Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Renters Insurance with Bad Credit: 5 Tips to Save on Your Premium

July 1, 2025

Having bad credit can make many things more expensive – and renters insurance is no exception. If your credit score is low, you might notice higher quotes when shopping for a policy. On average, renters with poor credit pay substantially more than those with good credit.

The good news is you’re not stuck paying a fortune. There are several ways you can save money on renters insurance even if your credit isn’t great. Below are five tips to help you get affordable coverage with a less-than-perfect credit score.

1. Shop Around and Compare Quotes

The number one rule: don’t settle for the first renters insurance quote you get. Different insurance companies treat credit history differently. One insurer might penalize a low credit score heavily, while another might be more forgiving.

Take advantage of online quote tools and independent agents. Gather at least 3 quotes from different insurers. Make sure you’re comparing apples to apples. By shopping around, you might find a company that offers a much better rate for someone with your credit profile.

Why this works: Every insurer has its own formula for pricing. Some give more weight to your credit score, others focus more on your claims history, location, or other factors. If your credit is a sticking point for one company, another might give it less emphasis. The only way to find out is to check multiple options.

2. Look for Credit-Friendly Insurers or Alternatives

Not all insurance companies use credit the same way. Some smaller or regional insurers, or newer InsurTech companies, advertise that they either don’t use credit scores or are more lenient for people with poor credit. If you have bad credit, it’s worth researching which insurers might be a better fit.

For instance, in a few states there are state-backed insurance plans (often called “FAIR plans” or similar for high-risk homeowners) that might not consider credit – though these are usually last-resort options and not typically needed for renters insurance. More commonly, you might find an insurer that markets themselves to customers with imperfect credit or one that uses other data in underwriting.

Additionally, check your state’s laws. As mentioned in our other article, a handful of states ban credit-based insurance scoring. If you’re in one of those, your credit won’t matter to insurers by law, so you can focus on other factors. If not, focus on finding an insurer with a credit policy you’re comfortable with. Customer reviews and insurance agents can sometimes shed light on which companies hit folks with the largest credit surcharges.

3. Bundle Policies and Ask About Discounts

One easy way to snag a lower rate is to take advantage of discounts. Many insurers offer a discount if you bundle your renters insurance with another policy (like your auto insurance). If you own a car, getting both policies from the same insurer could shave off a percentage of each premium. Even if your credit is making the base rate higher, a bundling discount of say 5-10% can help offset that.

Always ask insurers about any discounts you might qualify for. Common ones include:

- Multi-policy discount: as mentioned, bundling renters with auto or other insurance.

- Security systems or safety devices: If your rental has burglar alarms, smoke detectors, or sprinklers, some insurers lower your rate.

- Claims-free discount: If you’ve never filed a renters insurance claim, you might get a better price.

- Paying annually: If you can pay your full year’s premium upfront, some companies discount the total.

- Paperless/auto-pay: Enrolling in electronic billing or automatic payments can earn a small discount with certain insurers.

Each discount might be small, but together they can make a dent in your premium. When your credit score is working against you, you want all the other savings you can get.

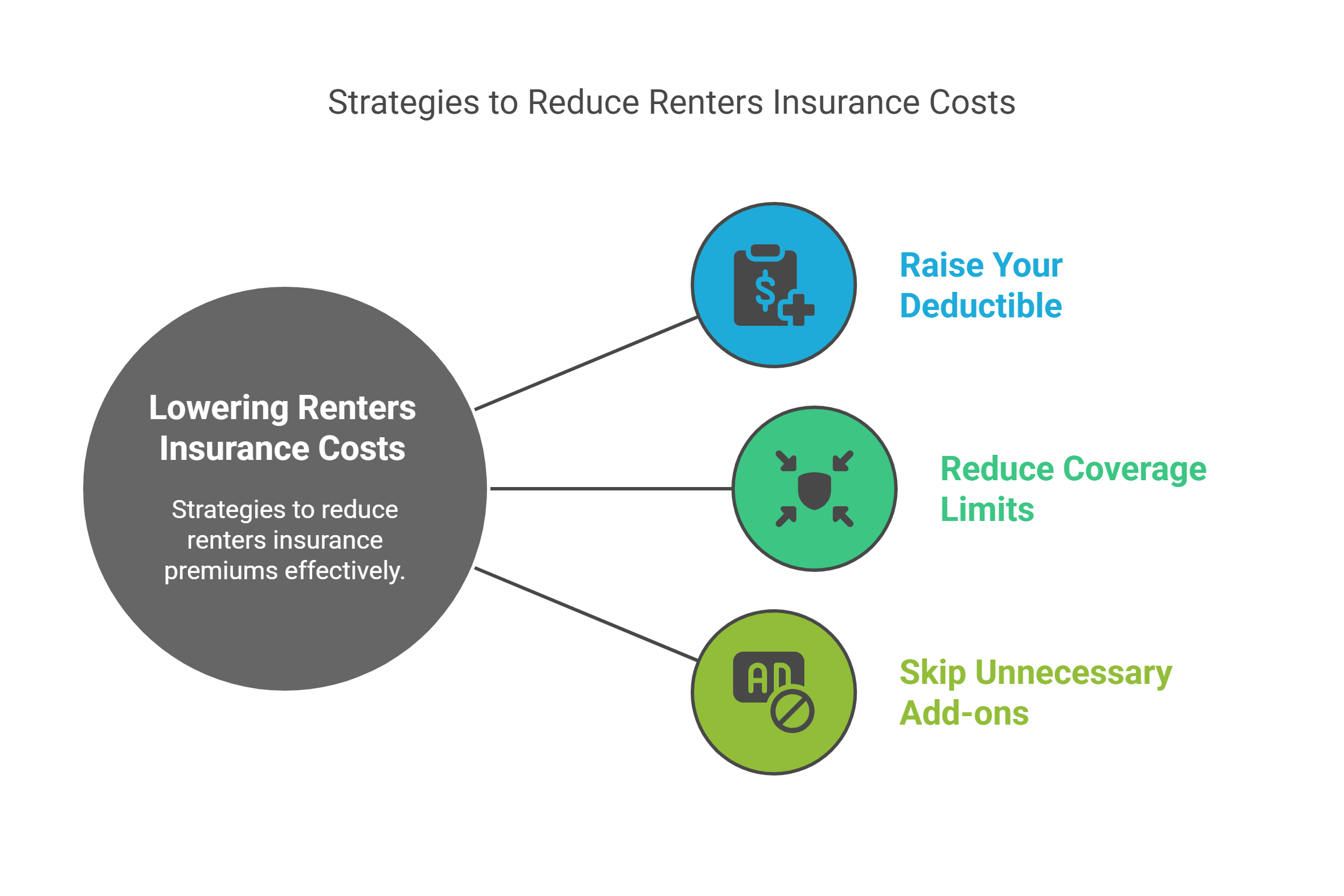

4. Adjust Your Coverage and Deductible

Another strategy to lower your renters insurance cost is to tweak the policy details:

- Raise your deductible: The deductible is what you’d pay out-of-pocket if you file a claim. Increasing it from, say, $500 to $1,000 can lower your premium. Just be sure you could afford that $1,000 if you had to make a claim.

- Reduce coverage limits (if appropriate): Don’t skimp on necessary coverage, but you might be able to lower your personal property coverage if you realize you don’t need as much.

- Skip unnecessary add-ons: Maybe you added an endorsement for jewelry or identity theft coverage that you can live without. Cutting extras can save a few dollars.

These adjustments apply to anyone looking to save, but they’re especially helpful if your credit score is inflating your premium. By making careful choices about your coverage, you can counteract some of the credit-related cost.

Just balance it with making sure you still have the protection you need (you don’t want to under-insure yourself and regret it later during a claim).

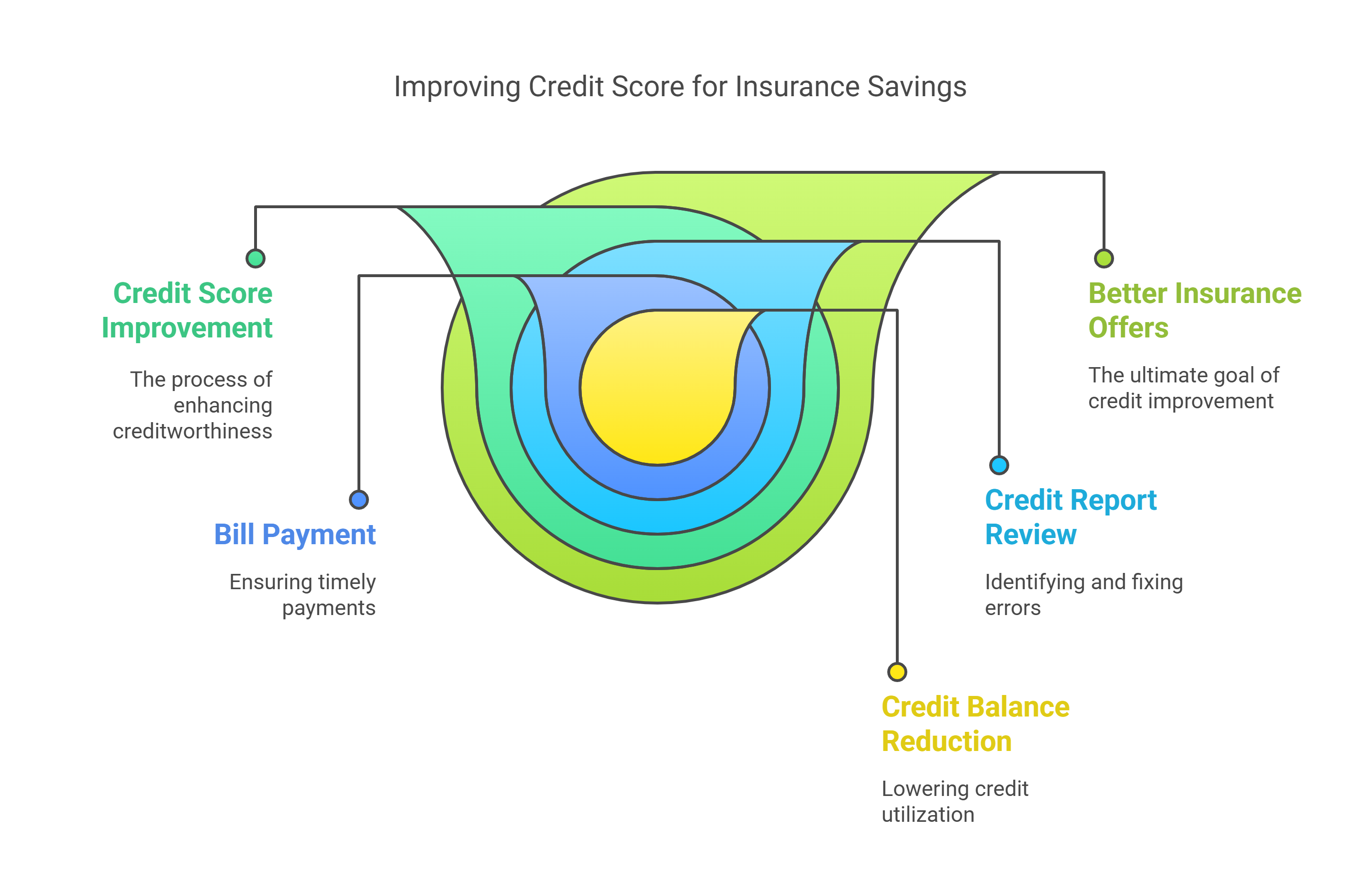

5. Improve Your Credit (Longer-Term Fix)

While it’s not an overnight solution, one of the best ways to save on insurance (and many other expenses) is to improve your credit score over time. As your credit moves from the “poor” range up to fair, good, and excellent, you’ll likely see better insurance offers.

Start by checking your credit reports for any errors or issues that could be dragging you down. Fixing an incorrect late payment or paid-off debt that’s still listed can boost your score quickly.

Beyond that:

- Pay bills on time – payment history is the biggest factor in your credit score.

- Reduce credit card balances – high credit utilization can hurt your score. Try to pay down existing debt if possible.

- Avoid new credit applications while you work on improving (too many inquiries can ding your score temporarily).

- Build positive history – if you have very little credit, consider using a secured credit card or a credit-builder loan to establish a track record.

As months go by, these actions can raise your score. Even a jump from “poor” to “fair” credit could make a difference in the insurance rates you’re offered. Be patient and keep at it. You can request that your insurer re-run your credit at renewal or requote your policy after your score has improved – you might earn a discount.

Also, remember that credit-based rates can work in your favor too: when your score improves, you deserve those better prices. Insurers won’t automatically lower your rate just because your credit got better, so be proactive in asking or re-shopping your coverage at renewal time.

Final Takeaway

Bad credit might make your renters insurance more expensive, but by using the strategies above, you can still keep your premium manageable. The key is to be proactive – compare options, leverage discounts, adjust your policy wisely, and work on your credit for the long run.

Don’t be discouraged from getting renters insurance due to a low score; the protection for your belongings and liability is still very much worth having. With a bit of effort, you can find a policy that fits your budget until your financial picture brightens.

Frequently Asked Questions (FAQs)

Can I be denied renters insurance because of bad credit?

It’s uncommon to be outright denied renters insurance solely for poor credit. Insurers that use credit mainly adjust your rate up or down. As long as you meet other criteria, you should still be able to get coverage. In rare cases, an insurer might decline an application if the credit is extremely bad combined with other issues, but generally they’ll just charge a higher premium instead of denying you.

What credit score is needed for renters insurance?

There’s no specific minimum credit score required to buy renters insurance. Even with a very low score, you can get a policy – there isn’t a cutoff like “below 500, no insurance.” However, the lower your score, the higher your rate is likely to be. A “good” credit score will usually net you the best prices, whereas “fair” or “poor” credit will mean you pay more. The exact impact varies by insurer.

Which renters insurance companies don’t check credit?

Most major insurers do check credit in states that allow it. There are a few that advertise not using credit scores – often newer companies or those in states with bans on credit-based scoring. It changes over time, but if you specifically want no credit check, you might need to seek out a specialty insurer or get assistance from an independent agent who knows companies that are more lenient. Always ask the insurer or agent directly if credit is used in pricing.

Will my renters insurance premium go down if my credit improves?

It can, but it might not happen automatically. If your credit score has significantly improved since you first bought your policy, contact your insurance company and let them know. They can re-run your credit-based insurance score and potentially adjust your premium downward. If they won’t, you can shop around with your new and improved credit – you may find lower quotes from other insurers that reflect your better score.

Does paying renters insurance monthly help my credit?

Not really. Renters insurance payments are not reported to credit bureaus, so paying on time doesn’t directly build your credit history. The only time insurance might affect your credit is if you fail to pay altogether and your account goes to collections – that could hurt your credit. So, while paying your premium monthly is a good habit, it won’t boost your credit score like a credit card or loan payment would.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)