary disadvantage to owning a joint credit card is that you put your finances on the line and have to place a lot of trust in your relationship and your partner. A joint credit card means there are two or more ‘co-owners,’ which is convenient in some ways yet implies a complete shared liability. That means the full financial burden of making sure debts get paid off lies with both partners. The authorized user is the one option in which one partner will have limited or even no liability on the funds they have access to.

- Lack of privacy: When you sign up for a joint credit card, you effectively sign away your right to privacy with your money. Whenever you make a payment, it will appear in your joint account, so your partner will be able to see it. In a joint account, every transaction is transparent, so both partners can see the details of every payment regardless of who made it.

When Is the Right Time To Get a Joint Credit Card?

So when is the right time to push the button and sign up for a joint credit card account?

Long-term committed relationship

The first instance in which you might want to consider getting a joint card is if you’ve been together for several years. This proves you’re in a strong relationship, which is paramount to sharing finances without paranoia.

Lots of shared expenses

If you share a lot of expenses as a couple, such as everyday purchases, bills, and groceries, you probably have to make numerous e-transfers to one another regularly. This is fine for some, but for many couples, this can become frustrating, tedious, and difficult to keep track of who owes who what.

Both have good credit or healthy spending habits

If you’re both prone to spending sprees and the odd lavish combined purchase, then signing up for a joint credit card account could add pressure to the relationship. Wavering finances in the context of a shared credit card can add a huge amount of stress to both partners, so you want to cultivate healthy spending habits before you take the leap.

The 5 Best Credit Cards for Couples

We recommend having your partner as an authorized user since this places less stress on the relationship as one partner has limited to no liability but both get to access the funds. It’s also easy to remove them should your circumstances change.

The best credit cards for young adults will offer credit card rewards, a card sign-up bonus, and extras such as gift cards or luxury hotel access.

Here are five of the best joint credit cards for couples:

American Express Platinum Card®

[[ SINGLE_CARD * {"id": "106", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Serious Points on Flights"} ]]

Chase Sapphire Reserve®

- [[ SINGLE_CARD * {"id": "510", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "$300 Annual Travel Credit"} ]]

Capital One Venture X Rewards Credit Card

- [[ SINGLE_CARD * {"id": "2888", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Luxurious Travel Benefits"} ]]

American Express® Gold Card

[[ SINGLE_CARD * {"id": "118", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Foodies and Frequent Travelers", "headerHint": "4x on Restaurants"} ]]

Blue Cash Everyday® Card from American Express

- [[ SINGLE_CARD * {"id": "260", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "No Annual Fee"} ]]

Conclusion

Joint credit cards can be a great way to share finances without all of the messy calculations. It’s a straightforward solution to combining finances effectively and opens the doors to more quickly obtaining perks associated with the card.

You do have to consider the downsides, too. By opting for a joint credit card, you relinquish privacy in how you spend your money and assume the burden of shared liability which could prove disastrous if you split up.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)