Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Best Metal Credit Cards of 2026: Top 9 Picks Ranked by Category

July 1, 2025

.webp)

The content on this page is accurate as of the posting date; however, some of the offers mentioned may have expired.

What's New in 2026

Before diving into the picks, here are the changes that matter most heading into 2026 — so your research starts with current information, not outdated assumptions.

Chase Sapphire Reserve® annual fee increased to $795. This happened in 2025 as part of a broader benefits overhaul. New credits and expanded partnerships came with it, but it meaningfully changes the break-even math. All value calculations in this guide reflect the current $795 fee.

Marriott Bonvoy Brilliant® American Express® Card limited-time welcome offer. The Marriott Bonvoy Brilliant® American Express® Card is running an elevated welcome offer of 200,000 Marriott Bonvoy® bonus points after spending $6,000 in the first 6 months. This offer ends 5/13/2026 — if you've been considering this card, the window is closing.

More affordable metal cards than ever. No-fee and sub-$100 metal cards have proliferated. You no longer need a $400+ annual fee to carry metal. We cover options across every price point below.

What Makes Metal Cards Different

The weight and feel of a metal card are the first things people notice — but they're not the reason to choose one. Here's what actually matters.

Material and construction. Most metal cards use stainless steel, titanium, or a metal composite core. Card weight runs from about 10 grams for lightweight composites to 18+ grams for full steel cards. Heavier doesn't mean more valuable, but weight often correlates with tier.

The metal card hierarchy generally falls into three tiers. Ultra-premium cards ($500+ annual fee) use titanium or stainless steel construction and typically weigh 13–18 gram. Mid-premium cards ($95–$400) use metal composite or steel and include options. No-fee metal cards use a lighter metal alloy and come with no annual fee.

Durability. Metal cards survive washing machines, overstuffed wallets, and years of daily use far better than plastic. They carry "do not shred" warnings — when a card expires or is cancelled, most issuers send a prepaid envelope to return it for secure destruction.

Metal detectors. Metal cards can trigger sensitive equipment, though modern TSA checkpoints ask you to empty pockets entirely regardless. Place your card with your keys when going through security.

The bottom line. Don't pick a card because it's metal. Pick it because the rewards and credits align with your actual spending. Metal is a byproduct of premium card tiers — not a selection criterion.

The 9 Best Metal Cards of 2026

#1 — American Express Platinum Card®

Best for: Lounge access and travel credit stacking

[[ SINGLE_CARD * {"id": "106", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Serious Points on Flights"} ]]

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level vary by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

#2 — Chase Sapphire Reserve®

Best for: Everyday travel and dining rewards with premium protections

[[ SINGLE_CARD * {"id": "510", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "High-Value Perks"} ]]

#3 — Capital One Venture X Rewards Credit Card

Best for: Maximum premium card value per dollar of annual fee

[[ SINGLE_CARD * {"id": "2888", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Frequent Travelers", "headerHint" : "Luxurious Travel Benefits" } ]]

#4 — Chase Sapphire Preferred® Card

Best for: Entry-level travel rewards with strong transfer partners

[[ SINGLE_CARD * {"id": "509", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Exceptional Travel Value"} ]]

#5 — American Express® Gold Card

Best for: Households with high restaurant and grocery spending

[[ SINGLE_CARD * {"id": "118", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Generous Travel Rewards"} ]]

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level vary by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

#6 — Marriott Bonvoy Brilliant® American Express® Card

Best for: Frequent Marriott guests who want elite status and a free annual night

[[ SINGLE_CARD * {"id": "1189", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "High-End Travel Option"} ]]

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level vary by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

#7 — U.S. Bank Altitude® Reserve Visa Infinite® Card

Best for: Mobile wallet users who want premium perks outside the Amex/Chase ecosystem

[[ SINGLE_CARD * {"id": "2350", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Rewards on Travel Spending"} ]]

#8 — Capital One Venture Rewards Credit Card

Best for: Simple, flat-rate miles with premium metal feel

[[ SINGLE_CARD * {"id": "438", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Frequent Travelers", "headerHint" : "High Travel Rewards" } ]]

#9 — Prime Visa

Best for: Prime members who want a metal card with no incremental annual fee

[[ SINGLE_CARD * {"id": "79", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Amazon Shoppers", "headerHint": "Impressive Rewards and Benefits"} ]]

The information for the Prime Visa has been collected independently by joinkudos.com. The card details on this page have not been reviewed or provided by the card issuer.

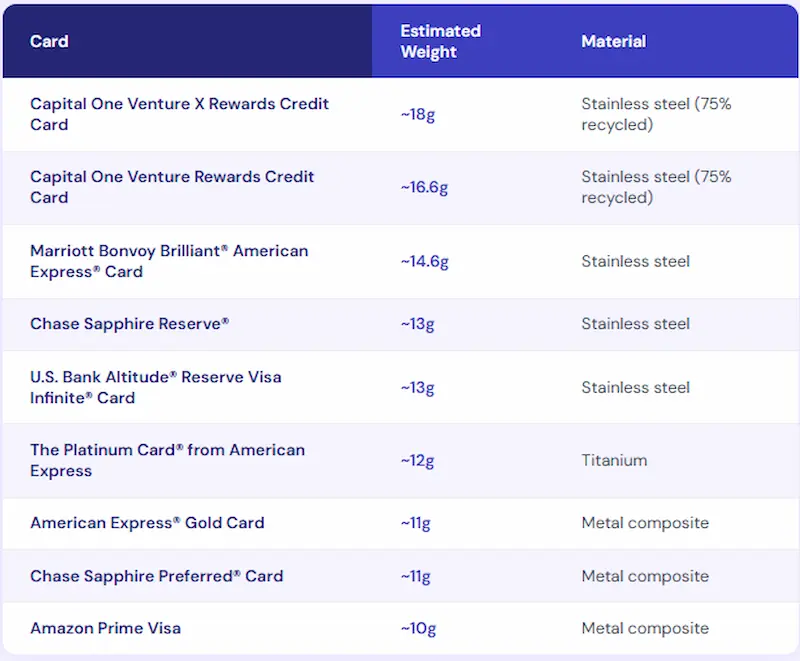

Card Weights at a Glance

Card weights are approximate and may vary by production batch. A U.S. nickel weighs approximately 5 grams for reference. Heavier weight does not indicate higher card value or rewards quality.

The Hidden Math — When Premium Fees Actually Pay Off

The counterintuitive truth about premium metal cards is that a high annual fee can actually cost you less than a low one — if you use the right benefits consistently.

Most premium metal cards bundle their annual fee with a set of recurring statement credits: travel credits, dining credits, rideshare credits, entertainment credits, fitness credits, and more. When you add up the face value of those credits, it often meets or exceeds the annual fee before you earn a single reward point. In that scenario, you're effectively getting the card's rewards program for free.

The math only works, though, if your lifestyle already aligns with the credit partners. A $300 fitness credit is worth zero if there's no eligible gym near you. A $200 travel credit is worth zero if you only fly once a year and the credit applies to incidental fees, not base fares. Credits you have to change your spending habits to use are not savings — they're marketing.

The practical framework. Before applying for any premium metal card, take five minutes to do this: list every credit the card offers, then honestly mark which ones you would use naturally without changing your behavior. Add up only those. If that number exceeds the annual fee, the card is likely worth it. If it falls short, either the credits don't match your lifestyle or a lower-fee card would serve you better.

The single most common premium card mistake is applying for a card because of its welcome offer, then paying a high annual fee year after year for benefits you rarely touch. The welcome offer is one-time. The annual fee is forever.

Airport Lounge Access Explained

Lounge access is the most-cited reason people apply for premium metal cards, and also the most commonly wasted benefit. Understanding how the major lounge networks differ helps you decide how much to weight this perk in your card decision.

Proprietary issuer lounges are owned and operated by the card issuer itself — think of the flagship lounge experiences you've likely heard about. These tend to offer the highest amenity quality: premium food and beverages, full bars, spa services, and quiet workspaces. Access is typically exclusive to cardholders of specific premium cards within that issuer's portfolio. Guest policies and fees vary by issuer and location, so always verify current terms before bringing companions.

Co-branded airline lounges are operated by the airline and accessible to cardholders of affiliated co-branded cards, usually when flying that airline. Benefits like complimentary access or a set number of annual visits are common, but access rules depend on the specific card and ticket type.

Priority Pass™ Select is the broadest independent lounge network, covering more than 1,300 lounges globally across dozens of airports. Most premium metal cards that include lounge access provide Priority Pass membership. Quality varies significantly by lounge and airport — some are excellent, others are modest — so checking the specific lounge in advance is always worth doing.

Practical tip: Download the Priority Pass app or LoungeFinder before every trip to confirm which lounges your card unlocks at your departure airport. The most common lounge-related mistake is paying a premium annual fee for lounge access and then walking past the lounge because you didn't know it was there.

Red Flags — When Metal Cards Become Money Traps

Knowing when not to get a metal card is as important as knowing which one to get. These are the most common ways premium metal cards cost more than they deliver.

You don't travel enough for travel credits to matter. A $300 annual travel credit is valuable if you take multiple trips a year. If you take one domestic trip, it covers a single fare — and the rest of the annual fee is pure overhead.

You'll never use the specific credit partners. The Amex Platinum's Equinox credit only works at Equinox gyms. If there isn't one near you, that credit is worth zero regardless of what the marketing says.

You're excited about the welcome offer, not the ongoing value. A 175,000-point welcome bonus is compelling — once. The card needs to make sense at its annual fee every subsequent year too.

You'll carry a balance. Every premium metal card carries a high variable APR. Carrying a balance even once will cost more in interest than a month of rewards value. These cards are designed exclusively for people who pay in full every month.

You already have a card with overlapping benefits. If you hold both the Amex Platinum and the Chase Sapphire Reserve®, you're paying for two Priority Pass memberships and two Global Entry credits. That's significant double-counting in combined annual fees.

How to Maximize Your Metal Card

Choosing the right card is step one. Actually using all of its benefits is where most cardholders fail — and where the real value lives.

Activate everything on day one. Most card benefits require one-time enrollment: DashPass, Priority Pass, Instacart+, monthly dining credits, Equinox. The day your card arrives, log into your card's benefits portal and activate every benefit, even if you won't use it immediately.

Set monthly calendar reminders. Credits that don't roll over — Amex Platinum's dining credit, CSR's Lyft credit, Amex Gold's Uber Cash — expire at month-end. A recurring reminder on the 25th of each month takes 30 seconds to set up and prevents forfeiting credits you've already paid for.

Use the airport lounge on every single trip. A single lounge visit provides roughly $25–$50 in value (food, drinks, wifi, quiet seating). If your card offers unlimited visits and you fly 10 times a year, that's $250–$500 in annualized value from one benefit alone.

Track your annual value once a year. Calculate every credit you used, every lounge visit, every point earned against the annual fee. If total value is less than what you paid, the card needs to go or your habits need to change.

Stack Kudos on top. When you hold multiple metal cards, Kudos automatically selects your highest-earning card at each merchant at checkout. This is especially valuable when your Amex Gold earns at restaurants but your Venture X earns on everything else.

The Application Process

Most premium metal cards require a good to excellent credit profile. Approval is never guaranteed by a specific score, and issuers look holistically at payment history, income, existing debt load, and recent hard inquiries.

Chase 5/24 rule. Chase typically declines applications if you've opened 5 or more credit cards (across any issuer) in the past 24 months. This applies to both the Chase Sapphire Preferred® Card and Chase Sapphire Reserve®. Check your recent application history before applying.

Amex "once per lifetime" rule. American Express generally limits welcome offer eligibility to once per card, per lifetime. If you've previously held The Platinum Card® from American Express and received a welcome offer, you may not qualify for the current one.

Approval timeline. Most metal cards provide an instant or near-instant decision online. Physical card delivery takes 7–10 business days for most cards, with expedited delivery available for premium tiers.

After approval, before first use. Log into your card account immediately to activate all benefits, set up autopay for the full statement balance, and download your issuer's app to track spending and credits.

Who Should Get Which Card — The Final Decision Guide

The right metal card is the one that matches where you actually spend money and which perks you'll genuinely use. Here's a direct guide to finding your match.

Get the American Express Platinum Card® if you frequently fly through Centurion Lounge airports (JFK, LAX, SFO, MIA, DFW), you regularly use Uber and would otherwise pay for CLEAR, and you can honestly check off using most of the stacked credits in a year.

Get the Chase Sapphire Reserve® if your spending is concentrated in travel and dining, you want the strongest ongoing earn rate in those categories, and the travel credit plus partnership benefits meaningfully reduce your effective annual cost.

Get the Capital One Venture X Rewards Credit Card if you want the best premium card value at the lowest fee in the ultra-premium tier, you're comfortable booking through Capital One Travel for elevated earning, and you travel through airports with Capital One Lounges.

Get the American Express® Gold Card if restaurants and U.S. supermarkets dominate your monthly spending, and you want the highest earn rate on those categories with credits that naturally offset the fee.

Get the Chase Sapphire Preferred® Card if you're new to premium travel cards, want access to the Chase Ultimate Rewards transfer partner network, and aren't yet ready to commit to a $400+ annual fee.

Get the Amazon Prime Visa if you're already an Amazon Prime member, shop frequently at Amazon or Whole Foods, and want a no-incremental-fee metal card with the best category earn rate in its tier.

The universal rule. The average cardholder leaves $624 in unused card benefits on the table annually according to Kudos Insights data. The most expensive card isn't the one with the highest annual fee — it's the one whose benefits you forget to use. Use Kudos Explore to compare these cards side by side, and Kudos Insights to track your benefit usage so every dollar of your annual fee works for you.

Frequently Asked Questions

What is the heaviest consumer metal credit card?

Among publicly available cards, the Capital One Venture X Rewards Credit Card is one of the heaviest at approximately 18 grams. For reference, a U.S. nickel weighs about 5 grams.

Do metal credit cards set off metal detectors?

They can. Most TSA checkpoints ask travelers to empty all pockets regardless, so place your card in your security bin with your keys and loose change.

How do you destroy a metal credit card when it expires?

Do not shred it — metal cards will damage standard shredders. Most issuers provide a prepaid return envelope for secure destruction. Some accept returns at branch locations. Contact your issuer for their specific process.

Are there no-fee metal credit cards?

Yes. The Amazon Prime Visa carries no annual fee (outside the required Prime membership). The U.S. Bank Altitude® Go Visa Signature® Card also has a metal construction with no annual fee.

Can I get a metal business credit card?

Yes. The Business Platinum Card® from American Express and the Ink Business Preferred® Credit Card are well-regarded metal business options with elevated category earning on business expenses.

[[ COMPARE_CARD * {"ids": ["2290", "1100"], "bestCategoryIds":["17", "18", "19"], "bestForTexts":["Premium Offer", "Valuable Rewards"]} ]]

Is a heavier card automatically a better card?

No. Card weight reflects material choice, not benefit quality. The U.S. Bank Altitude® Reserve at 13 grams has outstanding benefits; the Capital One Venture X at 18 grams also does. Evaluate benefits and annual fee — not how satisfying the card sounds when it hits the table.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)