Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Does Your Credit Score Affect Your Renters Insurance Rates?

July 1, 2025

Renters insurance is known for being affordable, but did you know your credit score can influence how much you pay? Yes – in most U.S. states, a lower credit score can lead to higher renters insurance rates. Insurers often review an applicant’s credit-based insurance score when quoting a premium.

In fact, renters with “poor” credit tend to pay about 66% more for insurance on average than those with good credit in states that allow credit scoring. The good news is that credit isn’t the only factor, and some states even prohibit insurers from using credit scores. Let’s break down why credit matters for renters insurance and what it means for you.

Why Your Credit Score Matters to Renters Insurance

Insurance companies use credit information as one factor in determining your renters insurance premium. The key is something called a credit-based insurance score. This isn’t exactly the same as the FICO score a lender might check, but it’s closely related. Both look at similar factors to gauge financial responsibility. The difference is that an insurance score is tuned to predict the likelihood that you’ll file an insurance claim, rather than whether you’ll repay a loan.

Why would your credit behavior relate to insurance claims? It may seem unrelated, but studies have shown a correlation between low credit scores and more frequent insurance claims. Essentially, statistically, people with very poor credit histories tend to file more claims. Insurers view this as a higher risk. So, if your credit-based insurance score is low, an insurer might charge you a higher premium to offset the perceived risk. On the flip side, having excellent credit could earn you a discount – some companies reserve their cheapest rates for customers with top-tier credit.

How big of a difference can credit make? It varies by insurer and state. In many cases, poor credit can bump your renters insurance rate substantially – that 66% figure is an average, meaning some insurers might hike prices even more, while others less so. Each company has its own formula. One insurer might increase your rate 20% for fair credit, another might charge 50% more for the same score. That’s why it pays to compare quotes if you suspect your credit is dragging your rate up.

Credit Checks and Renters Insurance Quotes

When you apply for renters insurance, the insurer may perform a credit check to obtain your insurance score. Don’t worry – this is typically a “soft” inquiry, not a hard credit pull, so it won’t hurt your credit score. In other words, getting a renters insurance quote won’t ding your credit report. The insurer just uses the data to price your policy.

Not all insurance companies weigh credit the same way. A few smaller or niche insurers might ignore credit entirely, but most mainstream insurers do use it in states where it’s allowed. You usually won’t be asked for a specific credit score when buying renters insurance; instead, the company checks behind the scenes. If you have no credit history or very thin credit, the insurer might treat you similarly to someone with lower credit.

States Where Credit Scores Don’t Impact Renters Insurance

Insurance is regulated at the state level, and some states ban or limit the use of credit scores in setting insurance rates. For renters (and homeowners) insurance, California, Maryland, and Massachusetts do not allow credit-based insurance scoring.

Hawaii and Michigan have also put strict limitations on credit use for insurance pricing. If you live in one of these states, your credit score won’t impact your renters insurance premium by law. In all other states, however, credit can be factored into your rate.

It’s worth noting that even in states where credit is used, insurers cannot use your credit score as the sole reason to deny coverage – they typically consider it alongside other factors. And if an insurer does raise your rate or deny your application partly due to your credit info, they are required by the Fair Credit Reporting Act to inform you.

You have the right to request an “adverse action” notice that explains the factors from your credit that influenced the decision. This can clue you in on what financial issues to address.

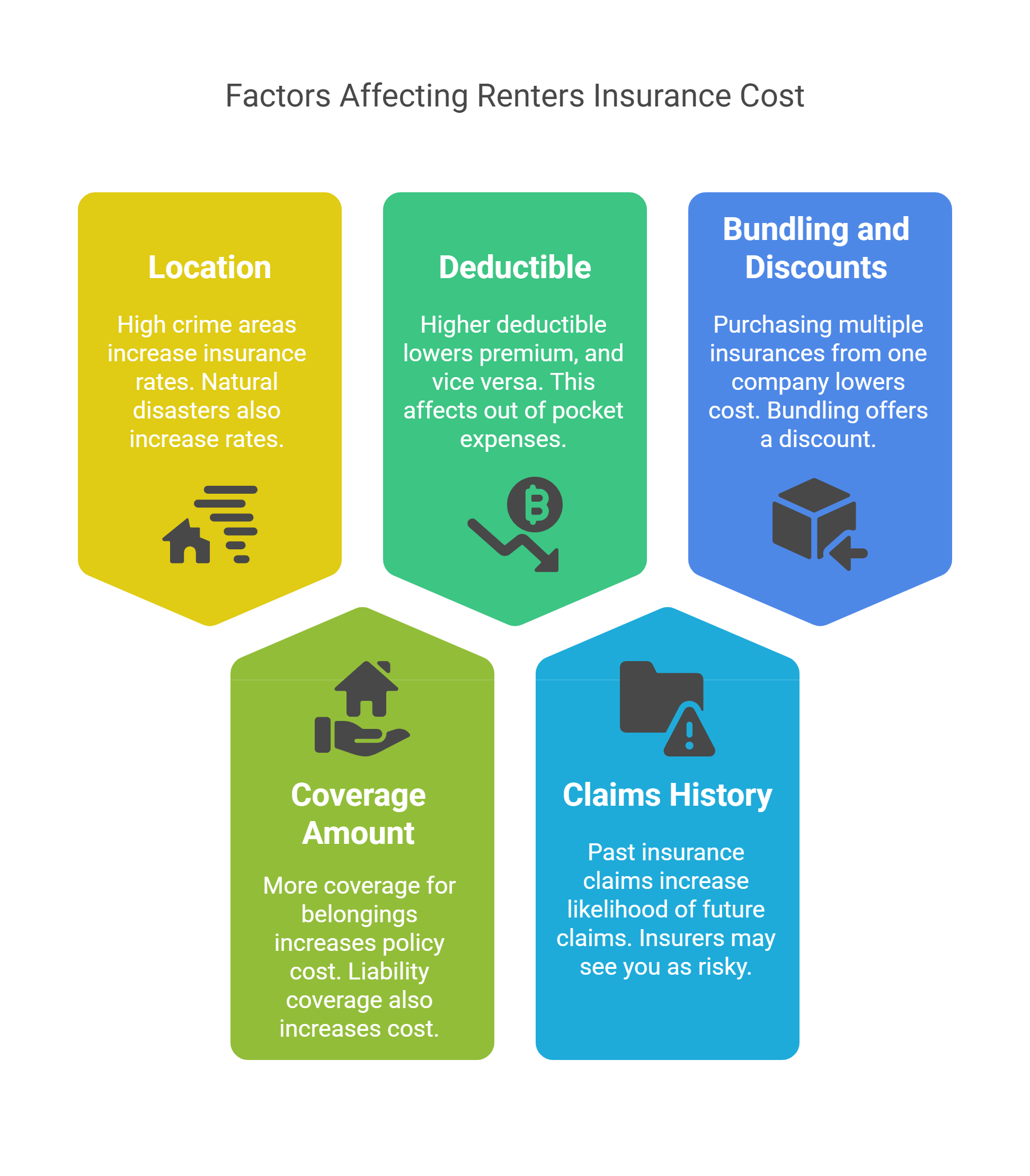

Other Factors Affecting Renters Insurance Rates

Credit score is just one piece of the puzzle. Renters insurance premiums also depend on:

- Location of your rental: Areas with higher crime rates or frequent natural disasters tend to have higher rates, as the risk of theft or damage is greater.

- Coverage amount: The more coverage you need for your belongings or liability, the more your policy will cost.

- Deductible: A higher deductible (what you pay out of pocket in a claim) usually means a lower premium, and vice versa.

- Claims history: If you’ve filed insurance claims in the past (renters or even auto/home claims), insurers may see you as more likely to claim again.

- Bundling and discounts: If you purchase renters insurance from the same company that insures your car, for example, you might get a bundling discount.

Given all these factors, credit is not the be-all end-all. But it can have a significant swing effect: two renters with identical apartments and coverage might get very different quotes if one has excellent credit and the other has poor credit.

Is It Fair to Use Credit for Insurance? (The Debate)

Using credit scores in insurance pricing has sparked debate. Consumer advocates point out that it can disproportionately hurt lower-income individuals and minorities, who on average have lower credit scores due to systemic factors. Essentially, people already struggling financially may get hit with higher insurance costs, making it harder to afford coverage.

During the COVID-19 pandemic, for instance, sudden job losses caused credit score drops for many – and those with worse credit may have seen insurance premiums rise at the worst time.

Insurance companies defend the practice by saying it helps align premiums with risk more accurately. From their perspective, it wouldn’t be fair for low-risk customers to subsidize higher-risk ones. An industry expert explains that if someone is more likely to file a claim, “logically they should pay more for insurance”. Both things can be true: credit scoring makes pricing more precise on average, but it can feel unfair on an individual level if you have bad credit for reasons beyond your control.

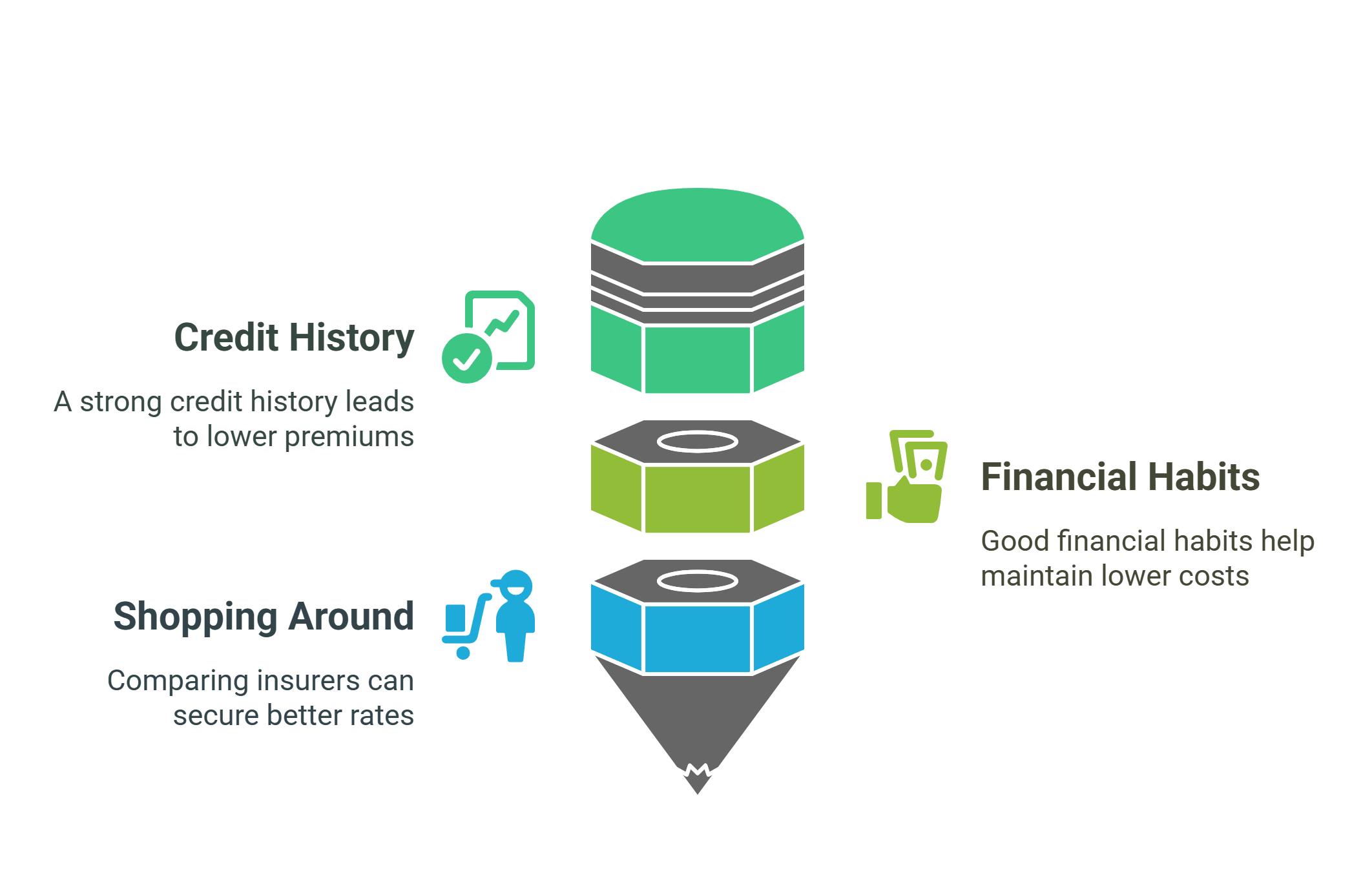

For now, the practice is legal in the majority of states. Regulators continue to examine its impacts. As a renter, the key takeaway is that improving your credit can pay off in lower insurance costs, while letting your credit slide could cost you over the long run.

Bottom Line

Your credit score can absolutely affect your renters insurance rates in most states. A strong credit history can help you snag a cheaper premium, while a poor credit history might lead to a more expensive policy. Make sure to maintain good financial habits – it not only helps your borrowing ability but can also keep your insurance costs down.

And remember to shop around with multiple insurers, because each company treats credit a bit differently. By understanding this credit-insurance link, you can avoid surprises on your bill and take steps to secure the best rate possible.

Frequently Asked Questions (FAQs)

Which states don’t allow credit scores to affect renters insurance?

Currently, at least five states ban or heavily restrict credit-based insurance scoring: California, Hawaii, Maryland, Massachusetts, and Michigan. In these states, insurers cannot use your credit history to set renters (or home) insurance rates. In all other states, your credit can be factored into pricing.

How much more will I pay for renters insurance with bad credit?

It depends, but studies show it can be significantly higher. One analysis found renters with poor credit pay about 66% more in premiums on average compared to those with good credit. Your exact rate increase will vary by insurer and how “bad” your credit is – some might see smaller increases, others larger.

Do all renters insurance companies check your credit?

Most major insurance companies do use credit as part of their pricing in states where it’s permitted. They won’t always do a visible “credit check” that shows up to you; instead they pull an insurance-oriented credit score behind the scenes. A few insurers (or certain state-sponsored insurance programs) might not use credit, but those are more the exception than the rule.

Will getting a renters insurance quote hurt my credit score?

No. Insurance inquiries are treated differently than loan or credit card applications. When an insurer checks your credit for a quote, it’s a soft inquiry that does not impact your credit score. You might see it listed on your credit report, but it won’t lower your score.

What can I do if my credit is making my renters insurance expensive?

First, make sure to shop around – another insurer might offer a better rate for the same coverage even with your credit profile. You can also work on improving your credit over time. Ask your insurer if they can re-evaluate your rate after a year or so of improved credit. Additionally, look for other discounts to help offset the credit surcharge.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)