Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Do I Need Commercial Umbrella Insurance? Who Should Get One in 2026?

July 1, 2025

If you’re a business owner wondering whether commercial umbrella insurance is necessary for you, you’re asking a smart question. A commercial umbrella policy provides extra liability coverage beyond your standard insurance. But not every business may urgently require this additional layer.

In this guide, we’ll break down who really needs commercial umbrella insurance (with scenarios that practically scream for extra coverage) and who might not need it right away. By the end, you’ll know if 2025 is the year your business should get that umbrella policy for peace of mind.

Who Definitely Should Consider a Commercial Umbrella Policy

While almost any business could benefit from extra protection, certain types of businesses or situations have a higher risk of big liability claims. If any of the following describes your business, getting a commercial umbrella insurance policy should be a strong consideration:

1. Businesses with Public Foot Traffic (Customers on Premises)

Do you operate a store, restaurant, gym, or any business location where the public comes and goes? If yes, you face the classic slip-and-fall and other injury risks. Inviting others onto your property opens you up to risk. If someone is injured on-site or an employee’s actions harm a visitor, lawsuits could quickly exhaust your general liability policy.

2. Contractors and Businesses Working on Clients’ Property

If you or your employees frequently perform work at other people’s homes or facilities (think electricians, plumbers, cleaners, consultants working at client offices), the risk of property damage or injury is higher. Even a minor accident – say, a contractor accidentally causes a fire or a flood in a client’s building – could result in a massive claim beyond your basic insurance. Working on others’ property means increased risk: even accidental damage can result in expensive lawsuits.

3. Businesses with Significant Assets or High Net Worth

If your company has substantial assets (equipment, cash reserves, property) or you are a high-net-worth business owner, you have more to lose in a lawsuit. Plaintiffs and attorneys know where the deep pockets are – unfortunately, success can make you a target. To protect the hard-earned assets of your business, an umbrella policy provides that extra cushion. Essentially, the more you have, the more coverage you need to insulate it. Large judgments can wipe out assets; umbrella insurance prevents a large award from exceeding your liability coverage and forcing you to liquidate assets or fold the business.

4. Businesses with Many Employees or Higher Workplace Risk

If you have a sizable team or your employees perform risky tasks, consider umbrella coverage. While workers’ comp covers employee injuries, there are cases where employees (or even third parties) sue for negligence beyond workers’ comp limits. Also, more employees can mean more chances of someone else (customer or public) being harmed by an employee’s actions.

5. Companies with Vehicles or Fleet Operations

As hinted above, if your business involves driving – whether it’s a single delivery van or a whole fleet of trucks – you should strongly consider umbrella insurance. Auto accidents can lead to some of the costliest liability claims, especially if multiple other parties are involved. Commercial auto policies have limits, and a bad crash can exceed them. Umbrella coverage will kick in for medical bills and legal claims beyond your auto policy. Even businesses that rent cars frequently or have employees drive personal cars for work (hired/non-owned auto) could see umbrella as a backstop for serious accidents.

6. Businesses in Highly Litigious Industries

Certain industries see lawsuits more often. Examples: hospitality (nightclubs, bars), healthcare (clinics might already have malpractice but could face other liabilities), construction (accidents on sites affecting the public), and so on. If you know your industry tends to attract litigation or large claims, an umbrella is almost a must. It’s basically part of the cost of doing business safely in those fields.

7. Required by Contract or Clients

If a client, landlord, or project contract requires an umbrella policy of a certain amount, then you’ll need to get one to do business with them. This often happens in government contracts or large corporate vendor requirements. They might say “Must carry $3 million in umbrella liability.” Even if you haven’t felt you needed it before, this is a clear situation where you do (at least if you want that client!).

If one or more of the above points hit home for your business, it’s a strong indication that commercial umbrella insurance is a worthy investment in your risk management.

Weighing the Risk: Why Most Businesses Could Use the Extra Coverage

It’s easy to assume only “big companies” or those in extreme situations need umbrella insurance. But consider this perspective: “Unfortunately, [high risk for a lawsuit] describes most businesses”. Even if you run a small business, you might be surprised how a single incident can escalate.

The truth is, liability lawsuits can happen to anyone – and they can be devastating. The average liability suit (just defense and judgment) can easily exceed $50,000, and that’s for relatively minor issues. Major lawsuits can run into the hundreds of thousands or millions.

For most businesses, the cost of umbrella insurance is relatively low (often in the hundreds to low thousands per year range) compared to the protection it provides. It’s essentially transferring the risk of a financially ruinous event to the insurer, for a relatively small premium.

One way to think about it: If your business is on the line (could go bankrupt) from a worst-case lawsuit, then umbrella insurance is needed. If your business could easily absorb a worst-case scenario without it… well, then maybe you’re truly low-risk or well-capitalized enough to skip it. Few small or mid-sized businesses are in the latter category.

Who Might Not Need Umbrella Insurance (Or Could Wait)?

While umbrella insurance is advisable for many, there are a few cases where you might reasonably forego it:

1. Solo Entrepreneurs with No Public Exposure

If you’re a home-based sole proprietor with no employees, no physical storefront, and you don’t have clients visiting you or you visiting them, your liability risk is minimal. For example, say you’re a freelance graphic designer working from home, dealing with clients over Zoom. Your main risks (like maybe a client lawsuit for work errors) would be covered by a professional liability policy, and you have virtually zero risk of a big bodily injury/property damage claim.

2. Businesses Already Fully Covered by Niche Policies

If you operate in a very niche field and have specialized liability coverage with high limits (for instance, a medical practice with hefty malpractice limits, or an industrial company with a large general liability policy already), you might not need an umbrella on top – or you might need a smaller one. Sometimes, you can also increase the limits on your primary policies as an alternative. If your liability insurance limits are already higher than typical (say you already carry $5M GL policy due to contract requirements), an additional umbrella might be overkill unless you want more cushion.

3. Budget-Constrained Startups (with Low Risk)

A brand-new small business with very little customer interaction and limited funds might delay purchasing umbrella insurance initially. If you’re just starting out, operating from a laptop, and your base policies already cover your current exposure, it’s understandable to focus on immediate needs. However, this is a bit of a gamble – as soon as you can afford it, getting even a $1M umbrella is wise.

It’s important to honestly assess your risk. Don’t skip umbrella coverage simply to save money if your risk profile calls for it. As one insurer advises, even if you think you might be in that very low-risk minority, “weigh the risk of being named in a lawsuit before deciding to pass on this additional protection”.

If you’re on the fence, consider consulting an insurance professional. They can help evaluate your specific operations and possibly even run some scenarios of what claims could cost you. Sometimes, hearing that, for example, a common accident in your industry can easily lead to a $2 million claim helps put the cost of an umbrella policy in perspective.

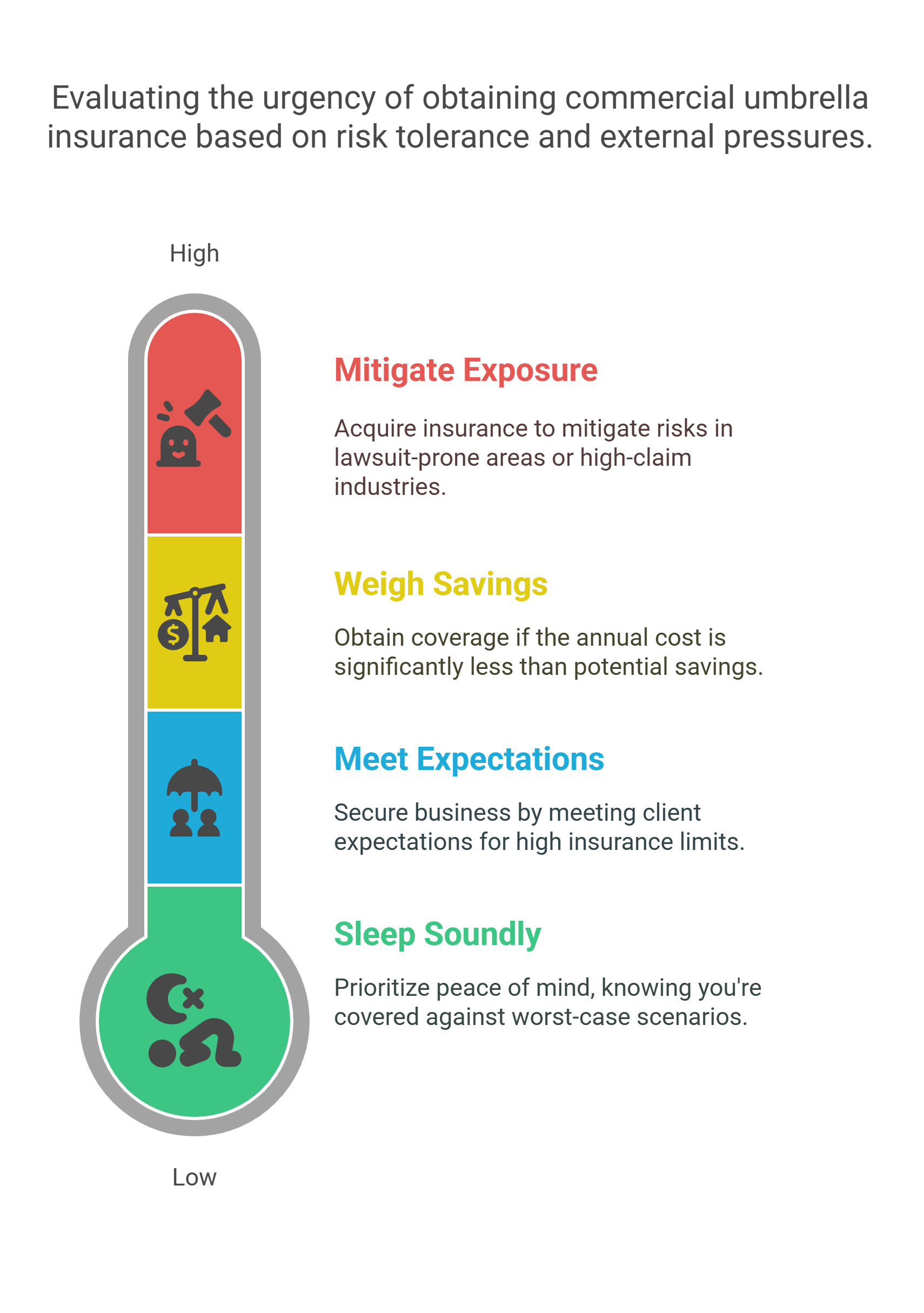

Making the Decision: Umbrella Insurance Now or Later?

To decide if you need commercial umbrella insurance now, ask yourself these questions:

- Can I sleep at night without it? If the thought of a worst-case lawsuit makes your stomach flip (because you know it would exceed your current insurance), that’s a sign you need the extra coverage.

- Do clients or partners expect high insurance limits? If yes, don’t risk appearing underinsured. It could cost you business or credibility.

- How does the cost compare to the risk? Get a quote for an umbrella policy – knowing it might be, say, $500 a year for $1M coverage – and ask if that $500 is worth potentially saving $1M of your own money in a rare event. For most, the answer is yes.

- What is the legal climate in my area/industry? If you’re in a state known for big lawsuits or in an industry where claims are frequent, lean towards getting it.

Remember, insurance is something you hope you never have to use, but you’re incredibly grateful for it when you need it. Commercial umbrella insurance is no different, except it’s safeguarding you against the kinds of losses that could otherwise wipe out years of hard work building your business.

And if you decide you don’t need it today, keep reevaluating as your business grows. Revisit the question annually or whenever you significantly expand operations, take on new activities, or notice the external risk environment changing.

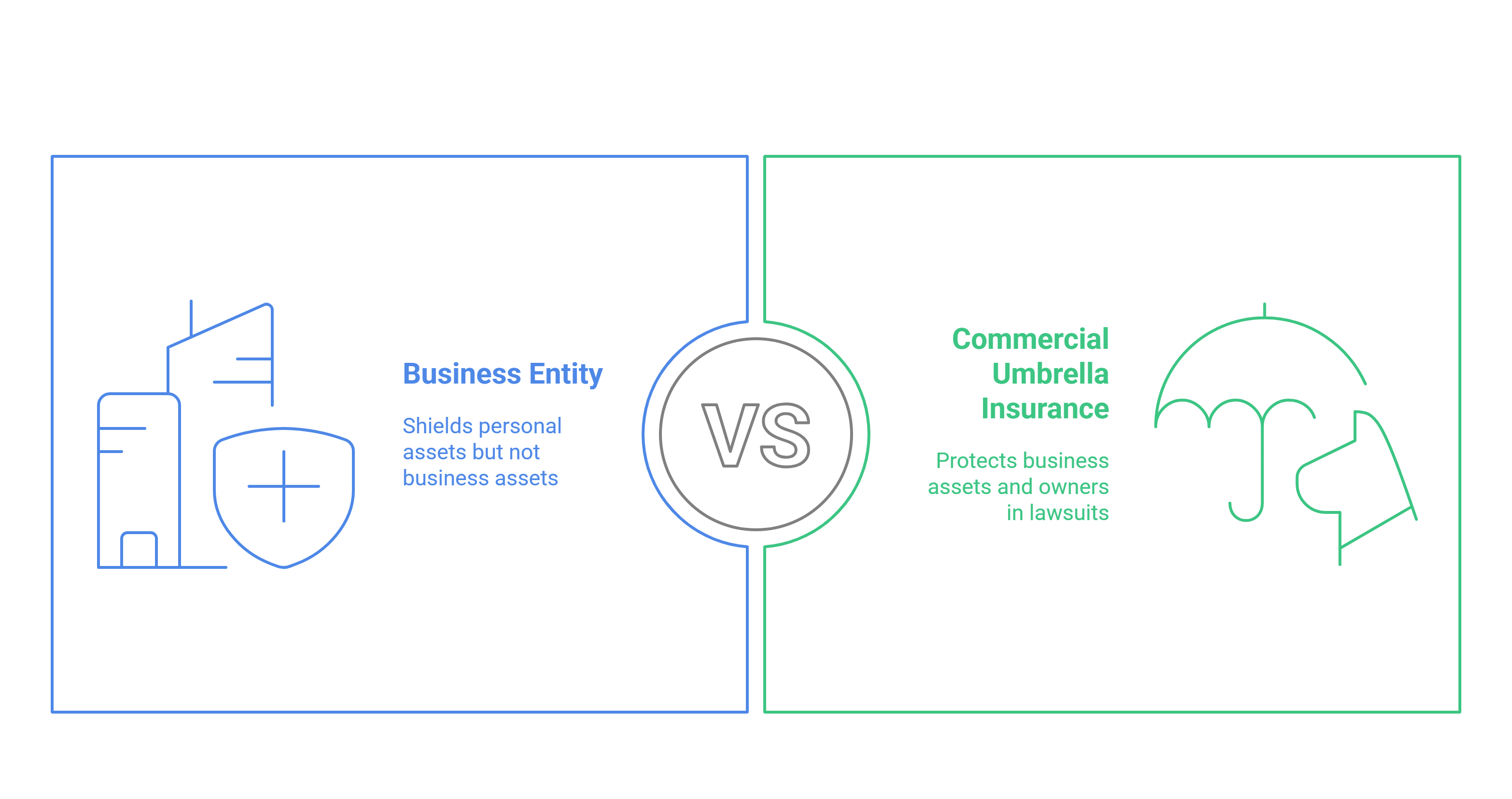

A Note on Personal Assets and Business Structure

One more consideration: Some small business owners think, “I operate as an LLC or corporation, so my personal assets are safe; I don’t need extra insurance.” While an LLC or corporation can shield your personal wealth from business liabilities to an extent, it doesn’t protect your business’s assets – your business could still go bankrupt paying a claim.

Plus, there are scenarios where plaintiffs might “pierce the corporate veil” or include you personally (especially if you personally were involved in an incident). Liability insurance, including umbrella, defends both the business and sometimes its owners/employees in lawsuits. So don’t rely solely on your business entity for protection; insurance is a crucial partner to your legal structure.

In short, if your business has something to lose and faces more than trivial liability risks, commercial umbrella insurance is a prudent safeguard.

Frequently Asked Questions (FAQ)

At what point (revenue or size) should a small business get umbrella insurance?

There’s no fixed revenue threshold, but generally as soon as your business has any meaningful exposure to the public or clients, you should consider it. Even a small business with modest revenue can face a big claim.

How much does commercial umbrella insurance cost for a small business?

The cost can vary by industry and coverage amount, but on average small businesses pay around $75 per month (about $900 annually) for a $1 million commercial umbrella policy. Many pay less – nearly a third of small businesses pay under $50 a month, while some with higher risks pay over $100 a month.

Can I skip umbrella insurance if I just raise the limits on my other policies?

You could increase the limits on your general liability or other policies individually, but that can be expensive and sometimes insurers have a cap on how high they’ll go on a single policy. Umbrella insurance is designed as a cost-effective way to get higher limits across multiple policies.

Does having an umbrella policy mean I can reduce my other insurance?

Generally, no – you shouldn’t drop your primary insurance limits just because you add an umbrella. In fact, your insurer will require you to maintain certain minimum underlying limits (e.g., you usually need the standard $1M liability on underlying policies) for the umbrella to be valid. Umbrella is not a substitute for primary insurance; it’s a supplement. It only kicks in after those primary limits are exhausted.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)